TODAY’S S&P 500 SET-UP - November 28, 2011

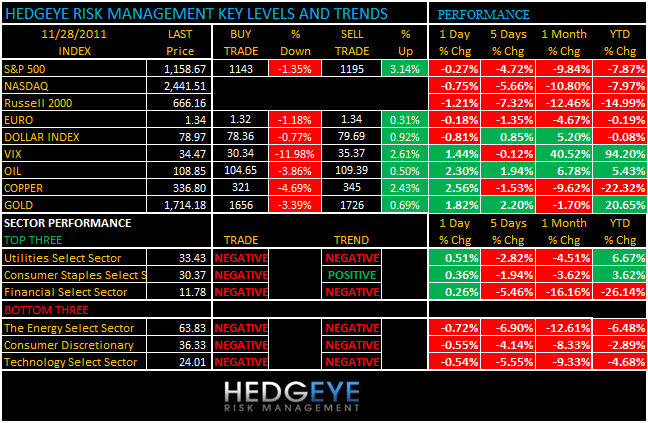

Don’t forget that last week was the worst Thanksgiving week for US stocks since 1932. The S&P500 would have to close > 1203 for us to not be selling on green today. As we look at today’s set up for the S&P 500, the range is 52 points or -1.35% downside to 1143 and 3.14% upside to 1195.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -385 (+1947)

- VOLUME: NYSE 441.77 (-49.57%)

- VIX: +34.47 +1.44% YTD PERFORMANCE: +94.20%

- SPX PUT/CALL RATIO: 1.88 from 2.16 (-13.09%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 50.78

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 1.97 from 1.89

- YIELD CURVE: 1.69 from 1.63

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: Oct. new home sales, est. 313k, prior 313k

- 10:30am: Nov. Dallas Fed Manufacturing activity, est. 5.0, prior 2.3

- 11am: New York Fed releases 3Q report on household debt

- 11am: Fed to purchase $4.25b-$5b in notes/bonds

- 11:30am: U.S. to sell 3-mo., 6-mo. bills

WHAT TO WATCH:

- U.S. retail sales up 16% to record $52.4b over Thanksgiving weekend; National Retail Federation. Cyber Monday takes place

- German Finance Minister Wolfgang Schaeuble urged fast-track treaty changes to tighten budget discipline to calm markets

- Biggest bond dealers in U.S. say Fed is poised to start a new round of stimulus, injecting more money into the economy by purchasing mortgage securities instead of Treasuries

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COMMODITIES – same Global Macro trade (Correlation Risk) that’s associated with the USD; what went down last week goes up this morning (with the USD down) – important immediate-term TRADE lines of resistance we are watching are Gold $1726 and Copper $3.45. If both fail there, both are shorts.

- Raw Materials Topping Equities With Growth Intact: Commodities

- Seaway Pipeline Creates Contango With Oil Glut: Energy Markets

- Ternium, Tenaris Buy $2.7 Billion Stake in Usiminas

- Oil Climbs to Highest in a Week on U.S. Sales, Syrian Sanctions

- Gold Gains as IMF Loan Report Helps Euro, ETP Holding at Record

- Oil Advances a Second Day on Economic Outlook, Syrian Sanctions

- Copper Advances Most in Two Weeks on Record U.S. Holiday Sales

- U.K. Power Use Drop ‘Symptomatic’ of Economy: Chart of the Day

- Baosteel Cuts Costs With Biggest Corporate Dim Sum: China Credit

- BHP Billiton Names Kerr to Succeed Vanselow as CFO

- Ruble Bears Lifting Swap Rates Lure Uranium One: Russia Credit

- Commodities Advance on Signs Europe Seeking to Contain Crisis

- Codelco Cuts 2012 Copper Fees to S. Korea After China, Japan

- Posco to Post Record Stainless Steel Production This Year

- U.K.’s Osborne Said to Aid Steel, Aluminum Producer Energy Costs

- Iraq Signs $17 Billion Gas Agreement With Shell, Mitsubishi

- China Sharpens Food-Safety Fight, Condemns Man for Contamination

- Wheat, Corn Gain on Optimism European Leaders May Stem Crisis

- Gold Gains as Dollar’s Decline May Spur More Investment Demand

CURRENCIES

EURO – immediate-term TRADE oversold at 1.32 is as oversold does (we covered our Euro short there) – now you get the bounce back up toward a lower-high of immediate-term resistance (1.34). Take your time with this and use the USD as your front-runner to fade the Global Macro market’s beta

