TODAY’S S&P 500 SET-UP – December 9, 2011

With US Stocks down for both November and December, Santa is going to have to have one heck of a rally in the next 2 weeks for us to be wrong. I am hearing that central planners are considering moving the date on Christmas however. As we look at today’s set up for the S&P 500, the range is 17 points or -0.03% downside to 1234 and 1.35% upside to 1251.

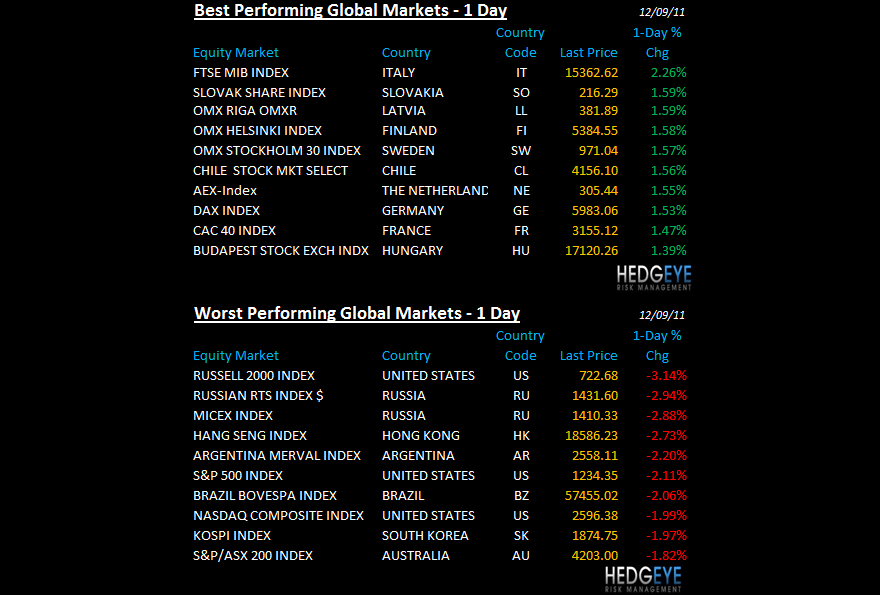

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2198 (-2370)

- VOLUME: NYSE 930.50 (-3.88%)

- VIX: 30.59 +6.70% YTD PERFORMANCE: +72.34%

- SPX PUT/CALL RATIO: 1.23 from 1.17 (+5.60%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 54.00

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 1.99 from 2.02

- YIELD CURVE: 1.770 from 1.880

GLOBAL MACRO DATA POINTS (Bloomberg Estimates):

- US Trade Balance (Oct); consensus ($43.7B)

- US Michigan Consumer Sentiment (Prelim.) (Dec); consensus 65.2

- Germany Nov final CPI +2.4% y/y vs preliminary +2.4%

- France Oct Industrial output 0.0% m/m vs consensus (0.3%), prior revised (2.1%) from (1.7%)

- UK Nov PPI; Output +5.4% y/y vs consensus +5.4%, prior +5.7%; Core output +3.2% y/y vs consensus +3.3%, prior revised +3.3% from +3.4%; Input +13.4% y/y vs consensus +13.2%, prior revised +14.3% from +14.1%

- Japan Q3 revised GDP +5.6% y/y vs cons +5.2% and initial +6.0%.

- China November CPI +4.2% y/y vs cons +4.4%. November PPI +2.7% y/y vs cons +3.3%. November industrial output +12.4% y/y vs cons +12.8%. November retail sales +17.3% y/y vs cons +16.9%.

WHAT TO WATCH:

- EU Backs $267 Billion for IMF as Draghi Hails Fiscal Pact

- Stocks Advance, Euro Rebounds After Summit; Italy Bonds Decline

- EU Leaders Drop Demands for Investor Write-Offs in Bailouts

- U.S. Money-Market Funds Cut French Bank Debt by 68% in November

- Toyota Lowers Annual Profit Forecast 54% After Thai Floods

- Cameron Wishes Euro Bloc Well as U.K. Negotiates Isolation

- Obama Defeats Romney in Global Poll Showing Republican Weakness

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Corzine’s ‘Intent’ Was to Head Off Possible Claims, Lawyers Say

