McDonald’s sales are to be released on Thursday, December 8th, before the market open.

McDonald’s reported stronger-than-expected sales in October after an impressive 3Q. In October, comparable restaurant sales came in at +5.5% versus consensus expectations of +4.1%, according to Consensus Metrix. Europe was encouraging, coming in at +4.8% versus consensus of +3.4% despite the escalation of the European sovereign debt crisis intra-month. The U.S. exceeded expectations by the widest margin, printing a +5.2% versus the street at +3.7%. APMEA completed the hat trick of beats for the company with a +6.1% comp versus +4.3% consensus.

We will be watching closely for any commentary on the domestic business. October was a particularly strong month with core menu items as well as beverages driving sales. According to an article on the Restaurant Finance Monitor website, the beverage segment has been leading the industry in terms of sales. A large part of McDonald’s success this year has been the successful lapping of last year’s frappes and smoothies rollout. At the outset of the year, our bearish case on the stock was predicated on the company not pulling this off, given the need for more marketing dollars to be allocated to the core business as we moved into 2011. The company did, of course, manage to successfully lap the beverage rollout of last year and strength in that category has remained even after the summer months. Other aspects of the business are also improving as the company remodels domestic stores and expanding day parts. In terms of business in Asia, and China in particular, we believe that the major QSR companies like YUM and MCD were still seeing strong trends in Asia during November.

Compared to November 2010, November 2011 had one less Wednesday and one additional Monday. As a result, we would not expect a significant calendar shift.

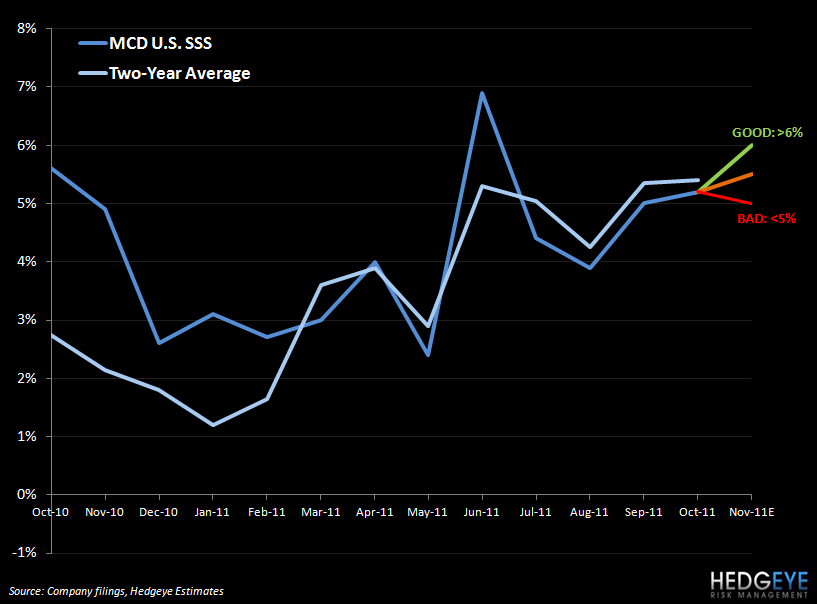

Below we go through our take on what numbers will be received by investors as good, bad, and neutral MCD comps numbers by region. For comparison purposes, we have adjusted for historical calendar and trading day impacts.

U.S.: facing a compare of +4.9% (including a calendar shift which impacted results by -1.8% to +0.1%, varying by area of the world):

GOOD: A print above 6% would be received as a good result, as it would imply a slight improvement in two-year average trends from October. Any improvement in two-year trends would, in our view, be encouraging because it would imply that last month’s stark improvement in trends has been sustained. September and October were exceedingly strong months in the U.S. with comps coming in at 5% and 5.2%, respectively. November faces a slightly easier year-over-year compare, but any improvement or continuation of the recent strength would be taken as a positive particularly as others in the restaurant group, like Darden, have clearly struggled recently.

NEUTRAL: A print between 5% and 6% would be considered neutral given that, on a calendar-adjusted basis, the midpoint of the range would imply trends roughly in line-to-slightly down from October. Given the outperformance in September and October, we do not believe a slight moderation would be received negatively given that comps would still be in the mid-single digit range and would still imply McDonald’s taking share from competitors.

BAD: A result below 5% would likely be received as a bad result given that it would imply that trends had decelerated from the September/October period. As strong as the company’s operational performance has been, the stock price has appreciated greatly (up over 9% QTD). It would seem that an inflection point in trends to the downside would likely bring the stock lower in short order.

Europe: facing a compare of 4.9% (including a calendar shift which impacted results by -1.8% to +0.1%, varying by area of the world):

GOOD: A print of 5% or higher would be considered a good result as it would imply two-year average trends roughly in line with October. Given all of the turmoil going on in Europe, it would seem that McDonald’s should be impacted at some point. That said, last month was an extremely strong month versus consensus so we are anticipating a print somewhere within our neutral range.

NEUTRAL: A result between 4% and 5% would be received as neutral, despite the slight deterioration in two-year average trends that the midpoint of that range implies. Given that austerity measures continue to impact consumers in Europe, a 4-5% print would still be indicative of a strong business, certainly relative to other plays on Europe.

BAD: A print of less than 4% would indicate a significant slowdown in trends for McDonald’s European business. Given the obvious concerns investors are having about Europe’s broader economy, it would likely not be difficult for sentiment around McDonald’s business in the continent to turn negative.

APMEA: facing a compare of 2.4% (including a calendar shift which impacted results by -1.8% to +0.1%, varying by area of the world):

GOOD: A print of 7% or higher would be considered good as it would imply trends slightly down from October but still at a healthy level of approximately 5%. Concerns about economic growth slowing in China are weighing on sentiment but we believe that the major US QSR chains are seeing strong trends in China at the moment.

NEUTRAL: A print of 5% to 7% would be received as neutral as, on a calendar-adjusted basis, the sequential change would be negative but the absolute level of the two-year trend would still be indicative of strong top-line trends.

BAD: A print of less than 5% would be received as a bad result as it would imply a significant slowdown in APMEA trends.

Howard Penney

Managing Director

Rory Green

Analyst