TODAY’S S&P 500 SET-UP - December 5, 2011

With pre-market futures up, the most read headlines are all about European hope – hope is not a risk management process. As we look at today’s set up for the S&P 500, the range is 25 points or -1.65% downside to 1233 and 1.06% upside to 1267.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +630 (+1240)

- VOLUME: NYSE 872.80 (+1.98%)

- VIX: 27.52 +0.40% YTD PERFORMANCE: +54.04%

- SPX PUT/CALL RATIO: 1.67 from 1.54 (+7.87%)

CREDIT/ECONOMIC MARKET LOOK:

YIELDS – US Treasury Yields backed off hard at the 2.12% TRADE line of resistance on Friday and that level remains intact this morning with 10s trading 2.07%. The Bond market has had Growth right for all of 2011, and I don’t expect that to change this week.

- TED SPREAD: 53.34

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 2.05 from 2.11

- YIELD CURVE: 1.80 from 1.84

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: ISM Non-manufacturing, est. 53.8 (prior 52.9)

- 10am: Factory orders, est. -0.3% (prior 0.3%)

- 11:30am: U.S. to sell $29b 3-mo., $27b 6-mo. bills

- 12:10pm: Fed’s Evans speaks in Muncie, Ind.

WHAT TO WATCH:

- Fed and Eurozone national central banks may give loans to IMF to help Euro zone -- Die Welt

- Eurozone Dec Sentix index (24.0) vs consensus (22.5) and prior (21.2)

- Wal-Mart Canada tries to seize online sales for Holiday - Globe and Mail

- ECB lines up €1 trillion cash injection for the Eurozone economy -- Sunday Times

- Italy's PM Monti unveils €30B austerity package

- European leaders to meet in Paris today to work on another blueprint for fixing the debt crisis

- Service industries in the U.S. probably expanded in November to 53.8, fastest pace in six months

- Senate Majority Leader Harry Reid plans to offer a new proposal to extend payroll tax cuts and unemployment benefits that are set to expire this month

- Vice President Biden meets with Greek Prime Minister Georgios Andreas Papademos in Athens

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Merkel Heads to Paris as EU Leaders Seek Debt-Contagion Strategy

- Chow Tai Fook $2.8 Billion IPO May Top 2011 Hong Kong Offers

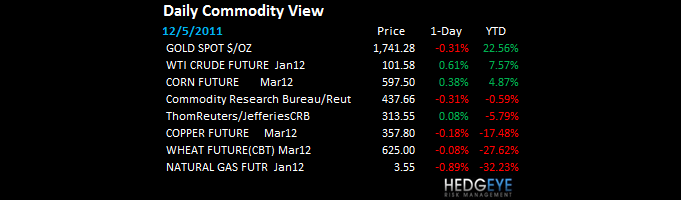

- Commodities Signaling Economic ‘Trouble Ahead’: Chart of the Day

- Economy Avoiding ‘Death Spiral’ Boosts Fund Wagers: Commodities

- Tinkler’s Aston Holding Deal Talks With Whitehaven Coal

- Hedge Funds Reverse as Iran Drives Oil to $100: Energy Markets

- Italy Approves 30 Billion-Euro Emergency Plan for Economy

- Oil Rises a Second Day on Iran Tension, European Debt Meetings

- Ternium Shareholders Lose Two Decades in Brazil Steel: Real M&A

- Gold May Fall as EU Leaders Form Plan to Enforce Budget Rules

- Cocoa Slump Signaling Hershey Chocolate Profit: Chart of the Day

- China, EU Maneuver to Avoid Blame for Expiring Carbon Limits

- Copper, Zinc Drop as China Industry Contraction May Cut Demand

- Anglo, Stung by Australian Carbon Tax, Fights South African Plan

- Aluminum Downside ‘Limited’ on Possible China Cuts: Goldman

- Australia to Allow Uranium Exports to India After Labor Vote

- Cameco’s Gitzel Says Uranium Supply Deficit May Loom After 2013

- Oil Rises a Second Day on Iran Tension, European Debt Meetings

- Palm Oil Gains for Third Day as China May Replenish Stockpiles

CURRENCIES

EURO – Get the EUR/USD right and you’ll get the market’s beta right. The Euro sold off intraday Friday and so did the US stock market; I think that’s how this ends on Thursday as an IMF backstop isn’t happening by then and hopes for the ECB backstop will only end up with another rate cut (which is Euro bearish). Big Euro resistance at 1.35-1.36.

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – despite Merkel having lunch today in Paris, Chinese growth and stocks refused to stop slowing overnight with another weak Services PMI print and the Shanghai Comp closing down another -1.2% (down -0.8% last wk). Thursday is also China economic data day for November, and that will be negative, so keep that catalyst in mind as markets try to rally ahead of EU Summit.

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Hedge Funds Reverse as Iran Drives Oil to $100: Energy Markets

- Oil Rises a Second Day on Iran Tension, European Debt Meetings

- Dubai Bank Provisions to Peak in Next Two Years: Arab Credit

- Louvre Delay Lifts TDIC Yields to 7-Month High: Islamic Finance

- Iranian Forces Shot Down U.S. Spy Aircraft, PressTV Reports

- Debt Crisis Threatens Global Warming Fight as Kyoto Fades

- Oil Rises a Second Day on Iran Tension, European Debt Meetings

- Qatar Petroleum, Shell Sign $6.4 Billion Petrochemicals Deal

- Emirates NBD Appoints Oppedijk as Interim CEO of Dubai Bank

- Abu Dhabi’s Taqa Said to Sell 5-Year, 10-Year Bonds

- Deutsche Bank Names Salah Jaidah as Chairman of Islamic Finance

- Saudis Won’t Immediately Start Pumping Oil From New Fields

- Iran Says It Downed U.S. Stealth Drone; Pentagon Acknowledges Aircraft Do

- Libya to Pump 1 Million Barrels a Day by End-2011, OPEC Says

- Iraq Considering Exxon Options, Not Sanctions, Upstream Says

- EXtra Starts Share Sale in Worst Saudi Arabia IPO Year in Seven

- Nakheel Posts First-Half Net of $134 Million as Projects Resume

- Syria: Fall of Bashar Al-Assad Will Bring War to Middle East, Warns Iraq

- Russia to Downgrade Diplomatic Ties With Qatar, Interfax Says

<CHART8>

The Hedgeye Macro Team

Howard Penney

Managing Director