Positions in Europe: Short France (EWQ)

Keith shorted France via the eft EWQ in the Hedgeye Virtual Portfolio today with the etf broken on its immediate term TRADE and intermediate term TREND lines (see chart below).

France remains an important EU country in the crosshairs—constrained by fiscal pressures (debt and deficit) and a web of cross-country sovereign banking exposure, the two combined put pressure on the country’s AAA credit rating. Moody’s put France’s credit rating on watch back in October; last night La Tribune rumored that within 10 days Moody’s will place France's AAA rating as “negative outlook”; today Moody’s said it may cut EU subordinated bank debt (including a review of SocGen); and in late November Fitch Ratings warned that France’s AAA credit rating would be at risk if the crisis intensifies.

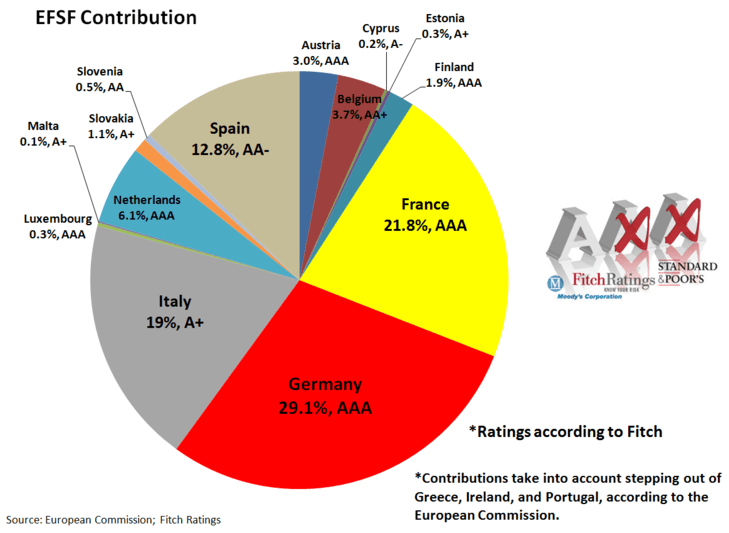

The likelihood of a rating cut comes as no great surprise to us. On 10/18 we penned a note titled “France is Going to Get Downgraded”, and made the important point that there exists an enormous outsized risk to the entire European bailout project for sovereigns and banks should France lose its credit rating: essentially the entire EFSF would be jeopardized, as France is the second largest contributor of collateral to the facility, at 22%, behind Germany at 29%.

From the fiscal side, France’s public debt as a % of GDP is likely to hit 88.4% this year, near the important 90% (and above) level that Reinhart and Rogoff outline in their seminal book This Time is Different as prohibitive to growth. Through austerity, the government hopes to bring down the budget deficit, forecast to hit 5.7% of GDP this year, to 3% in 2013, or in compliance with the EU’s Growth and Stability Pact. Nevertheless, there’s been great push-back to Sarkozy’s austerity programs, including the most recent €8 Billion in additional budget cuts, and we expect growth to come in below estimates.

On the banking side, France is the largest holder of Italian public debt ($106.8B) and private debt ($309.6B) of any country according to June BIS report, which compounds risk given Italy’s own debt imbalances and investor uncertainty around leadership in the wake of Berlusconi.

Early this month Sarkozy’s government revised GDP to 1.0% in 2012 versus a previous estimate of 1.75%. Politically, Sarkozy remains faced with high unemployment, at 9.2% (vs 7% in Germany), or 22.8% among the French youth, and unlike Germany does not have the ability to cushion slowing growth through exports.

Matthew Hedrick

Senior Analyst