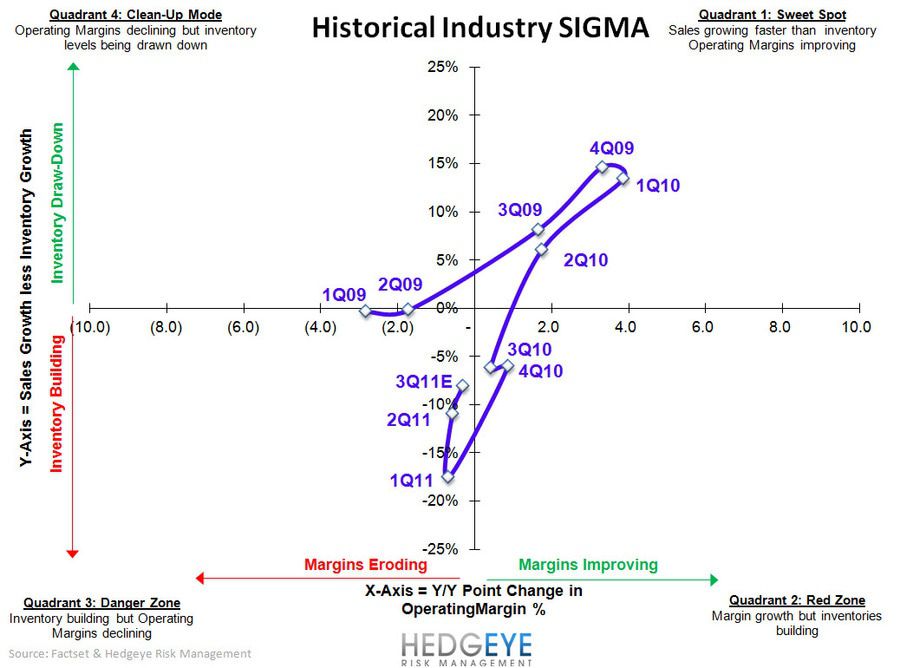

November sales coupled with several retail earnings reports out after yesterday’s close add a dose of reality to recent Black Friday bullishness. We expected fewer misses (9 companies missed to 11 beats) given the strength at month’s end, which suggests the first 80% of November was not nearly as impressive. We chalk this up to a large extent to consumers becoming increasingly conditioned to wait for the deep discounts associated with Black Friday despite some retailers getting an earlier start this year.

The takeaway here is consistent with last week’s post “Key 4Q Themes,” expect underperformance in the domestic mid-tier market as retailers get increasingly more competitive on pricing in an attempt to manage inventories. This was reflected in results at both JCP (-2%) and KSS (-6%), which came in below expectations. Not surprisingly, the few retailers that highlighted favorable inventory positions headed into the holidays (ROST & TGT) posted positive sales while KSS – expecting inventories up +LSD – did not. Volatility is picking up in retail and is starting to reveal a bifurcation between upward and downward revisions that we expect will continue through this quarter and into next year.

A few additional callouts in November:

- The High/Low-end performance spread has widened once again. Within department stores, SKS +9.3%, JWN +5.6%, M +4.8% were solid while JCP -2% and KSS -6.2% both came in lower than expectations in addition to continued underperformance at BONT -4.9%.

- Food/Grocery continues to outperform driving results at discounters. Retailers with exposure there (TGT up mid-teen and COST up LDD) fared better than most with similar results to last month i.e. COST betting expectations and TGT coming in light, though still up +1.8% and up +1.2% seq on 2yr basis.

- JCP missed expectations again just 2-weeks after reporting disappointing Q3 results. The company’s e-commerce sales were down -6.9% for the fourth consecutive month though it resulted in an improvement in the 2yr trend on top of tougher compares (+12% ly). With others like Macy’s Bloomingdales.com posting sales up +50%, JCP.com continues to grossly underperform. In addition, despite citing a competitive disadvantage to not opening until 4am on Black Friday, the company noted sales remained weak through the weekend. The reality is that it wouldn’t have made much of a difference.

- KSS posted the biggest miss of the month relative to expectations coming in -6% vs. +2%E with all categories coming in negative.

- From a regional perspective, it’s hard not to highlight the fact that virtually every single retailer flagged California or the west coast among the best performing regions. I can’t recall the last time I saw that much consistency.

- At a category level, footwear outperformed apparel by and large. This could indicate consumer’s response to higher prices at retail, but will be worth watching through the key holiday season as it could precipitate an acceleration in discounting.

- The magnitude of downward revisions out of several apparel companies reporting quarterly results after the close yesterday is also worth noting. GES & ARO kicked it off taking numbers down next quarter to $0.35-$0.38 from $0.45E and $1.03-$1.09 from $1.22E respectively. This morning GIL took next quarter down to a loss of -$0.40 from $0.28E and guided F12 EPS 40% below consensus expectations to $1.30 from $2.26E.

Shorts: HBI, GIL, CRI, JCP, SHLD

Longs: LIZ, NKE, RL, WMT

Casey Flavin

Director