“Schumpeter’s ambition was to replace static with dynamic economic theory.”

-Sylvia Nasar

Chapter V of Nasar’s “Grand Pursuit”, Creative Destruction: Schumpeter and Economic Evolution, was my favorite. While I am not sure if it’s politically correct to say that I like to creatively destruct things, I’m not sure I care. I’m not exactly a politically correct kind of a guy.

While Joseph Schumpeter ended up becoming a compromised man of government later in life, his early days of collegiate thinking were some of the most formative in all of modern economic theory.

Shakespeare wrote that youth is ‘ambition’s ladder.’ Being left to the devices of his own commoner’s experiences (“born in a small factory town” in the Czech Republic, page 171), Schumpeter defined “creative destruction” using common sense.

Back to the Global Macro Grind…

First, in order to contextualize this morning’s sharp squeeze higher across Global Equities, we need to take a step back and remind ourselves of what pricing of risk that we are bouncing from:

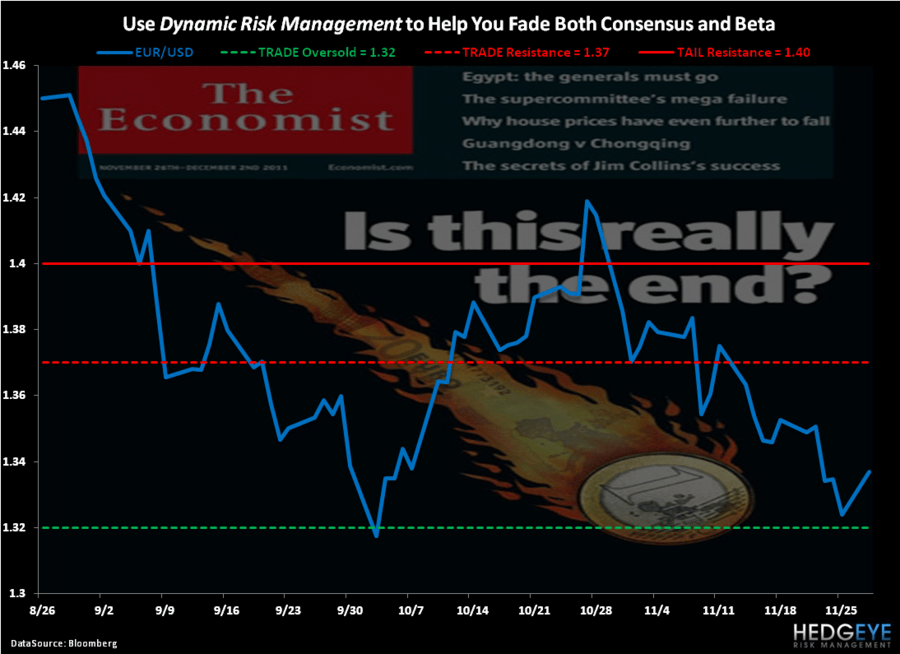

- US Dollar Index was up another +2.1% to close the week at a fresh Q4 high of $79.69 (up +9.2% from the April low)

- EUR/USD was down -2.2% to our immediate-term TRADE oversold line of $1.32

- US Stocks (SP500) were down another -4.7% week-over-week to close at a higher-YTD-low of 1158

- Italian, German, and French stocks were down -8.3%, -5.3%, and -4.7%, respectively (all crashing and in Bearish Formations)

- Asian stocks were down across the board again (Taiwan -6.2%, Australia -4.5%, Hong Kong -4.3%)

- CRB Commodities Index (19 commodities) was down another -2.2%

- Gold was down another -2.1% (in-line with the weekly US Dollar move up)

- Volatility (US Equities) was up another +11% to 34.47 (taking the cumulative rip in Bernanke’s “price stability” since April to +130%!)

- Long-term US Treasuries rose again as 10-year yields dropped to 1.96%

- Yield Spread (10s minus 2s) compressed by another 4 basis points week-over-week to 169bps wide

Dead cats bounce.

That would be a polite way of putting it actually. Last week was the worst week for US stocks during a Thanksgiving week since 1932 (not a good historical reference point, fyi).

In a world dominated by Keynesian policy makers perpetuating immediate to intermediate-term price moves in their respective fiat currencies, what we have left is called Correlation Risk.

The Correlation Crash (one of our 3 Global Macro Themes for Q4 alongside King Dollar and Eurocrat Bazooka) is born out of what the world’s fiat reserve currency (US Dollar) does relative to everything else.

If you get the US Dollar right, you’ll likely get mostly everything else right.

To be clear, correlations, like political careers, are not perpetual. So don’t expect this to stay with you for the rest of your born life. Just expect to have to deal with its implications in your portfolio again today.

Today’s immediate-term TRADE inverse-correlations to the US Dollar Index are as follows:

- US Stocks (SP500) = -0.94%

- European Stocks (EuroStoxx) = -0.94%

- Commodities (CRB Index) = -0.87%

- Bond Yields (UST 10yr) = -0.81%

Now if you are still using a static Marshallian or Keynesian economic model to manage risk, you’re probably not too happy with your 2011. What you should have done in the last 4 years is use this tremendous learning opportunity to evolve your risk management process into a dynamic one – a process that embraces the uncertainty associated with a Globally Interconnected Market’s last price.

Today’s uncertainty leads me toward one question – can this EUR/USD bounce extend itself this week so that the following immediate-term TRADE and TREND lines of resistance are overcome:

- SP (TREND)

- Germany’s DAX 5893 (TREND)

- France’s CAC 3089 (TRADE)

- Italy’s MIB 15135 (TRADE)

- Hang Seng 19443 (TREND)

- Shanghai Composite 2449 (TRADE)

- Japan’s Nikkei 8601 (TRADE)

- Brent Oil $110.61 (TREND)

- Gold $1726 (TRADE)

- Copper $3.45 (TRADE)

- UST 10-year yield 2.12% (TRADE)

- EUR/USD $1.37 (TRADE)

I know. Those are a lot of lines and a lot of durations. But that’s the point about Dynamic Risk Management – its construction needs to be multi-factor and multi-duration. And its principles need to adhere to one of the greatest mathematical discoveries since relativity (Chaos Theory).

“… just as Darwin had swept aside traditional with evolutionary biology” (Grand Pursuit, page 177), I’m very comfortable climbing Schumpeter’s ladder of creative destruction on Old Wall Street this morning. Change is good.

My immediate-term support and resistance ranges for Gold, Brent Oil, France’s CAC40, and the SP500 are now $1, 104.65-109.39, 2, and 1143-1195, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer