Darden is an impressive company and the investment community has liked the stock for some time. Issues highlighted in this morning's press release are important for Darden and other names within the industry.

Since he became CEO of Darden, Clarence Otis has been focused primarily on one thing: maintaining 4-5% unit growth. Buying LongHorn Steakhouse was one means to this end and, while the concept has proven to be successful, Darden paid a premium and may have incurred other costs indirectly. Despite the impressive infrastructure the company has built up, managing a large number of brands is difficult. The acquisition of Eddie V’s Restaurants, Inc. is another step in that direction. The company now manages seven brands.

As a public company CEO, Mr. Otis only has 80% of his time to manage the business after the basic duties of a public company CEO are fulfilled. That time is now spread between those brands and it not likely that any one of them has his full attention. Darden is a large company with many competent executives but the overall resources of the company are being stretched further as more brands are brought in to help sustain unit growth.

This morning’s press release, in our view, constituted an admission of two key issues for Olive Garden that can only occur, at a company like Darden, from management taking its eye off the ball:

- "At Olive Garden, we're addressing the erosion in one of the brand's essential attributes, its value leadership in casual dining. In working to re-establish that historical value advantage, Olive Garden more strongly emphasized containing check growth this quarter than in prior periods, and that was reflected in its promotion and in-restaurant merchandising tactics."

- “Our anticipated second quarter results reflect increased investment to rebuild guest counts at Olive Garden, as well as our decision to limit pricing across our portfolio of brands to levels that did not fully cover a meaningful increase in our year-over-year food costs"

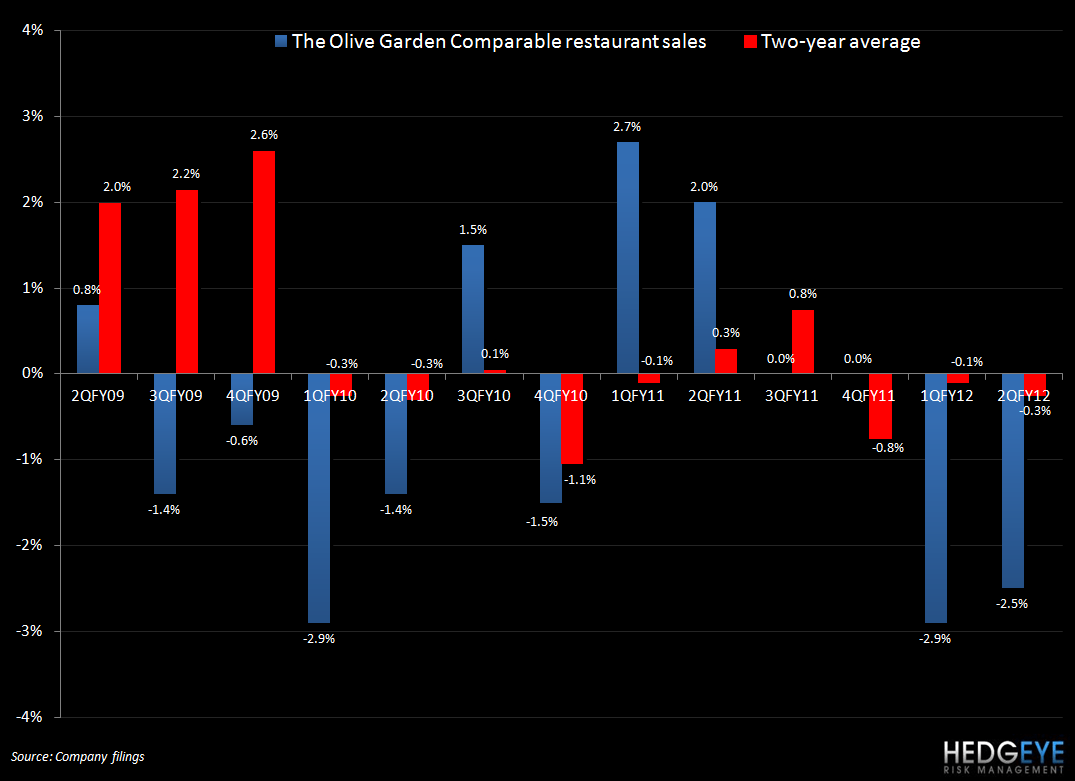

How can Olive Garden have lost its value advantage? We would posit that annual 2-3% menu price increases have been a factor. This is a pattern that is difficult to reverse. Promotions and in-restaurant merchandising tactics did not succeed in driving guest counts, as the press release says, because promotions as a strategy for driving the top-line are not sustainable. This unsustainable nature of this promotional strategy can be masked by favorable food costs but, as Olive Garden’s 2Q results show, a “meaningful” increase in year-over-year food costs can rain on the parade. Going forward, we do not anticipate the strategy mentioned in this morning’s press release as being a “silver bullet” for Olive Garden; the asset base is impaired and the turnaround will be a multi-quarter event, at best. During 2QFY12, Olive Garden saw trends deteriorating through the quarter. Red Lobster is another concept that is producing comps largely sustained by promotions.

As Darden continues to spread itself thin from a concept management standpoint, we believe it will be difficult to aptly address the issues facing Olive Garden and Red Lobster as they compete in what has become a very competitive industry.

In terms of the broader industry, we view this press release as having serious implications for BWLD going forward but EAT’s outlook is largely unaffected by the factors outlined by DRI. We would be a buyer of EAT today on any DRI-related weakness.

Howard Penney

Managing Director

Rory Green

Analyst