TODAY’S S&P 500 SET-UP – December 12, 2011

Back to reality! Europe failed to deliver on a consensus failure to understand what they could deliver. Interconnectedness should insulate the risk management of ranges. We like US Consumption stocks (Healthcare and Consumer Discretionary) as the USD strengthens and Deflating The Inflation becomes more and more obvious. As we look at today’s set up for the S&P 500, the range is 37 points or -1.77% downside to 1233 and 1.18% upside to 1270.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2150 (+4348)

- VOLUME: NYSE 819.22 (-11.96%)

- VIX: 26.38 -13.76% YTD PERFORMANCE: +48.62%

- SPX PUT/CALL RATIO: 1.61 from 1.23 (+30.30%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 53.67

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.07 from 1.99

- YIELD CURVE: 1.85 from 1.77

GLOBAL MACRO DATA POINTS (Bloomberg Estimates):

- Japan November corporate goods price index +1.7% y/y vs cons +1.5%. November machine tool orders +15.9% y/y.

- Australia October trade balance A$1.60B vs cons A$1.90B.

- Germany Nov wholesale price index +4.9% y/y vs consensus +4.2%, prior +5.0%

- 11:30am: U.S. to sell $29b 3-mo., $27b 6-mo. bills

- 2pm: Monthly budget statement, est. $139b (prior -$150.4b)

WHAT TO WATCH:

- President Obama meets with Iraqi PM Nuri al-Maliki at White House

- U of Iowa holds news conference on results of latest Hawkeye Poll of likely Republican caucus-goers, 10am

- U.S. Deputy Secy of Energy Daniel B. Poneman travels to Taipei

- U.S. online holiday spending up 15% to $24.6b Y/y: ComScore

- Google Chairman Eric Schmidt speaks at Economic Club of Washington, 12:30pm

- Lehman said to prepare $1.3b bid for Archstone stake

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

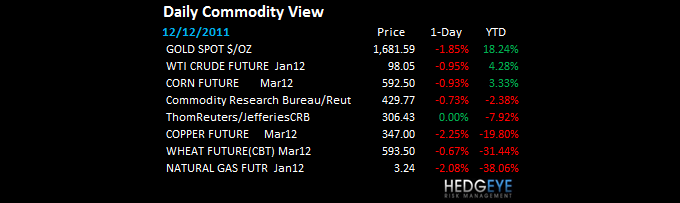

COPPER – the Doctor is ill this morning, trading down -2.7% moving back into a Bearish Formation as Gold fails at $1743 TREND resistance ($1683/oz last) and Brent Oil’s TAIL remains broken ($110.11/barrel) – all this started breaking down again on Thursday morning after the ECB press conf call where it was clear that there would be no ECB backstop (bond buying).

- China May Add to Reserve-Ratio Cuts as Europe Exports Weaken

- Gold Drops to Two-Week Low in London as Dollar Gain Cuts Demand

- Oil Falls on Europe’s Debt Crisis as Moody’s Readies to Review

- Speculators Miss Oil Drop on European Debt Woes: Energy Markets

- Funds Cut Bets on Rising Food Costs to 27-Month Low: Commodities

- Whitehaven Agrees to Buy Tinkler Assets for A$2.72 Billion

- Copper Drops on Rising China Stockpiles; Europe Crisis Concern

- South African Platinum Drop ‘Unprecedented,’ JPMorgan Says

- Indian Mines Bill Before Parliament Seeks to Share Profits

- Peru to Hire Consultants to Review Stalled Newmont Gold Project

- Palm Oil Drops Most in Two Months on Higher Global Soy Reserves

- Copper Declines on Speculation Chinese Demand May Weaken

- Wheat Drops as Global Harvest May Reach Record, Boosting Supply

- China, India Vow Pollution Cuts in Biggest Climate Move

- Rubber Growers May Back Physical Market to Set Up Benchmark

- U.K. Gold Hallmarking Slumps as Retailers, Consumers Cut Demand

- China’s November Foreign Trade by Commodity (Table)

- Goldman Sachs Said to Back Former Barclays Trader’s Hedge Fund

- DuPont Cuts Profit Forecast on Weakening Electronics Demand

CURRENCIES

EURO – get the USD right, you’ll get the big beta moves generally right and that’s what’s shaking out there this morning with the EUR/USD testing 1.32 again. All European stock markets making consecutive lower-highs and now testing immediate-term TRADE lines of support (the only lines left) of 5845, 3071, and 15102 on the DAX, CAC, and MIB, respectively.

EUROPEAN MARKETS

ASIAN MARKETS

INDIA – all the Growth Slowing on the East side of the world continues - China (down another -1% to a new low last night, down -18.4% YTD) and India put up their worst Industrial Production print in 28 months last night (down -5.1% y/y) = Sensex dropped another -2.2% (crashing, down -23% YTD)

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Singaporeans Deny Conspiring Against U.S. in Technology Exports

- Speculators Miss Oil Drop on European Debt Woes: Energy Markets

- Dubai Sukuk Yields Rise as Debt Payments Loom: Islamic Finance

- Armed Clashes in Syria Leave Scores Dead in Anti-Assad Campaign

- Etihad Orders More Boeing 787-9s, 777s in $2.8 Billion Deal

- Syria’s Death Toll Mounts as Economic Squeeze Tightens

- Aramex Taps South African Market With Berco Express Purchase

- Egypt May Borrow Abroad to Bolster Economy, Prime Minister Says

- Mideast Sectarian Strife Is Symptom of Weak States: Noah Feldman

- Taqa Will Repay Remainder of 5.62% Bond at Maturity in October

- Bahrain Bank Lending Grows Helped by Personal Loans: Arab Credit

- Iran Wants OPEC to Adjust Output for Libya, Iraq Oil, Mehr Says

- BP Sees Pipeline Gas Price Moving Away From Oil Index in Europe

- Barcelona Faces Qatar’s Al-Sadd in Club World Cup Semifinal

- Iran Seeks to Decode Information Stored on Downed U.S. Drone

- Nakheel Says to Pay 10% Profit on Islamic Bonds on Time

- Arab States May Suffer 24% Foreign-Investment Slump After Unrest

- Alstom Signs EU400m Contract for 728mw Power Plant in Iraq

The Hedgeye Macro Team

Howard Penney

Managing Director