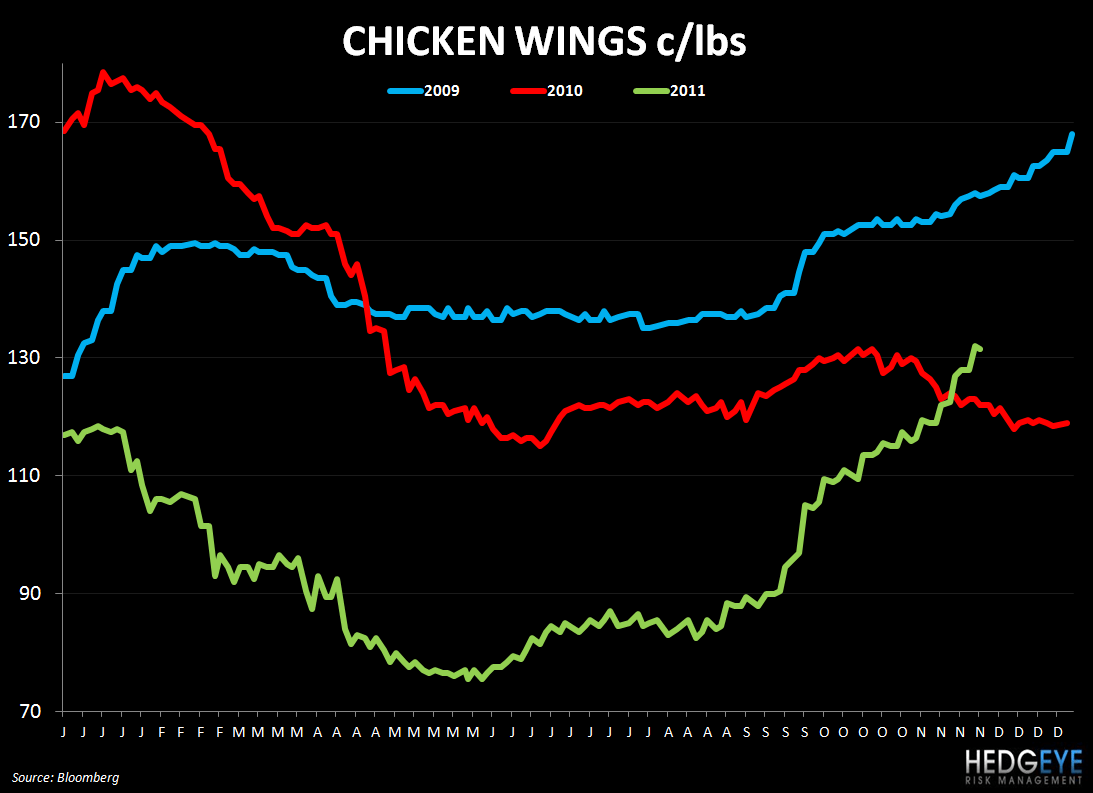

In general, the commodities that we monitor for the purpose of monitoring important trends for the restaurant and food industries posted mixed moves over the last week. Chicken Wings were up again as coffee and dairy costs came down.

STOCK THOUGHTS

Beef – WEN, JACK, CMG, TXRH

The outlook for beef in 2012 remains bullish from a price perspective and we continue to believe that restaurants with exposure to beef costs will see a dramatic increase in this item next year. As we have been highlighting for some time, smaller cattle inventories and healthy demand from emerging markets are indicating that prices could continue to gain despite the strong trend in 2011. It is important to note that while the export outlook is good, 80% of domestic beef production is reliant on consumption here in the U.S., according to cattlenetwork.com. If unemployment gets worse, consumers could begin to substitute beef for chicken. Today, at least, surging equity market seem to be reviving prospects for commodity demand but – while it is less clear what the markets will do in 2012 – the supply side picture is far more clear.

Chicken Wings – BWLD

Chicken wings continue to march higher. Last week, we highlighted commentary from TSN that suggested that food service companies may focus more on chicken in 2012. Given that processors such as SAFM are decreasing production, this could imply higher wing prices next year. Our stance remains that 1Q12 will be difficult for BWLD as high wing prices pressure margins and the company does not have the option of preserving margins while driving sales through promotion, as it did in 3Q. Higher wing prices do not necessarily correlate with EPS declines but, clearly, when prices are at extreme levels they become more relevant. We expect wing prices to be up 55% or 60% year-over-year in the first quarter.

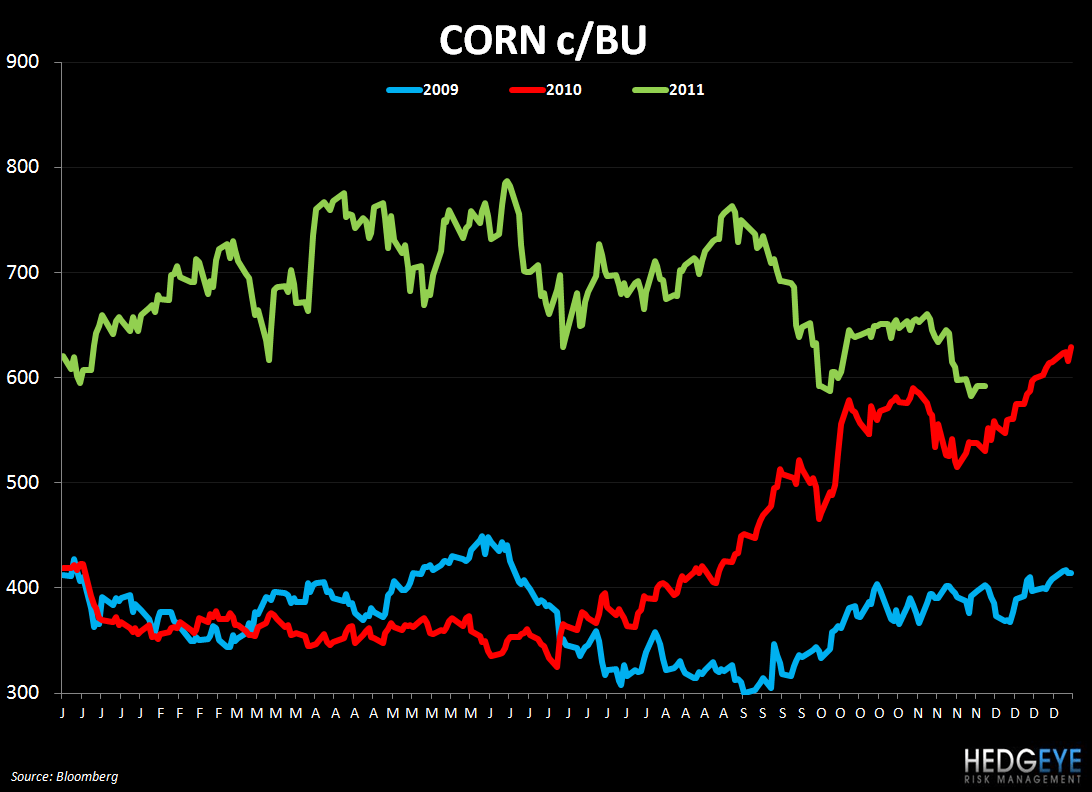

Grains – WEN, TXRH, CMG, PNRA, DPZ

Wheat and corn were up over the last week and continue to trade with a high inverse correlation to the US Dollar over the short-term. 92% of winter wheat in the 18 top producing states is emerged with 52% of the crop in good or excellent condition. The quality of the winter wheat is ahead of the previous year. Uncertainty around the debt crisis in Europe has been leading investors to exit grain markets, according to some commentators. CFTC data showed that noncommercial traders increased their net short position in wheat to the widest level since early 2006 during the week ended November 22nd.

Corn prices have traded lower on economic concerns over the last number of weeks but are trading higher today as equity markets gain following the action taken by the many of the world’s most important central bankers this morning. Corn prices remain up year-over-year, but there are several data points that suggest that downward pressure could continue. Brazil is set to releases some of its corn stocks next year to meet demand from meat producers that are currently combating higher prices. Ukraine is also stepping up its exports at these elevated prices levels. The country may ship a record amount of corn in November, according to some researchers. The International Grains Council also said, during the week, that the world corn harvest in 2011-12 will be less than expected even a month ago on a reduced outlook for harvests in the U.S. and Mexico.

All in all, declining wheat costs will be good for DPZ and PNRA while declining corn prices, if the trend continues, will be a positive for almost all industry players given how expensive the gain has become.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken – Whole Breast

Chicken Wings

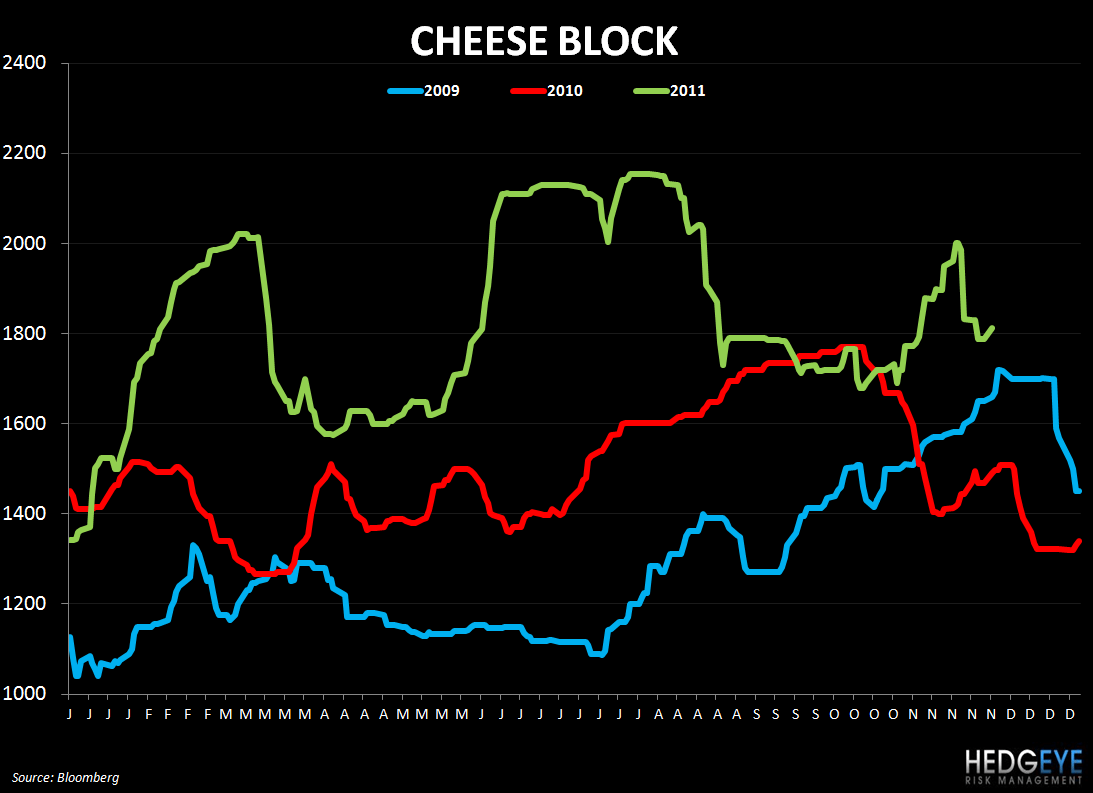

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst