Key factors for December shopping in light of today’s strong Consumer Confidence reading.

Let’s add some context.

a) First off, let’s not forget that last year’s confidence reading was 59.7 and 62.4 in November and December, respectively, and peaked out at an impressive 3-year high of 73.1 by February of this year. That’s a great pre-and post holiday set-up, and is what drove 5.2% growth in Holiday sales last year.

b) For the past two months, however, everyone was scratching their heads trying to figure out why Retail Sales and PCE were both so robust (steady-mid single digit) in light of a precipitous decline in Confidence down to 41.2. No fewer than 20 people asked me “what’s the disconnect?”.

c) Now we’re back to declaring victory for Retail because Confidence rebounded to a 56.2 level. Perhaps it should have been there all along over the past two months? Seriously…Check out the chart below. It’s as if the government’s BLS and BEA numbers simply ignored the 3-month decline in confidence – or the other way around.

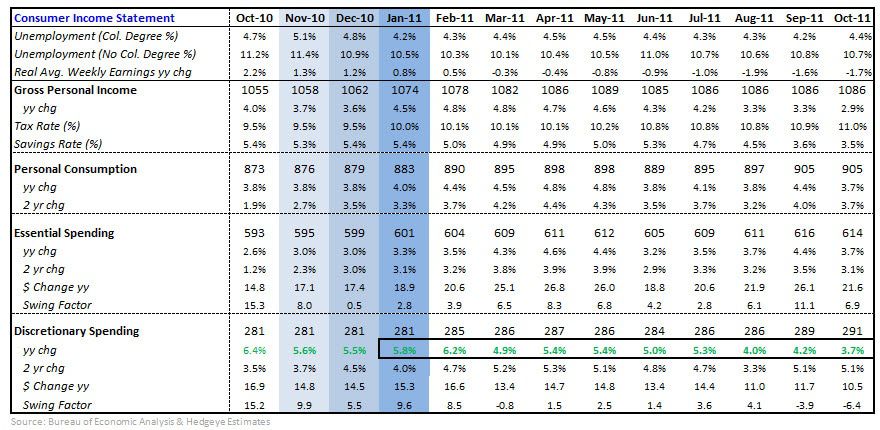

Aside from Consumer Confidence, here’s Hedgeye’s updated Consumer Income Statement along with some observations for the month of October (Note: this is VERY rear-view mirror as the data is on a one-month lag).

The punchline…

- Gross personal income slowed by 40 bps to 2.9%, with an interesting shift in mix. The unemployment rate went from 9.1% to 9.0%, but the rate for those with a college degree (that had otherwise been improving all year) eroded by 20 bps to 4.4%. The rate for those without a degree improved by 10 bps, and stands a full 50bps better than last year.

- Here’s a funny one for you…(if not sad), the consolidated personal tax rate came in at 11%, up 10bps sequentially, but a full 150bps higher than last year.. That’s a direct hit to consumption. So what did the consumer do? You guessed it. The personal savings rate came down by another 10bps, and is 190bps below last year. The consumer, as always, is finding room to spend. This rate is sitting at a 3-year low. It can always head towards zero, but the set-up into 2012 would be downright scary, and worthy of me getting overtly bearish on virtually every part of retail.

So what does this mean for Q4?

In our previous note “Retail: Key 4Q Themes” we highlighted 3 themes that emerged in the third quarter and will weigh heavily on Q4 execution:

- Driving Operating Expenses Higher: This was a common theme across all sub-categories -- especially among the poorer quality companies that need to catch up on years of deferred spending. Whether it be in the form of incremental marketing, added head count, or various IT improvements (e.g. mobile POS functionality), retailers are having to work harder and spend more to drive sales.

- Price Elasticity: Simply put, the better the product, the lower the elasticity. This has nothing to do with price. It’s all about perceived value.

- The Inventory Growth/Gross Margin Trade-Off: Five sequential quarters of sales/inventory erosion without commensurate decline in margins is absolutely unsustainable. There’s meaningful Gross Margin risk if the consumer does not comp the 5.2% holiday performance last year.