The last time LULU saw inventory growth exceed sales growth, its behavioral response was far better than it should have been for such an immature company. We should see the same this time around.

Great example as to why a hyper-growth cult stock like LULU simply can’t print a decelerating top line, or a buildup in inventories/degradation in Gross Margins. As much as we’re fans of the TAIL story with LULU for so many reasons, these near-term factors simply don’t support a 40x+ p/e.

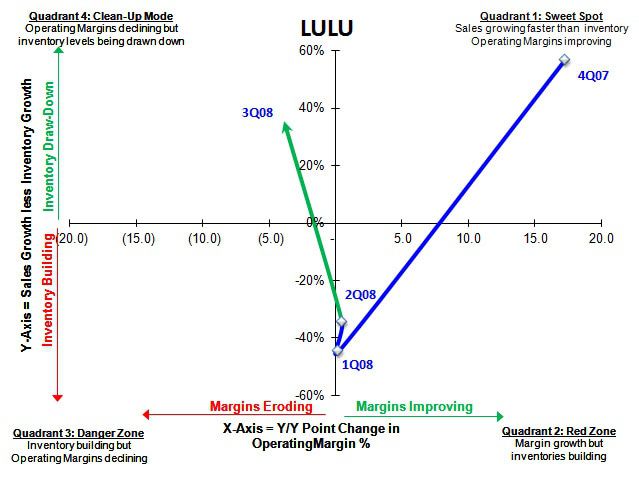

That said, Let me leave you with one thought. The last time LULU saw its sales/inventory spread go negative was in 1Q08. It was implementing new systems (getting out of the dark ages of Excel spreadsheets used to manage sales -- literally), and investing in its online platform. Back then, we were amazed (and impressed) to see such a sudden move from ‘inventory building with margins up’ mode (we like to call this the denial phase), up to the ‘take inventories down dramatically even if it hurts GM%’ mode. As one might think, hanging around in the lower right quadrant of our analysis (Denial) is a precursor to many a blow-up.

But only the smartest and best managed companies revert directly to the upper left (clearance) without turning a blind eye and living with down margins AND elevated inventories for a few quarters.

When LULU was presented with inventory issues back in 2008, it acted like a company that was 10x its size and age. It was an early cycle company acting like a mature company.

What do we have today? LULU is still an early cycle company, and there’s no reason we have to believe that it’s ‘maturity factor’ is any less today than it was 3 years ago.

We won’t fall on our sword and get involved here unless TRADE factors say the time is right. But the long-term TAIL call here is incredibly powerful.

Below is our December 2008 Note following up on LULU's Q3 2008 earnings:

12/11/08 12:37PM EST

LULU: Early Cycle Company Acting Mid Cycle-ish

The store growth slash overwhelmed the fact that the company managed its business like a retailer who has been in business for 30 years. As growth investors cycle out, this name is a gift.

What a flat-out weird quarter from LULU. Truly. Expectations were for a miss due to weaker comps, eroding gross margins, higher SG&A due to ERP investments, and inventory build. In actuality, the P&L looked better, the balance sheet looked exceptional, but store growth expectations were decimated. Bears definitely right on this puppy – though most probably for the wrong reasons.

Why do I say that LULU is acting like a mid-cycle company? Two main reasons…

1. The degree to which the company managed its inventories this quarter almost knocked me off my chair. Check out the SIGMA below. For 2 quarters straight, inventories built (and the multiple contracted), but then LULU took a massive V-shaped move to clean its balance sheet at the expense of margins (upper left quadrant). The key point here is that 80% of retailers revert to the lower left quadrant first – i.e. inventories building AND margins down – before taking any action. LULU is a step ahead. That’s unusual for a company like this where people so frequently question managements’ ability to execute.

2. The fact that LULU has secured only 5 real estate locations for next year on a base of 107 at year-end 2008 should scare even the most conservative growth investor at face value. Yes, it scared me as well. For most retailers, this behavior suggests management’s lack of confidence in its own growth platform. I don’t think this is the case with LULU. But it does show that the store growth strategy is part offense, and part defense.

a. The defensive angle is that company realizes that it does not live in a vacuum, and investing in a declining spending environment is risky business.

b. The offensive angle is that LULU fully realizes the leverage it holds with prospective landlords. LULU is taking a ‘come to Daddy’ approach to secure lower rents, which I like given that it will balance store-level economics as business shifts incrementally from 4-wall to .com.

c. The part of the growth equation that does not sit well with me is that a major theme next year, in my opinion, will be that the power brands that consumers want to succeed that also have the balance sheets to dominate the share-grab game and put weak competitors away will emerge the clear winners. LULU should be one of those. I’d rather see a more aggressive posturing here. They can afford it.

I still like the fundamental story here. Check out my 11/9 Post for the full thesis (I’m Finally On-Board with LULU”).