“The world will seek the greatest possible salvage out of the wreck.”

-Irving Fisher, 1918

That’s a famous Irving Fisher quote Silvia Nasar uses to introduce Act II “Fear” in her wonderfully written economic history book – Grand Pursuit. She starts the Act with a chapter titled “War of the Worlds” where a young John Maynard Keynes obtained a critical WWI post at the British Treasury where he became the “go to-official for inter-Allied (read American) loans.”

“The Treasury’s task was not to only achieve “maximum slaughter for minimum expense” but also to finance the war without debauching the world’s safest currency or jeopardizing Britain’s supremacy as the world’s banker.” (page 198)

This week, as Keynesian bailout politicians attempt to make history through another currency debauchery, I thought I’d use the pre and post WWI period as a reminder of how The People used to think about a currency’s credibility and purchasing power.

After the Treaty of Versaille (1919) when the Germans, Austrians, and Hungarians were saddled with reparations debt, money printing became their only option – a political Policy To Inflate (sound familiar?). The economic stagflation (then hyperinflation) that ensued throughout Europe during the 1920s may rarely be discussed by Ben Bernanke and Tim Geithner, but it will never be forgotten.

As stock market futures hope for European resolve this morning, do not forget what the Germans will never forget. Hope is not a risk management process.

Back to the Global Macro Grind…

After the worst Thanksgiving week for stocks since 1932, followed by one of the best weeks for stocks in the last 3 years, this week’s “full employment and price stability” Act III by central planners should be exhilarating.

Here’s how the Global Macro calendar of catalysts looks so far:

- Monday: US Federal Reserve President from Chicago, Charles Evans, will speak on his short-term politicking for QE3

- Tuesday: my brother Ryan’s birthday

- Wednesday: whispers of the ECB Rate Cut decision (Thursday) should be all over the tape, weakening the Euro (again)

- Thursday: The Chinese report all of their economic data for November (should be weak, sequentially, across the board)

- Thursday/Friday: The EU Summit where central planners will struggle to explain who, precisely, is going to backstop more bailouts

To review hope/expectations: there is hope of a $100-200B bank bailout fund from the IMF that is effectively backstopped by Americans more so than it would be Germans (USA’s IMF quota is 17% and Germany’s 6%). There’s also hope that we see an Italian Job by Super Mario Draghi to backstop the EFSF bailout facility by the ECB.

Hope is not a…

Right, right, Keith. But the futures are up, so how are we supposed to chase and/or beat beta when we don’t know what these European central planners are going to do?

Good question.

As most of you know, this Globally Interconnected Game of Risk is changing. In Hedge Fund Industry 1.0 some of us could “get the call” on a big market catalyst like this, whereas today Wall Street 2.0 is struggling with a flatter playing field of who gets to know what and when.

Rather than looking for some Orange Jumpsuit Risk, I look to the currency and bond market Correlation Signals before I look to equity markets. Why? Primarily because both FX levels and bond yields have had it right for the better part of 2011.

Effectively, currencies and bond yields have been front-running stocks.

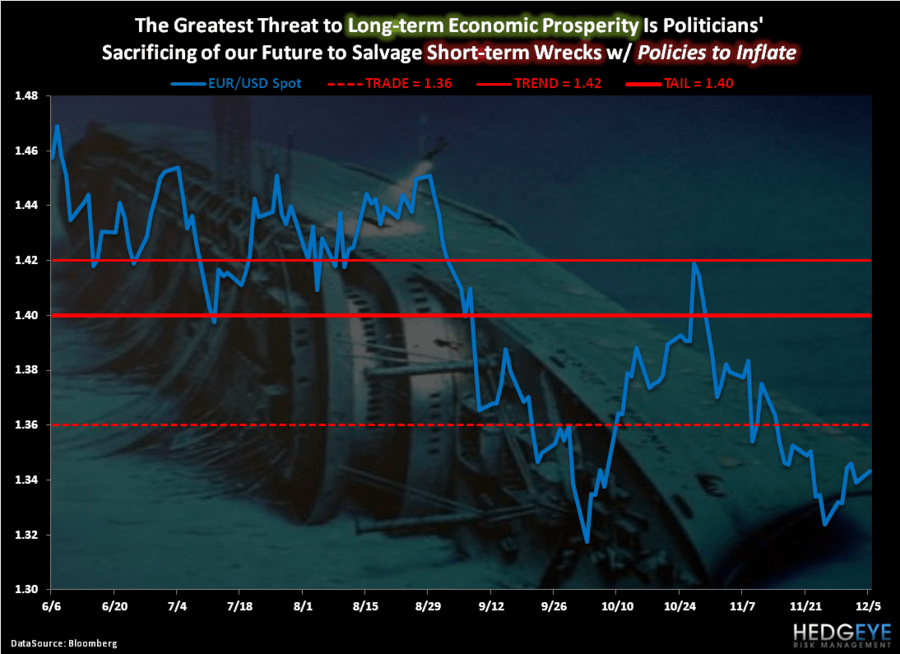

- FX: the EUR/USD’s TRADE and TAIL lines of resistance are $1.36 and $1.40, respectively.

- BONDS: the UST and European 10-year yield TRADE and TREND lines continue to confirm the same I see in the EUR/USD FX pair.

For US Treasury yields to signal that Growth Slowing is no longer going to be perpetuated by Piling-Debt-Upon-Debt, I’d need to see 10 and 30-year UST yields trade, sustainably, north of 2.12% and 3.22%, respectively.

For European Sovereign Bond yields to signal that we’re all free and clear from European bank insolvency on the order of magnitude that the likes of Lehman have never seen, I’d need to see Italian bond yields trade, sustainably south of 6%.

Salvaging The Wreck is going to take a very long-time. The greatest possible salvation we can all hope for this week is that stock markets don’t run-up too high ahead of another failed expectation on Friday.

My immediate-term support and resistance ranges for Gold, Brent Oil, France (CAC40), Italy (MIB Index), EUR/USD, and the SP500 are now $1, $109.34-111.89, 3074-3303, 149, $1.32-1.35, and 1, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer