Revisiting An Important Theme: Margin Pressure

We noted a number of stories of late about Bank of America redeeming Trust Preferred Securities in exchange for debt and equity. This is the follow-through from their November announcement in the Q that they may issue as many as 400 million shares ($2.3B of capital at today's share price). We noted at the time that this flies in the face of management's repeated insistence that no capital raises are necessary. As we said then, we think this represents the beginning and not the end of their campaign to raise common equity.

Leaving aside questions of adequacy of capitalization for a moment, what are the NIM implications? For a number of regional banks, the upcoming retirement of the TruPS will be a significant event. So what are the numbers for Bank of America?

Not so good. While it is unclear how much equity the company issued, giving the company the benefit of the doubt and assuming that the full $2.3B was used to pay off TruPS at 8%, the savings to interest expense would be $47M per quarter. This would push 3Q's $10.701 billion net interest income (FTE basis) to $10.748 billion. With interest-earning assets of $1.841 trillion, the beneficial NIM impact is exactly 1 bps. In fairness, we get that the impetus here was not to enhance NIM; rather, the goal was to improve Basel III capital. Towards that end, we estimate that IF the company swapped the full $2.3 billion of common for TruPS, the benefit to Tier 1 common would be 13 bps, assuming RWA of $1.8 trillion (their target).

We have been negative on BAC's NIM since September (for details, please ask for our September 7th, 2011 slide deck and conference call). In that presentation, we outlined why Bank of America and the other moneycenter banks would face considerable NIM pressure over the coming quarters. The correlation between asset yields and a moving average of the 10-year treasury is very high.

Our NIM analysis from September showed that the best fit for asset yields was a trailing 4Q average of the 10-yr treasury. This relationship means that NIM pressure from August's rate plummet will be realized ratably over the course of the next three quarters, provided that rates don't fall any farther from here.