- Gold Traders Most Bullish in Month on Debt Crisis: Commodities

- OPEC Deal May Falter on Saudi-Iran Supply Split: Energy Markets

- Oil Heads for Weekly Decline on Economic Concern, Europe Debt

- Extract Studies Options as $2.2 Billion China Takeover Looms

- Stocks, Euro, Italy Bonds Retreat as ECB Damps Debt-Buying Bets

- Gold Climbs in London on Concern About European Debt Measures

- Corzine, MF Global Executives Face Commodity Traders’ Lawsuit

- Malaysia’s Exports Rise More Than Estimated as Commodities Climb

- Gold May Drop 9.5% After Triangle Formation: Technical Analysis

- China’s Copper Output Declines to Five-Month Low in November

- Potash Corp. Reports Cutbacks at Two Saskatchewan Mines

- Extract to ‘Urgently’ Resume Partner Talks After China Bid

- Climate Talks Closer to Agreement on Plan with $100 Billion Aid

- Wilmar Beats China’s Cofco to Buy Proserpine Sugar After Vote

- INTL FCStone Starts Trading on LME Floor in Expansion of Metals

- Wheat Drops for a Third Day as Australia May Have Record Crop

- Indonesian Commodity Exchange Plans to Introduce Tin Contract

- Copper Declines in London After Car Sales in China: LME Preview

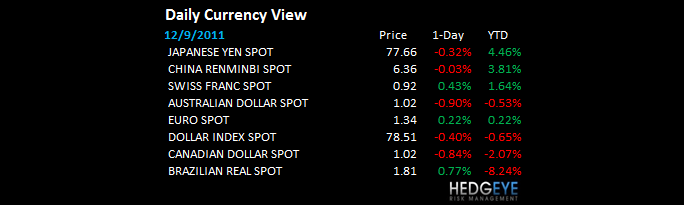

CURRENCIES

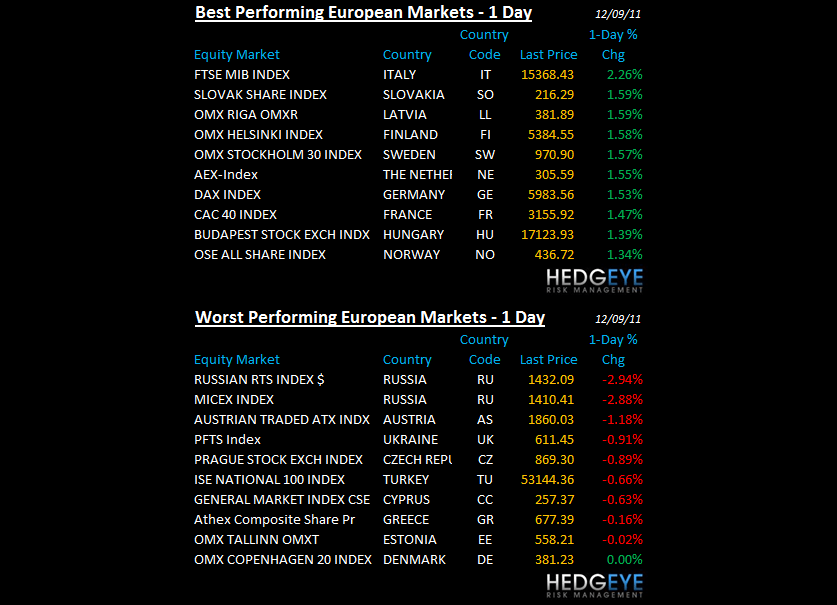

EUROPEAN MARKETS

GERMANY – the most important Global Macro factor to solve for when analyzing a country = GROWTH. The Bundesbank cut their Growth estimate huge this morning for 2012 to 0.6% (from 1.8% prior). European Stagflation is what kills Equity multiples, and there is no central plan that can stop gravity (Growth Slowing). Next line of DAX support = 5776.

RUSSIA – I’ve been up for 2 hrs and have yet to see or hear someone mention that the Russian stock market is crashing (that doesn’t mean it ceases to exist) – down -4.3% this morning and down -33.5% from YTD high confirming 2 Big Mac-ro calls we had yesterday: A) Strong Dollar and B) Cutting our Asset Allocation to Commodities back to 0%. Brent Oil snapped its TAIL line of $110.42.

