In our view sentiment is going to play a significant role in several restaurant stocks’ price action in 2012. For some of our Hedgeye Restaurants Alpha top ideas, in particular, sentiment is an important component or risk factor, as the case may be. Accordingly, we will be focusing more closely on sentiment going forward.

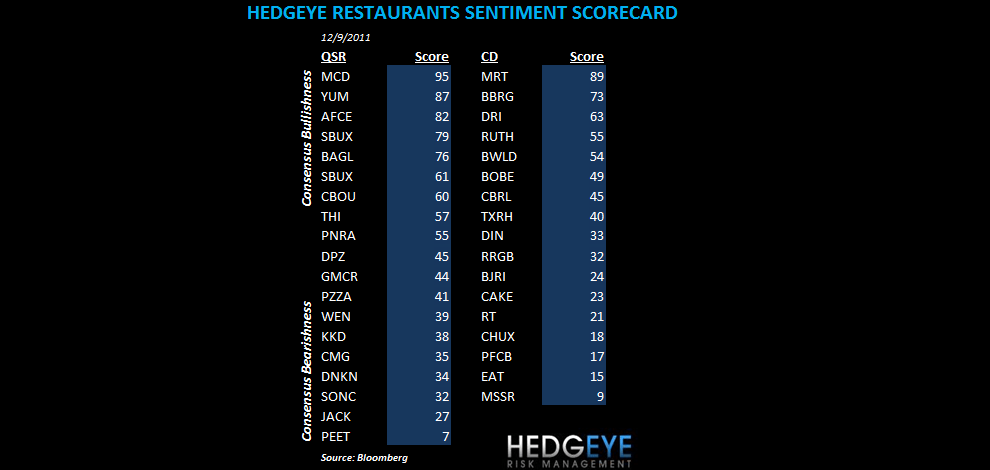

The Sentiment Scorecard, below, incorporates both sell-side and buy-side sentiment. As the table indicates, MCD and YUM are loved by the investment community. This has been true for some time, especially for MCD, and we don’t see sentiment turning alone as a catalyst for the stock, but it is worth bearing in mind that if the fundamental outlook for the company were to deteriorate, there is plenty of room for sentiment to turn bearish. MCD continues to be a favorite name of ours as it continues to take share with the latest monthly comps, reported last Thursday, indicated that global comps in November came in at +7.4% versus consensus at 5.1%. Even the bullish sell side (73% Buys, 0 sells), was not bullish enough going into the release. YUM has, over time, traded lower on China scares and our view is that these dips have made for opportune entry points on the long side. The company continues to drive strong sales in China, despite the slowdown in macroeconomic data in the country, and is also maintaining its appetite for seeking high-return growth opportunities in emerging markets. Both YUM and MCD are positive on Trade (3 weeks or less), Trend (3 months or more) and Tail (3 years or less) durations per our Hedgeye Restaurants Alpha list.

DNKN is not rated highly on the sentiment scorecard. The hype around the IPO shot the stock and the cash flow multiple embedded therein, to an unrealistic level. The stock has been trading poorly of late as investors have more closely scrutinized the growth strategy bulls are touting more closely. We are negative on this stock on all three durations (Trade, Trend, Tail).

WEN is a stock that is not viewed favorably by the investment community. We believe that there is a short-term opportunity for investors here with comparable restaurant sales running above the industry average. We are positive on WEN for Trade and Tail durations in the Hedgeye Restaurants Alpha list. Over the Trend, the stock may not perform well if a clear plan for remodeling the store base is not produced by management.

EAT is hated and we love both the stock and the fact that it is so hated. As investors, faced with the growing clarity around the improving performance of the Chili’s system, shed the emotional baggage that past experiences with the stock have burdened them with, we expect for a sea change in sentiment to buoy the stock price. We are positive on EAT on Trade, Trend and Tail durations. It should be noted that DRI registers a very positive reading on the sentiment scorecard and the company is experiencing significant difficulty in performing the current environment and its primary brand, Olive Garden, is hampered by an asset base in need of investment.

BWLD is a high conviction idea of ours on the short side. We have been publishing actively on this name, most recently last week on the significance of the Darden 2QFY12 EPS miss and its significance for BWLD going forward. There have been no sell ratings on the stock since 3Q09 when traditional chicken wing prices were up 51% and company same restaurant sales were running at 0.8% (3.1% for FY09). Please contact us for a copy of our latest work on BWLD; given the current fundamentals, the sentiment score is not taking into account the pressure the company will see in 1Q12 as wing prices squeeze margins and limit the viability of promotions as a means to driving comps. We are negative on BWLD for Trade, Trend and Tail durations on our Hedgeye Restaurants Alpha list.

In terms of short interest, the second table below shows that CAKE has seen a decline in short interest as dairy commodity prices have come down. Short interest as a percentage of shares out in EAT has been coming down but the absolute level, at 11.9%, remains above the industry average. GMCR is the standout in QSR, as sentiment continues to swing to the bearish side with the company’s ability to generate cash flow coming under scrutiny in recent weeks.

Howard Penney

Managing Director

Rory Green

Analyst