Conclusion: Here’s some of the most telling management quotes from 3Q, as well as our take on three important themes. With higher opex in 4Q – some which has been deferred – and 5 quarters of Inv/Sales erosion, elasticity will be a major factor in flushing out margins.

In looking back over Q3 results, several notable themes have emerged from Retail. Most notably, they related to the following…

- Driving Operating Expenses Higher. This was a common theme across all sub-categories -- especially among the poorer quality companies that need to catch up on years of deferred spending. Whether it be in the form of incremental marketing, added head count, or various IT improvements (e.g. mobile POS functionality), retailers are having to work harder and spend more to drive sales.

- Price Elasticity. Simply put, the better the product, the lower the elasticity. This has nothing to do with price. It’s all about perceived value.

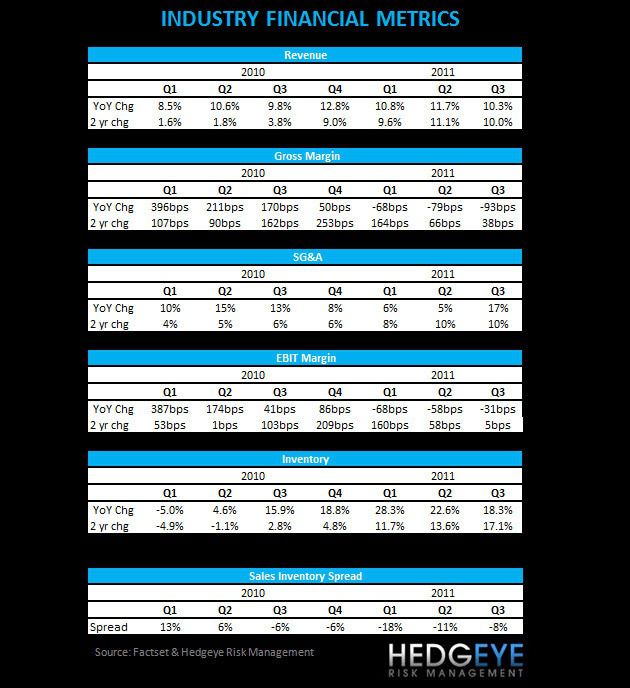

- The Inventory Growth/Gross Margin Trade-Off. Five sequential quarters of sales/inventory erosion without commensurate decline in margins is absolutely unsustainable. There’s meaningful Gross Margin risk if the consumer does not comp the 5.2% holiday performance from last year.

Here’s a quick look at some key commentary from management teams, as well as our take…

1) Elasticity:

HBI: “While units have declined, sales dollars are still quite strong. And even with the third price increase that was effective in late September, sell-through data across our major accounts indicate elasticity is at or better than our expectations…” – CEO Rich Noll

CRI: “Excluding Canada, we're forecasting inventory units at year-end to be up slightly over a year ago, with dollars up in the low 20% range reflecting largely the ongoing impact of higher product costs.” – CEO Michael Casey

GPS: “You put your plan together. Consumers respond to it, or in some cases, in Old Navy's case in October with their comp, did not respond to a level we had hoped for, so we have to make some adjustments and make sure we're aggressive in terms of our pricing, sharpen up our value proposition, and make sure we're prepared to compete in the fourth quarter… Strategically, I said in the opening comments, we have to broaden the bands of our pricing. We've been testing this, we just didn't do it all of a sudden. We've been trying that in certain categories and we've been getting good response.” – CEO Glenn Murphy

TGT: “As we expected, our guests have demonstrated a propensity to spend about the same dollar amounts through this period as they otherwise might have, essentially managing their household budgets by decreasing the number of units purchased.” – CFO Doug Scovanner

JCP: “We are on track the first couple weeks in November. We are seeing the kind of increase in AUR that we planned and we are seeing the corresponding decrease in units that we planned. So I think that we have every reason to believe at this point in time in the fourth quarter that we are on track to achieve our AUR expectations and that we will have the units necessary to take care of Christmas.” – CEO, Mike Ullman

DKS: “If we got into the gun and ammunition business, that's pretty price-sensitive business and that has not reacted particularly well to price increases. We take on the Nike side, the Under Armour side, if the brands bring to market great products, great designs, and technological advancements, the customers have pretty much stepped to the plate and said, yes, I need to have that product, whether it be increases in prices along key styles of football cleats, basketball shoes, running shoes, compression product, North Face products. Columbia has moved up their average unit retail with their Omni-Heat pretty substantially, and the customer has accepted that.” – CEO Ed Stack

GCO: “The overall theme is that ASPs were up. And for the obvious reason of the cost base driving costs to us in our branded businesses, and as we've discussed before, our expectation has always been that we get some of that back or all of that back, with retail price increases. And that's essentially the pattern we've been seeing.” – CEO Bob Dennis

