This note was originally published at 8am on December 02, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“I thought about running a marathon a long time ago, but I’m just not a runner.”

-Shannon Miller

I’ve woken up to some pretty ambitious central plans this week, but this morning’s caught my attention most – Angela Merkel is going to become a marathon runner.

“Marathon runners often say that a marathon gets especially tough and strenuous after about 35 kilometers…”

-Angela Merkel (speech to the lower house of German parliament)

While she doesn’t appear physically prepared to reach 35k on her own, looks (when gravity is being banned) can be deceiving. Central planners can try just about anything and have people who are paid by short-term stock and commodity inflations cheer them on.

Preparing for marathon, of course, requires some form of a diet, discipline, and sacrifice.

“The lives of a lot of French people are even harder after three years. Everybody has had to make an effort; everybody has had to make a sacrifice… it’s been a genuine revolution that’s begun.”

-Nicholas Sarkozy (speech yesterday in France)

Never mind the last 3 years of French hardship. French and German bankers have been sacrificing 3 hour lunches for conference calls with La Bernank for the last 3 weeks. Convincing the Great Depressionista that we should melt The People’s Savings again must be hard a hard life.

Back to the Global Macro Grind…

Life for real-time Risk Managers is hard too. God forbid none of us were born to this earth to constantly beat beta. But “god’s work” might have a different outlook than the 2 and 20 plan.

This, of course, like most things in human history, has happened before. The inability for asset managers to beat beta that is …

After Japan tried their 3rdand 4thquantitative and coordinated easing (and their stock market continued to make lower-long-term highs), beta was all that was left. What do you pay a manager to earn you beta?

Volatility kills returns, fund flows, and economic growth. Right now, all 3 of these factors are as clear as the sun rising in the East to anyone who manages money or a business.

But… we, as an industry, continue to beg for the very thing that perpetuates economic and market volatility – Big Government Interventions. Be careful what you beg for. In the long-run, we might all still have to live with its unintended consequences.

This morning, across the board in Global Macro, we’re seeing the Correlation Risk ramp as the US Dollar falls. Correlation Risk, if you are long and short, works both ways. It’s always on.

Looking across the asset classes in my model and across my core 3 durations (TRADE, TREND, and TAIL) here’s what I see:

- SP500 moves to bullish TRADE (1233 support); bearish TAIL (1270 resistance)

- US Equity Volatility (VIX) moves to bearish TRADE (31.02 resistance); bullish TAIL (23.07 support)

- Global Equity Volume remains in a Bearish Formation (bearish TRADE, TREND, and TAIL)

- Chinese Equities remain in a Bearish Formation (closing down another -1.1% overnight and down -0.8% on the wk)

- Japanese Equities move to bullish TRADE (8344 support); bearish TREND (8706)

- Indian Equities remain in a Bearish Formation (BSE Sensex bearish on all 3 durations)

- Germany Equities move to bullish TRADE (5895 support); bearish TREND (6279 resistance)

- French Equities move to bullish TRADE (3074 support); bearish TREND (3274 resistance)

- Italian Equities remain in a Bearish Formation (predictable divergence versus German stocks)

- Brazilian Equities move to bullish TRADE and TREND after cutting interest rates

- Commodities (CRB Index) remains in a Bearish Formation with TREND resistance = 321

- Oil (Brent and WTI) are now back into a Bullish Formation (inflationary, big time)

- Gold scales back into a Bullish Formation with TREND line support (was resistance) = $1743/oz

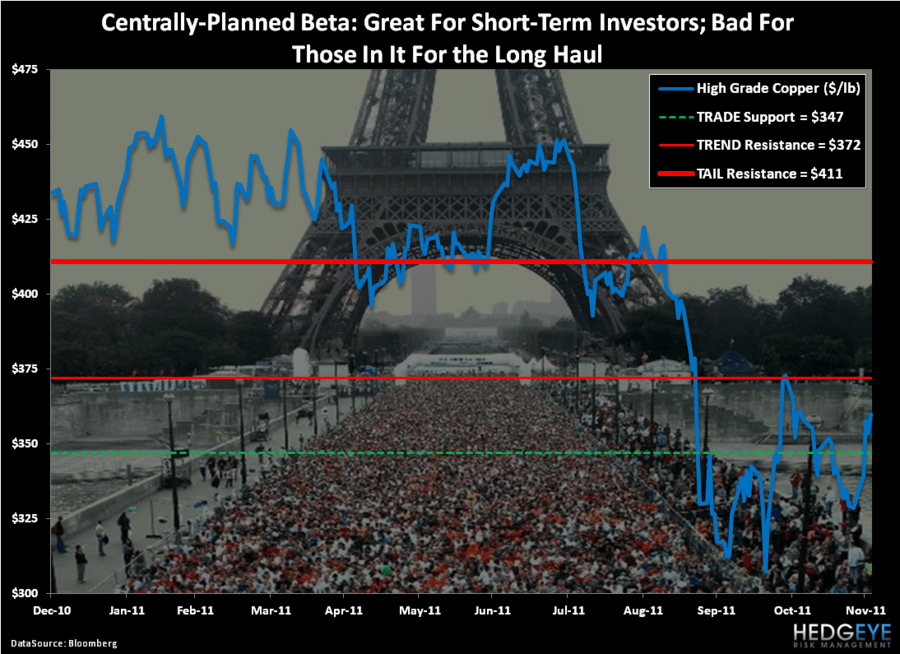

- Copper moves to bullish TRADE ($3.47 support); bearish TREND ($3.72 resistance)

- US Bond Yields are testing a TRADE line breakout (2.12% is the TRADE resistance for 10-year yields); bearish TAIL

All the while, the driver of all this Correlation and Duration Risk remains the US Dollar Index. With the US Dollar being debauched by Bernanke this week (down -1.8% on the week to $78.21), that’s why you see all these immediate-term TRADE breakouts in the aforementioned market prices.

But, Cher Bernank, a TRADE does not a sustainable economic TREND or TAIL make. Neither does an overweight and overleveraged economy sprinting out of the money printing blocks for the 1st three miles of what will be a deleveraging and deflationary marathon.

My immediate-term support and resistance range for the SP500 is now 1233-1258. If this morning’s full employment report inspires you to chase beta, run like the wind.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer