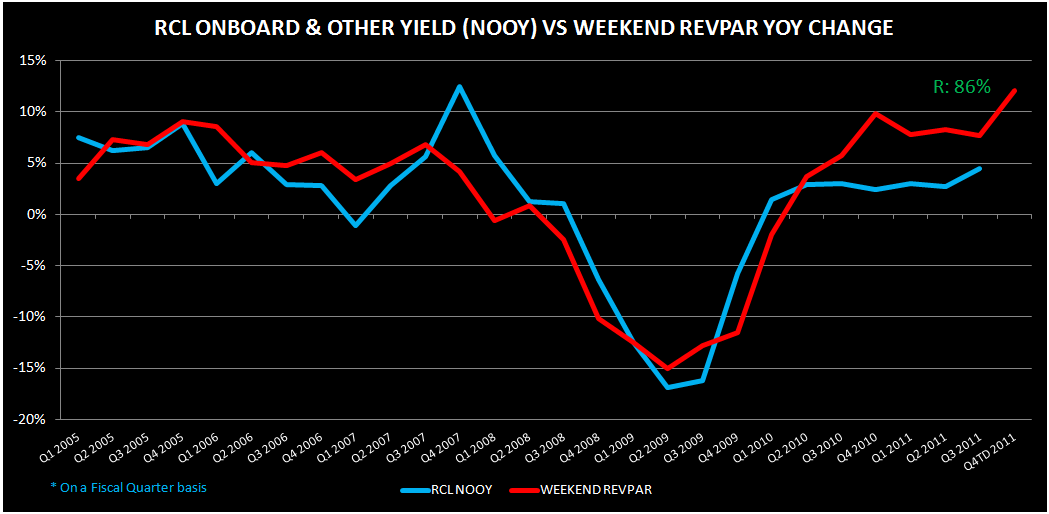

Solid weekend RevPAR data good for cruiselines.

Despite a difficult US macro environment, weekend REVPAR has been surprisingly resilient particularly over the last month. Why do we care? Our research has shown that net yields have a strong correlation (R: >80%) and onboard/other yields have an even stronger (R: >85%) correlation with weekend REVPAR.

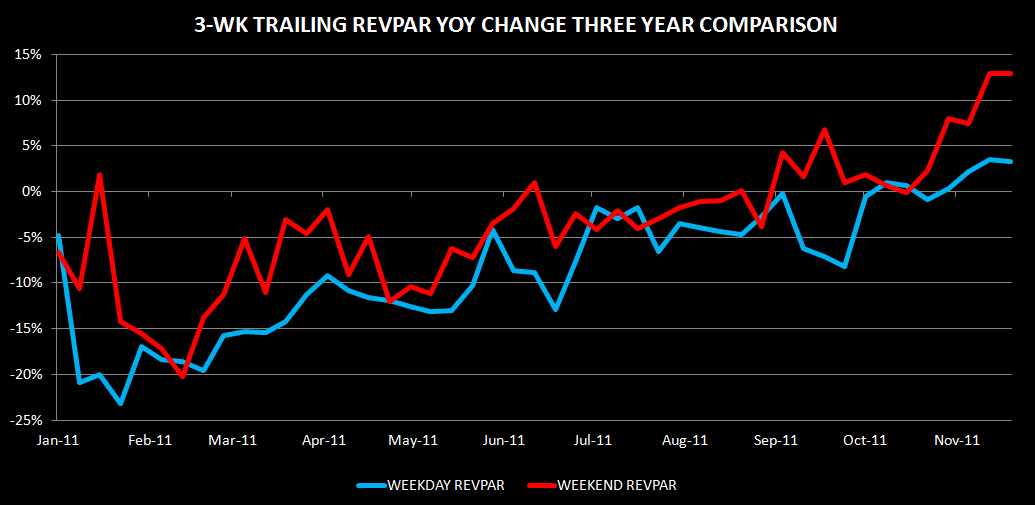

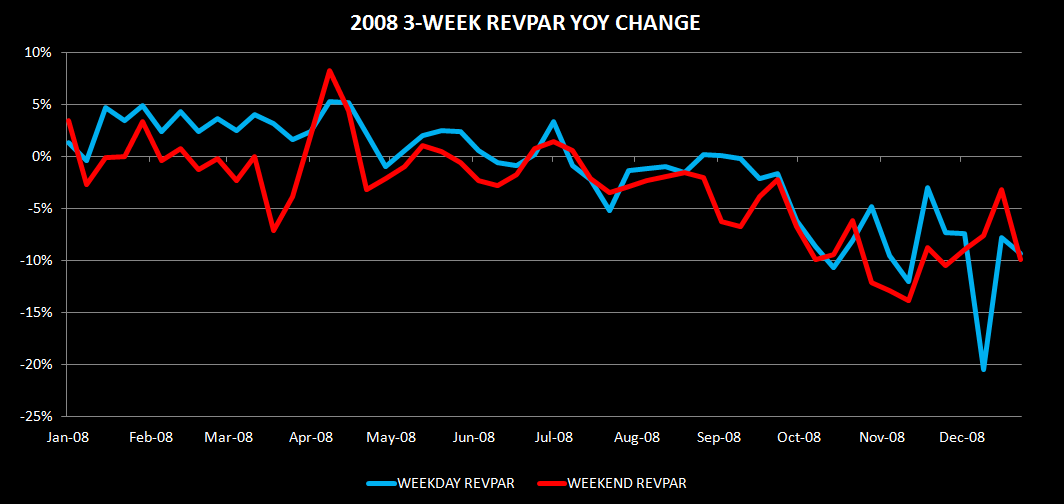

As the charts below show, not only has weekend RevPAR been strong, the spread over weekday REVPAR growth has recently widened on a 1-year, 2-year, and 3-year comparison. The outperformance can be attributed to weekend REVPAR underperforming significantly when the economy tanked (mid-October 2008 through early December 2008), so part of what we are seeing is a catch up. There is a calendar anomaly (Thanksgiving 2008) which will reverse some of the gains by Weekend REVPAR.

Either way, RevPAR trends remains solid, outperforming the broader economy, with leisure (weekends) doing even better.

Weekend REVPAR shows the strongest relationship with net onboard/other yields. The charts below display Q4 trending above 10% for Weekend REVPAR, which would be a sharp acceleration from Q3.

While we are concerned about the cruisers for FQ4 due to the uncertainty stemming from Europe, the North American business has been healthy. Furthermore, the momentum could carry into Q1 2012. Our pricing database shows Q1 2012 pricing in the Caribbean, South America, and Mexico has been quite strong. We will provide a pricing update in an upcoming note.