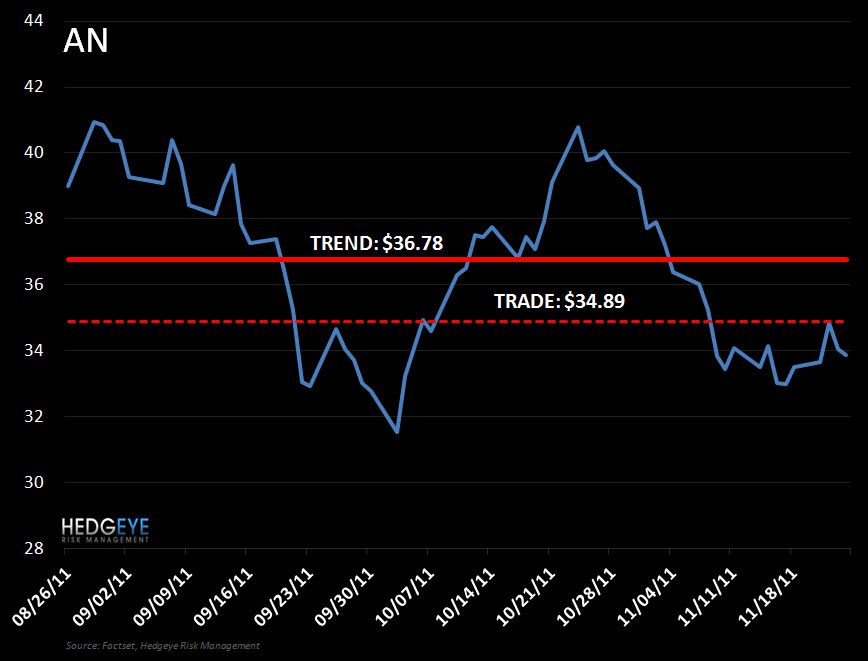

Keith covered AN in the Hedgeye virtual portfolio at $33.98 (please note correction on price) for a nice gain managing risk and trading the range this morning.

We continue to be concerned near-term with CapEx having doubled back to levels more in-line with investment prior to AN shrinking to half its size from ’05-’10 and is on pace to increase even higher as a % of sales this year. Returning to prior levels to offset deferred investment will impact FCF and the company’s ability to buy back shares and manage earnings near-term.