THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

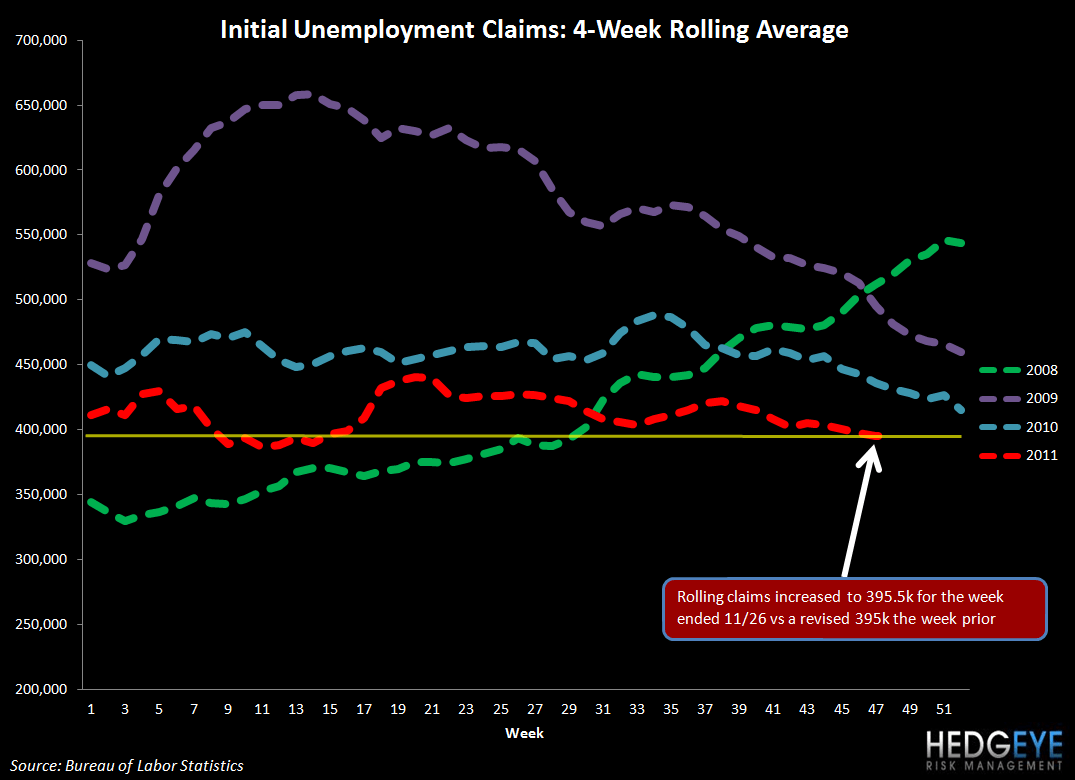

Initial Claims

Initial Jobless Claims came in at 402k versus survey 390k and a revised 396k the week prior.

Notes from CEO Keith McCullough

Yesterday was not a good day for me. You couldn’t have had a good day if you were having a good month.

- CHINA – when China started cutting in SEP 2008, they were serious about a serious slowdown in Chinese demand – this morning’s HSBC PMI print for NOV of 47.7 was awful (worst since 09) and Chinese stocks rallied less than they fell prior to the cut.

- ITALY – stocks look much different on the MIB index readings than they do on the DAX – so if you need to get paired off do it that way, but Italy failing at its first line of TRADE resistance (15,460) is a big problem. So is the Euro failing at 1.34 – both remain in Bearish Formations and the NOV PMI data across Europe supports the markets intermediate-term view as well

- DATA – plenty of it this morning – UK PMI hits 47.6 (lowest since 09), South Korean inflation rises sequentially to +4.2% NOV vs +3.6% OCT, Brazil cuts rates for the 3rd time in a row, etc – bottom line is that all of this remains much more a policy to inflate than it does equate to bare knuckled economic growth – there’s a difference – inflation slows consumption growth at $110/barrel.

Barring another central plan to blow out our industry’s hedges in the next few hours, US stocks should follow up their down NOV with a down DEC open.

KM

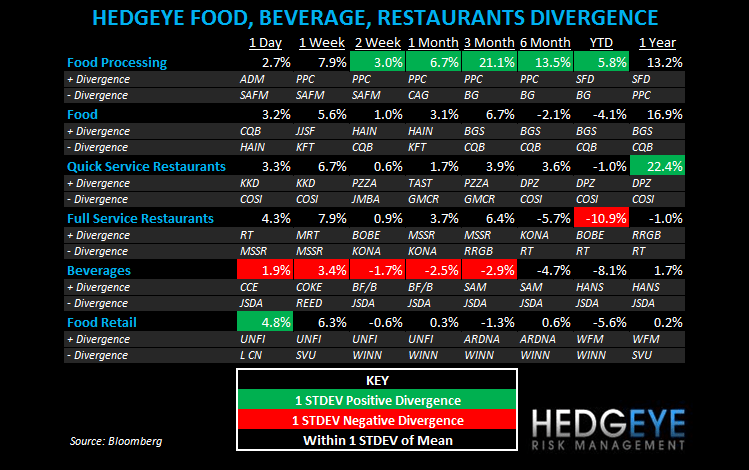

SUBSECTOR PERFORMANCE

QUICK SERVICE

GMCR: Green Mountain Coffee Roasters is facing a class action lawsuit being filed by purchasers of the company’s publically traded common stock. The Action alleges that, during the Class period, certain of the defendants systematically manipulated and strategically managed the company’s revenues.

MCD: McDonald’s is running a national discount offer with Living Social. Living Social is selling a booklet of individual vouchers for five Big Mcas and five French fries worth $26 for $13 on Thursday. The deal will be capped at one million vouchers.

CASUAL DINING

DIN: Dine Equity’s Applebee’s system-wide comparable restaurant sales were down -0.3% in the most recently reported quarter versus Chili’s company-owned comparable restaurant sales up 1.7%. Applebee’s is now taking a value-focused approach to driving sales. We are not confident that offering low prices for beef items will be the optimal strategy in 2012, given the likelihood that beef costs continue higher next year, but the prices are certainly compelling from a value standpoint. Details below:

- Sizzling Double Barrel Whisky Sirloins: Two 4-ounce steaks flavored with blackened seasoning, garlic and thyme over mashed potatoes topped with red peppers, mushrooms and onions caramelized in bourbon whiskey

- Sizzling Cajun Steak & Shrimp: A 7-ounce sirloin grilled with blackened seasoning and served over sautéed onions and red peppers, topped with blackened shrimp and Cajun gumbo with okra, with a side of red beans and rice with andouille sausage

The Sizzling line starts at $8.99, a price point company officials say has worked well as the brand strives to combine value and innovation to reverse slumping sales.

Howard Penney

Managing Director

Rory Green

Analyst