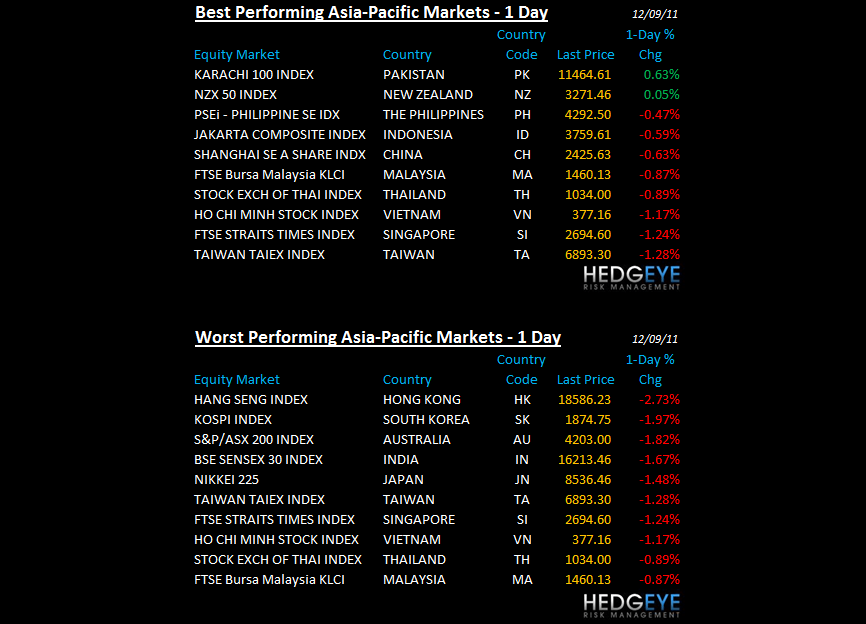

ASIAN MARKETS

CHINA – just a market mess in Asia overnight led by what we know - an acceleration in Growth Slowing in China – Industrial Production came in at +12.4% (lowest report since 2009) and inflation dropped, sequentially, inline with our model’s estimate at 4.2%. Deflating The Inflation (positive) will take time too. Chinese stocks hit a 33 month low (down -24.5% from YTD high).

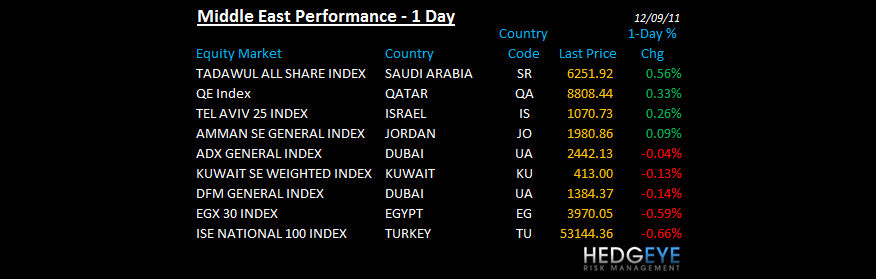

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Iran Shows Off Downed Spy Drone as U.S. Assesses Technology Loss

- OPEC Deal May Falter on Saudi-Iran Supply Split: Energy Markets

- Libya’s Bey Rebuilds After Feeding Rebels Who Killed Qaddafi

- Qatar May Consider Investing in Euro Bailout, Handelsblatt Says

- Malaysia Yields at One-Year Low Defy Sukuk Drop: Islamic Finance

- Gulf Keystone CEO Faces $6 Million Tax Fine Over Offshore Assets

- Luke Donald Bounces Back From Slow Start At Dubai World Champions

- Saudi Arabia Is in No Rush to Get New OPEC Quota, Naimi Says

- Oil at $150 Becomes Biggest Options Bet on Iran: Energy Markets

- Daily Mail (GB): Dubai World Championship leaderboard: Keep up to d

- Video Rekindles Mystery Surrounding Former F.B.I. Agent Missing in Ir

- Masdar City Offers Glimpse of Carbon-Neutral Future Amid Delays

- EU to Consider Additional Sanctions on Iran, Summit Draft Says

The Hedgeye Macro Team

Howard Penney

Managing Director