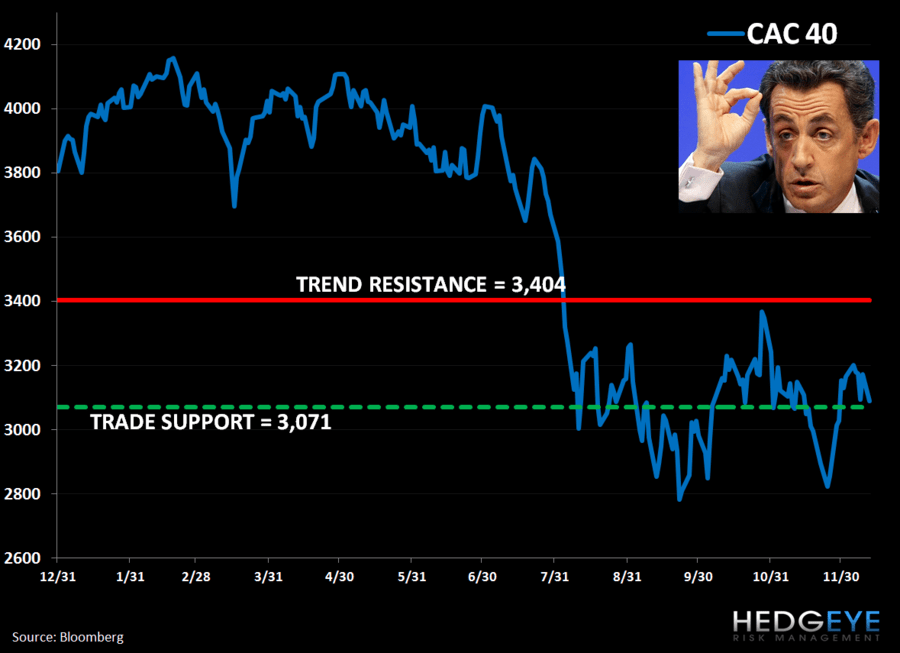

Keith covered France via the eft EWQ in the Hedgeye Virtual Portfolio today. Keith is trading risk around the position, covering it on red days, and shorting it on green days. We remain bearish on French stocks for the intermediate term TREND, with the CAC broken on TREND at 3404 (see chart below).

We remain bearish on France over the intermediate term due to:

- Pending downgrade of France’s AAA Sovereign Credit rating in T-3 weeks

- Public debt rising through the 90% (as a % of GDP) next year

- Slowing growth (below the government’s 1% 2012 projection) alongside Austerity’s Bite

- Banking risk, including any difficulties for its major banks (BNP, Credit Agricole, SocGen) to raise capital to the 9% Core Tier 1 ratio, and sovereign risk as France is the largest holder of Italian public debt and private debt, according to BIS

- EFSF and IMF are undercapitalized to materially aid any potential sovereign and banking bailout needs of France

- High unemployment rate of 9.8% (versus 7% in Germany); 22.8% among the French youth

- Smaller export profile (versus Germany), so there’s less benefit to grow via exports

Matthew Hedrick

Senior Analyst