Conclusion: There’s so much more to this story than the NBA. While there’s still much to like, the negative fundamental factors are lingering that the consensus might be missing.

It’s time for a serious update on Foot Locker. With two upgrades today – largely timed around the mitigated risk of a hit from the NBA strike – we think that people are glossing over some larger issues. Some are bullish, but for the first time in two-years, some bearish factors are starting to enter the equation. From a TRADE perspective (30-days or less), this name is still in a bullish formation and is one of the more attractive retailers based on Keith’s models. But as we head into 2012 and look at how the fundamentals are stacking up, our bull-case is no longer a slam dunk by any means.

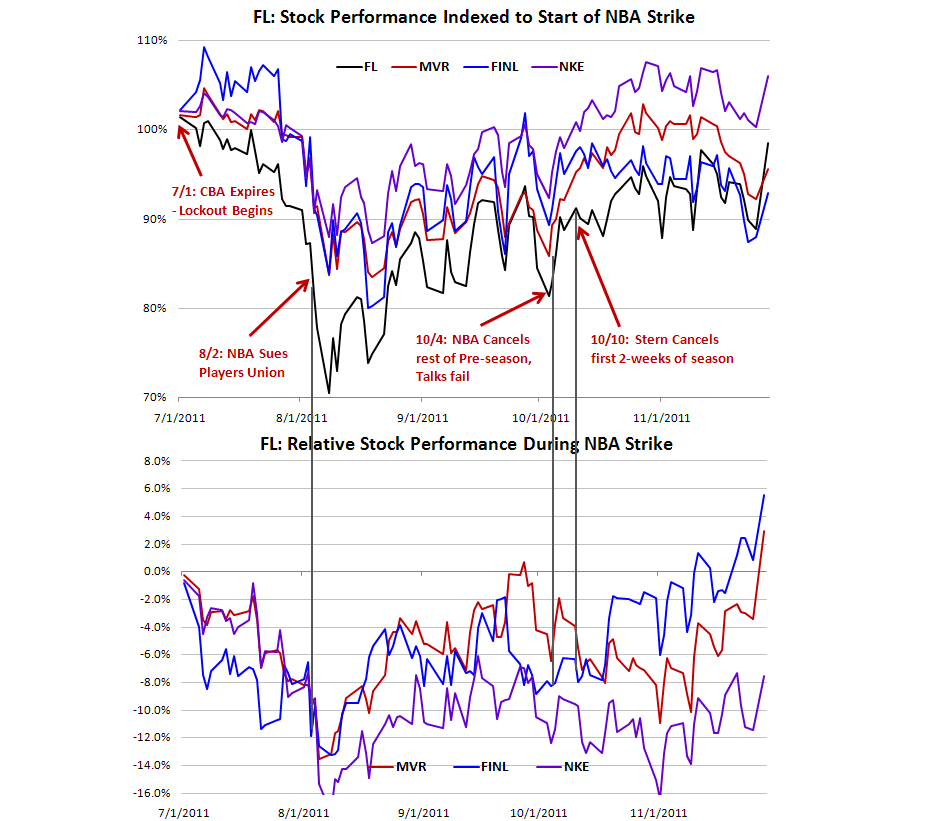

About the NBA strike… Ok, the risk is gone. I get it. But was there really any implied risk in FL from a strike in the first place? There’s a lot of noise week to week, but my answer is that – in aggregate -- the market has had this about right all along, and there really shouldn’t be a go-forward adjustment.

The timeline is important for a couple of reasons…

- The lockout started on July 1, but there was still perceived to be ample time to negotiate a deal. The stocks did nothing. But as talks cooled throughout July, FL underperformed the market by about 8%, and the broader retail space (MVRX) by 12%.

- Let’s not forget that the market simply melted down in August. On a relative basis, FL was a great place to be. By the time September 30 rolled around, FL had largely recouped all its losses (again, relative to the market and retail).

- Once the NBA cancelled the first two weeks of the season in October, the stock stalled, but only gave up 2-3%.

- But near the end of October, the market looked into the quarter, the health of its inventories, comp sales, ability to side-step basketball risk, and it was subsequently one of the better performing names in retail.