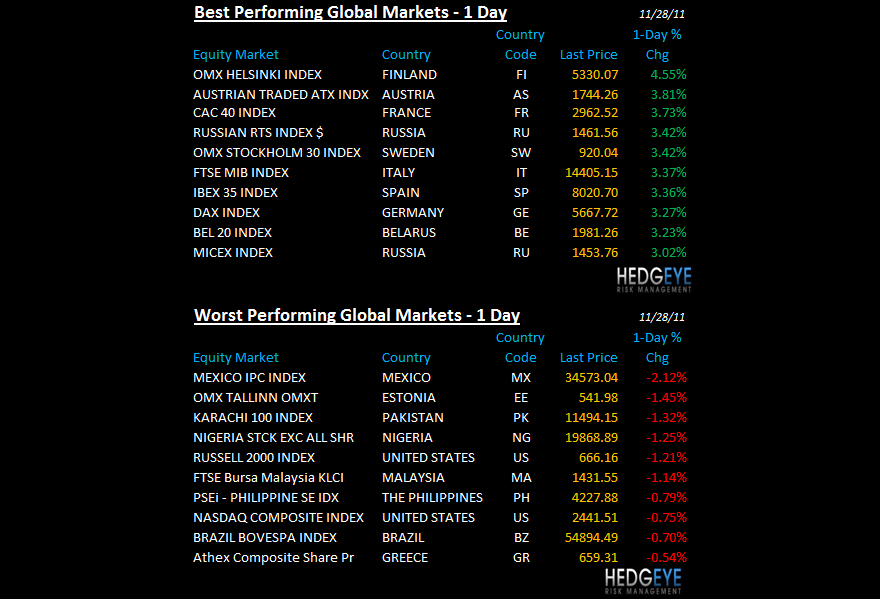

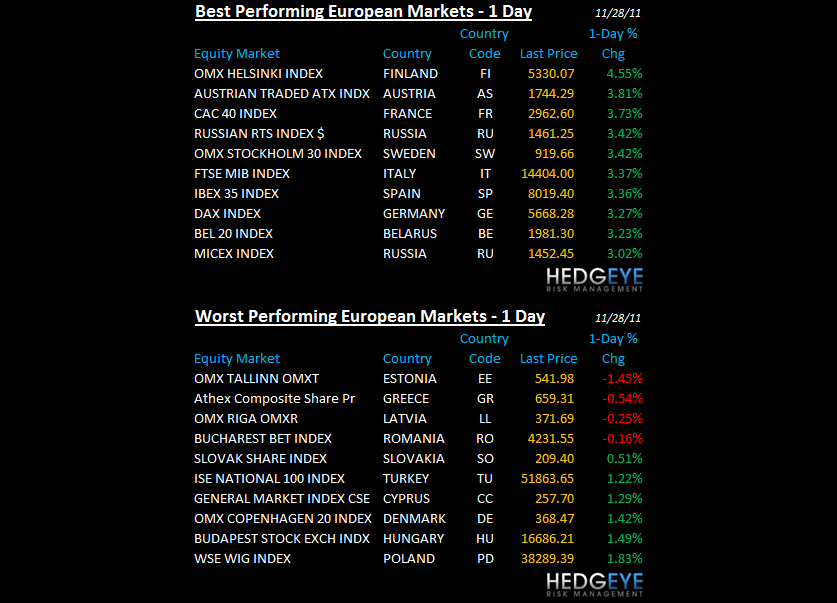

EUROPEAN MARKETS

ASIAN MARKETS

ASIA – mini-meltup in the markets that have been going down the most (HK, India, Korea – all up +2-3% overnight) as China and Indonesia didn’t care much to rally at all (closing up 0.12% and 0.27%, respectively). Asian Growth is still slowing and all Asian markets remain in Bearish Formations (bearish on all 3 of my risk management durations)

MIDDLE EAST

The Hedgeye Macro Team

Howard Penney

Managing Director