BUYING LIVESTOCK

Position: We are long livestock via the etf COW in the Hedgeye Virtual Portfolio.

This morning Keith went long the etf COW at $31.02 as “cattle correlations and supplies look better than most things in the commodities complex.”

SUPPLY

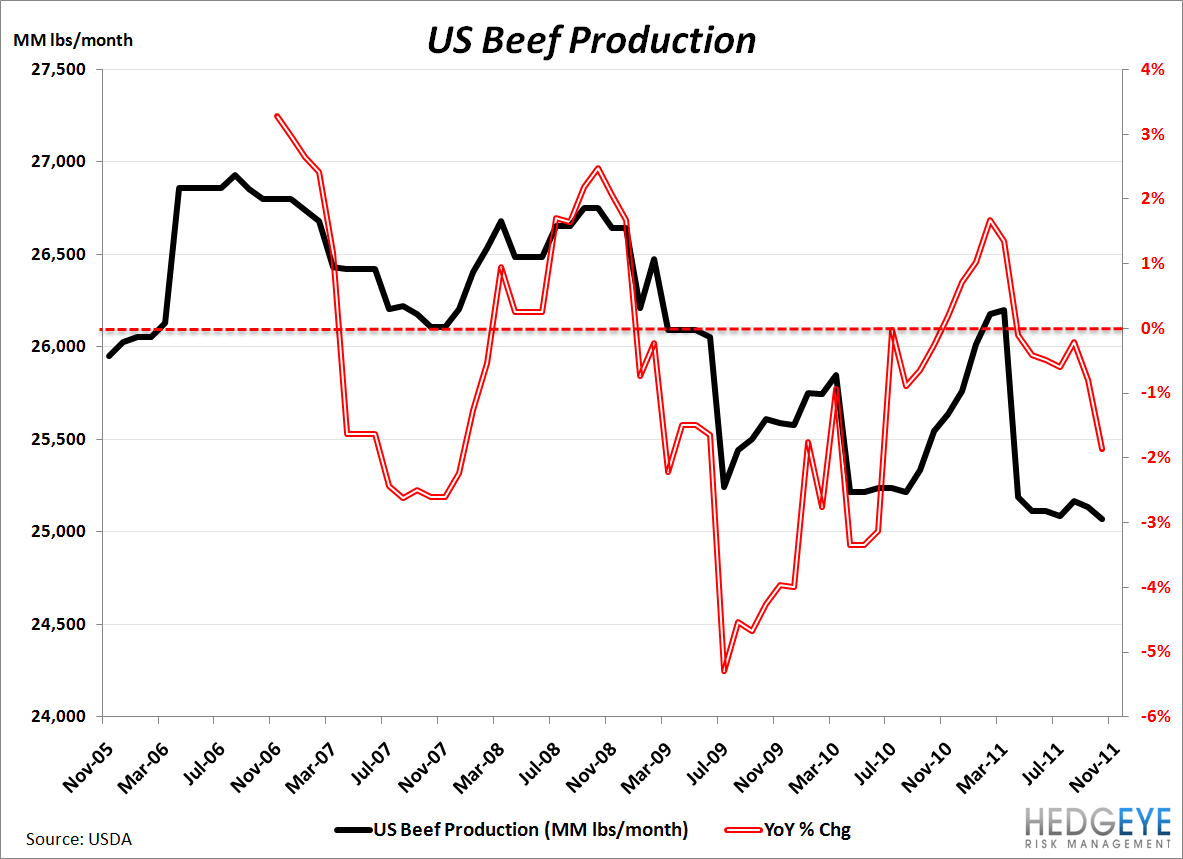

The largest (63%) component of COW is live cattle futures. Cattle futures and wholesale beef prices have launched higher in recent months as a combination of drought and high feed costs has led to the smallest calf crop in more than fifty years, with a smaller crop expected in 2012 (Cattle Network). This result has had an obvious impact on beef production: the USDA reported that production in November was 25,070 MM lbs – down 2% YoY and the lowest since 2004.

DEMAND

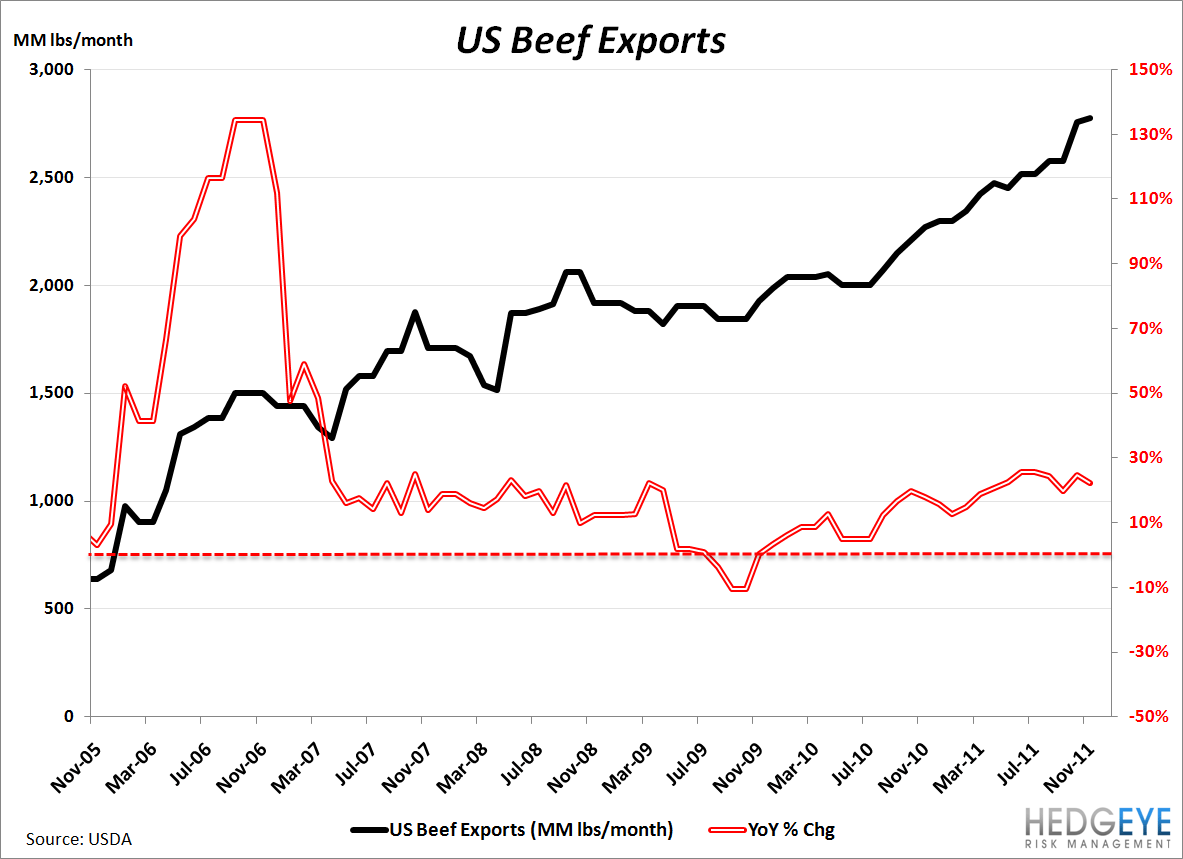

While domestic consumption comprises 80% of total demand for US-produced beef (Cattle Network), strength in the export market has been a tailwind to price, which shows no sign of abating as emerging market economies increase their per capita beef consumption. The US exported 2,775 MM lbs of beef in November, +22% YoY.

PRICE

The minority component (37%) in the COW etf is lean hog futures; both cattle and hogs are flashing positive correlations with the US Dollar on the immediate-term TRADE and intermediate-term TREND durations. With the USD in a Bullish Formation we are encouraged by the positive relationship developing between the dollar and livestock.

Correlations with USD Index

From a quantitative view, COW is bullish on the TREND duration with support at $30.22; and the underlying live cattle futures contract is entering a seasonally bullish season.

Daryl Jones

Kevin Kaiser