- Now we’re at a point where it has come full circle, and then some. It outperformed all relevant peers, comps, and broader benchmarks over the lockout period. Ironically, the only name that has performed better is Nike, which has greater basketball exposure. Yes, FL has printed good numbers in the interim, but at a decelerating rate relative to what we’ve seen in the past.

As much as Ken Hicks is running such a good ship and is rethinking the model, the fact is that the numbers simply get tough. We’ve had 10% comps over the past year, 40% EBIT growth, and seven consecutive quarters of improvement in the sales/inventory spread. It’s worth noting that over this precise seven quarter period, FL has beaten every quarter by a weighted average of 32%.

So what now? Product costs from the Nike’s of the world (even if only Nike) are being passed through to a far greater extent, and anemic levels of product in broader athletic channels will be refilled (note order books for all brands). FL will have a harder time keeping inventories in check, which definitely jeopardizes (peak) margins. Also, let’s not forget Europe, which is about 25% of sales, and is about 33% of EBIT. These stores are more productive and profitable than US counterparts. There’s a bit of a tug of war on the P&L between comp and SG&A, but net/net, the Euro had been a tailwind for the past 3-quarters. Economies aside…it becomes a headwind in 1Q13 (Feb 2012). The Olympics in London might be a jolt, but it will need to be a big one to offset the impact of a weaker pan-European consumer.

But might the company be a victim of his own success? Hicks delivered on his 5-year plan 3-years ahead of schedule. That in itself is so impressive – as has been the reward. Hicks made $2.475mm in cash last year ($1.1mm base with 125% target bonus – which he hit). That’s in-line with peers. The real kicker for him is in his incentive comp. He has 500,000 shares of restricted stock, and 900,000 outstanding options with strike prices between $10.1 and $15.1. The value of his vested equity at today’s $23 price is $8.6mm. The remainder vests by March 2013, and is worth approximately $21mm at today’s price. Every $1 fluctuation in FL’s price equals about a $1.2mm change in Mr. Hicks’ net worth. While he is a very accomplished retail executive, I’m going to assume that with a history at JC Penney and Payless, this kind of wealth creation is a huge deal for him, and something that he won’t let evaporate. This story is unlikely to crumble over the next 18 months when the rest of the options vest and the restricted stock balloon is up. But a risk that can’t be ignored is that these numbers are just so big and comfortable, and that he becomes complacent running a slow moving company in a business that is sub-par at best. In other words, that he becomes Matt Serra. Not likely, but we need to monitor it.

They’re hosting an analyst meeting in March to outline the new strategic plan. It might be foolish to bet against them. I don’t like betting against good management teams (it’s a long time since I’ve said that about FL). But numbers don’t lie, and the order of magnitude of additional changes will be difficult to engineer. Sales per square foot should break $400 this year, and prior peak flirted with $362. Margins are peak, and let’s not forget that this is a zero-square-footage-growth retailer with 33% exposure to Europe.

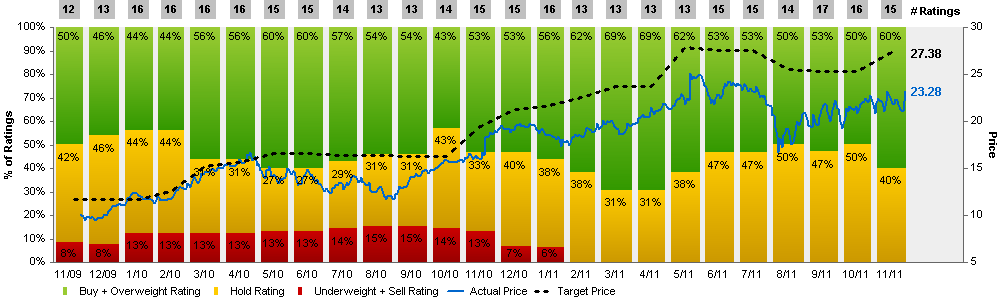

If the consensus numbers are right, and we actually think that they’re within a nickel of reality, then we’re looking at 14% EPS growth for next FY13, which is a sharp deceleration from the 61% FL is on track to print this year. The today’s two upgrades, there are officially no sells on the stock, and short interest remains relatively low at 6.1% of the float.

Brian McGough

Managing Director