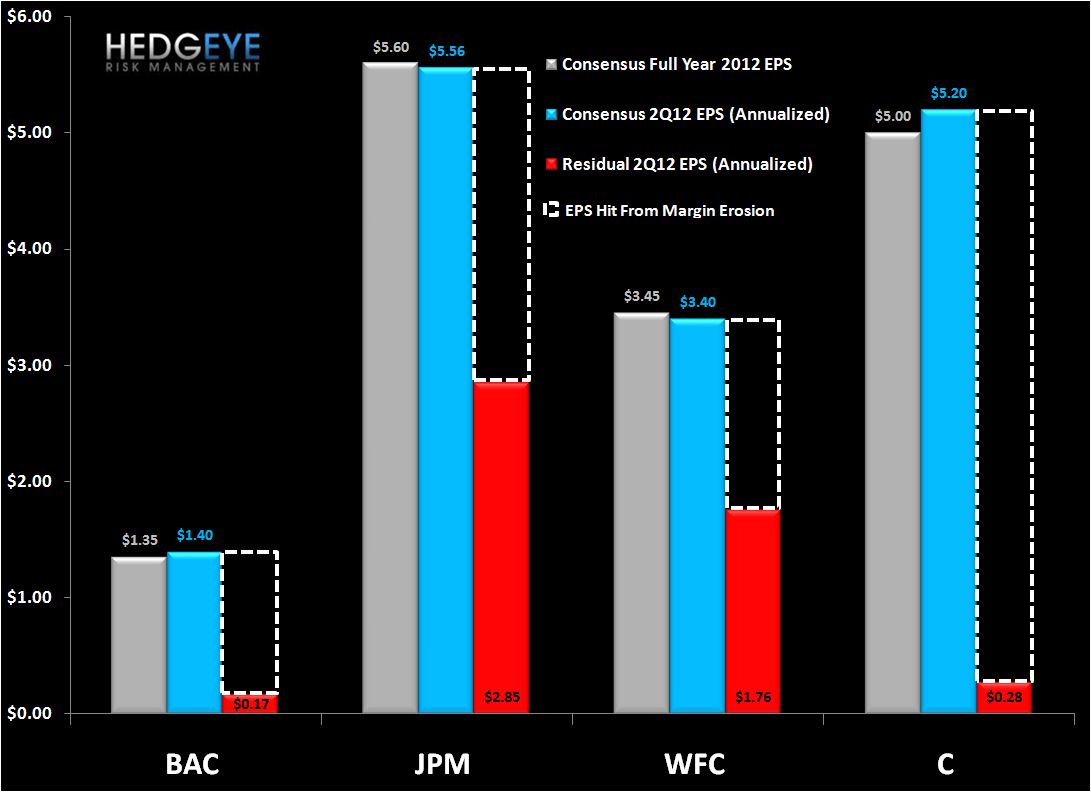

It's worth noting that an increase in interest-earning assets will serve to mitigate the effect of NIM declines on net interest income dollars. For those who believe this offset is sufficient, however, we would venture the following. Over the last twelve months, BAC's NIM fell from 2.69% to 2.31%, a decline of 14%. At the same time, their net interest income in dollars fell from $12.43B to $10.49B - a decline of -15.6%, or almost exactly the same proportion.

Ultimately, we expect the current environment to engender ongoing NIM pressure across the moneycenter banks, and Bank of America's small-so-far capital actions don't change that conclusion.

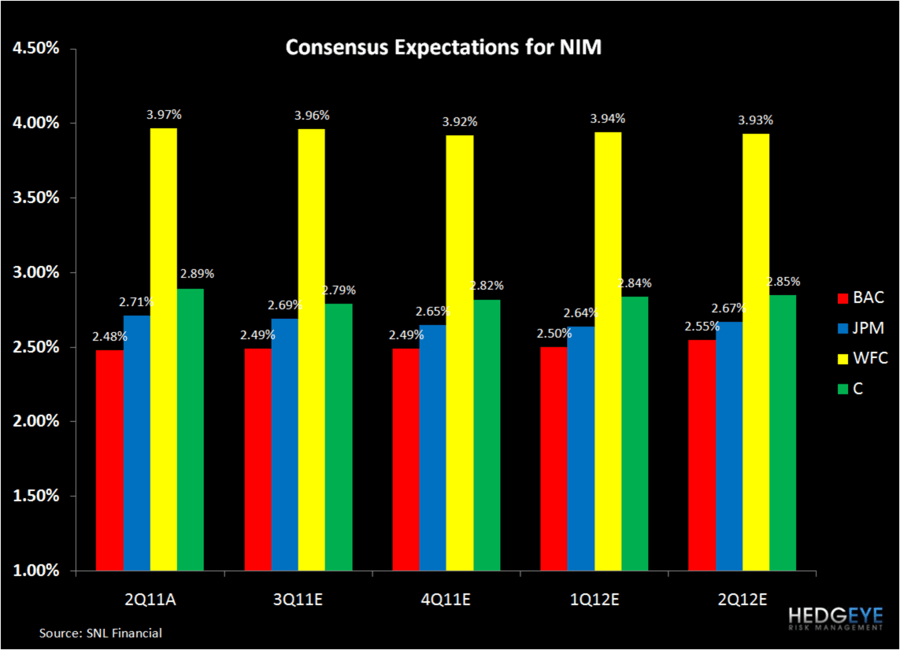

Below we show five charts from our September 7th presentation. Here's how our predictions shook out in 3Q vs. consensus and reality.

JPM reported 8 bps of NIM decline (vs consensus at -2 bps & Hedgeye estimate of -7 bps);

BAC reported 18 bps of decline (vs consensus at +1 bps & Hedgeye at -8 bps);

WFC reported -17 bps of NIM decline (vs consensus at -1 bps & Hedgeye at -9 bps);

C reported +2 bps of NIM increase (vs consensus at -10 bps & vs Hedgeye at -13 bps).

Joshua Steiner, CFA

Allison Kaptur

Trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.