THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Chain Store Sales

The post Black Friday sales decline continues with the ICSC index falling -0.1% on top of the prior week’s 2.3% decline. The index has now fallen 3 of the last 4 weeks. The year-over-year growth declined to 2.9% from 3.8% last month. Since there were apparently no weather issues and the survey suggests that more shopping has been completed than at this point last year, sales trends are likely to slow further.

Small Business Optimism

The National Federation of Independent Business index rose from 90.2 to 92 for November driven by better U.S. consumer spending and credit conditions. This is the third consecutive monthly gain and puts the index at its highest since February 2011; although the index remains 2-points lower than where it started the year. Most of the details are improving from depressed levels; hiring plans and sales expectations showed improvement between October and November.

Comments from CEO Keith McCullough

Our call yesterday for a Short Covering Opportunity only remains relevant from the level we made it at – manage your risk on green today:

- CHINA – certified train wreck in Chinese stocks didn’t stop overnight w/ the Shanghai Comp down another -1.9% to -19.9% YTD finally moving it to an immediate-term TRADE oversold signal in my model. Chinese Exports to Italy in NOV down -23% y/y! (not a typo)

- European Data – first morn in what seems like forever (10 months) where my entire data run on Europe was not a another sequential deterioration – better than toxic is still awful, but German ZEW up for the 1st time in 10mths to -53.8 (vs -55.2) and the UK inflation print stopped going up (+4.8% NOV vs +5.0% OCT). European Stagflation remains.

- COMMODITIES – last Thursday I cut my asset allocation to commodities back down to 0% after the ECB press conf as I thought the EUR/USD was going to unwind again – get that USD direction right and you get Commodities right – Oil, Copper, Corn, etc all have broken TAILS and Gold continues to break down this morning (new Gold range = 1 w/ TREND resistance = 1743)

I’m long SPY and holding my longest net long position of Nov/Dec. I doubt I overstay my welcome.

KM

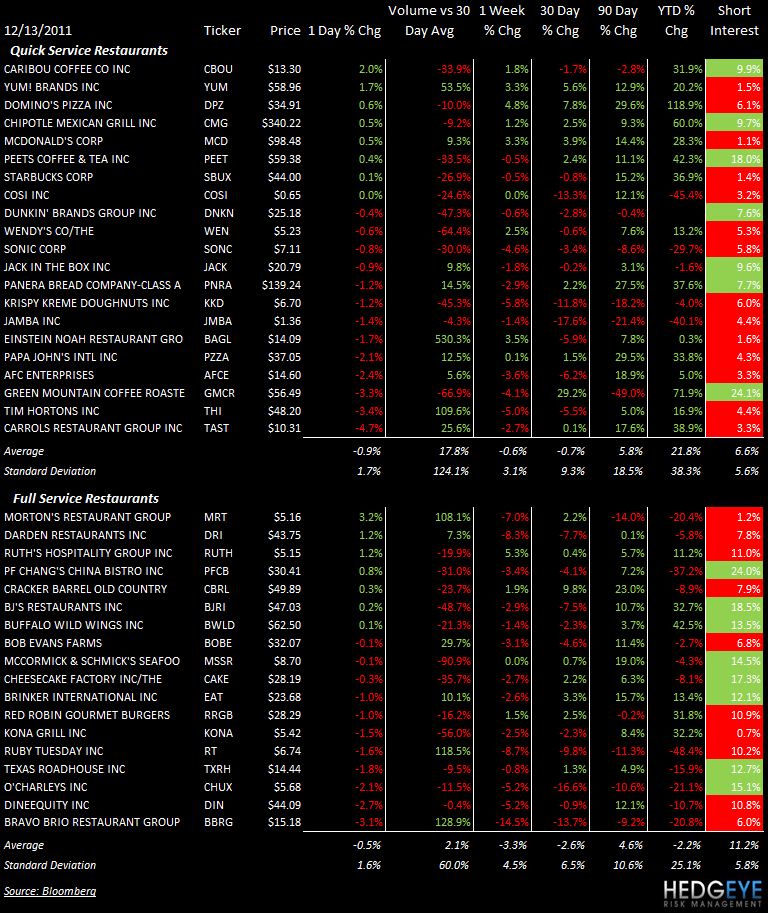

SUBSECTOR PERFORMANCE

QUICK SERVICE

DNKN: Dunkin’ Brands released an investor presentation this morning on the back of yesterday’s positive initiation from Jeffries (“Buy”, PT $30). Both the presentation and the initiation were bereft of any details on the all important backlog. To hit the company’s long-term target EPS growth of 15%+, unit growth needs to pick up and we are not seeing sufficient evidence of this yet.

PEET: Peet’s Coffee was initiated “Buy” at Jeffries.

SBUX: Starbucks was initiated “Buy” at Jeffries.

SBUX: Starbucks was reiterated “Overweight” at JP Morgan.

PNRA: Panera Bread was initiated “Buy” at Jeffries.

CASUAL DINING

EAT: Brinker President of Global Business Development, Carin Stutz, has left the company in order to take over as president and CEO of Illinois-based COSI from January 1.

Howard Penney

Managing Director

Rory Green

Analyst