PERY: “We have not been able to pass along full price increases to offset cost inflation in basic due to this fact. We have been able to get price increases in fashion goods, but in products where the consumer has not accepted the increases, retailers have had to be more promotional to move the inventory, which has resulted in higher markdowns. Our fall Perry Ellis Collection product did not perform to expectations. Some of the product that was not differentiated enough in the eyes of the consumer to warrant an increase in price, thus the value equation was wrong. We are looking at fourth-quarter increases in our organic store businesses of mid-to high single digits, driven by units down LSD, price increases in the HSD area, consistent with Q3.” – CEO George Feldenkreis

Hedgeye Retail: We think all the talk of high-end vs. low-end, is blown out of proportion. The bottom line here is that great product will not be price sensitive. Product that is ‘above average’ is on the fringe with price increases – in that perhaps a good process or marketing plan can make a difference. Product that is ‘average’ will have a problem. ‘Below average’ is a disaster.

2) Inventory/GM Trade:

GPS: “Our Q4 planned inventory unit buys are down. Similar to Q3, we expect our inventory dollars per store at the end of the fourth quarter to be up in the mid to high single digits.” – CFO Sabrina Simmons

CRI: “Overall the quality of our inventory remains excellent. Consistent with last quarter, roughly 5% of our inventory is characterized as excess, a consistent proportion of total inventory as a year ago. And we're well reserved for the expected losses on these items.” – CFO Rich Westenberger

PLCE: “When you look at the mall-based competition, we have kept our value space and kept notably below their price points 25% to 30%, but I think what we have seen there is we have seen very high inventory levels and very high degrees of promotion really all year. You can see it in the margins with the mall-based competitors and you can see it in the sales they are running. We don't anticipate, based on their inventory levels, that that is going to end anytime soon.” – CEO Jane Elfers

M: “Our stores are more set than ever for the holiday selling, and we hope that that pays off. Remember, though, that the higher in-transit will continue to be a factor at year-end, and at this point we expect to end the year with balance-sheet inventory up 6% to 7%, but comp-store inventory up less than half of that amount.” – CFO Karen Hoguet

JCP: “Our gross margin in the third quarter was impacted by the softer-than-expected selling environment, which resulted in higher promotional activity and more markdowns in the quarter.” – CFO Michael Dastugue

“The other half was in markdowns to clear the goods that -- we felt we needed to be in the right stock position coming into the fourth quarter. We are very satisfied with what we own today in terms of inventories appropriate for the fourth quarter. I would say as to the outlook for the fourth quarter, the reason we feel more confident about maintaining the margin at flat or slightly down is that, last year, we had a very difficult margin for the fourth quarter.” – CEO Mike Ullman

DKS: “Merchandise margin increased as a percentage of sales, primarily due to the continued effective inventory management, as evidenced by less clearance activity compared with last year and a shift in product mix...Meanwhile, inventory per square foot increased only 0.1%. On a consolidated same-store basis, our sales increased 4.1%.” – CEO Ed Stack

DLTR: “Consolidated inventory per selling square foot decreased by 1.2%. Inventory turns have been increasing for the past six years, and we expect this trend to continue for the full year of 2011. We have gotten better with looking at stores as far as clustering them and determining how to open them up, what inventory categories are going to be important store by store. So a lot of it is technology that we have been able to implement and continue to gain efficiencies that have continued to help us.” – CEO Bob Sasser

WSM: “Product sourcing initiatives and a strategic promotional calendar combined with tight inventories and strong expense management offset lower selling margins that resulted from a more promotional competitive environment.” – CEO Laura Alber

BKE: “Last year, we felt like we missed some business by being too low on our denim inventory, as well as certain top categories, and also in the men's outerwear, we did not have everything shipped to us last year, so we improved our inventory position there. So we felt that our inventory -- we wanted to capitalize on some of opportunities for holiday on several of those categories.” – CEO Dennis Nelson

Hedgeye Retail: Inventories have come down over each of the last two quarters, but not at the rate they need to in order to avoid a scenario where retailers are forced to get increasingly more aggressive on pricing. We’ve seen deterioration in the sales/inventory spread in apparel for five consecutive quarters without meaningful Gross Margin erosion. That is simply (and mathematically) not sustainable.

3) Accelerated SG&A/Marketing Spending:

VFC: “As we entered the year, what we indicated was, for the fourth quarter, that we thought our marketing spend could actually be down a little bit in the fourth quarter given that, given that we were up against such a -- that big increase in 2010 ($45mm in Q4 and an incremental $100mm in FY10). But at this point in time, we are spending some more. Again, we have seen such great success relative to our overall marketing spend and the investments that we have been making beyond on our brands. We are convinced that it at least plays a part in terms of the momentum that we are seeing. So at this point in time, we will spend more in the fourth quarter than we did over the high level of last year.” – CFO Bob Shearer

UA: “While we expect a generally consistent level of dollars spent as implied in our prior guidance, our higher top line guidance should allow us to leverage this line to a greater extent. We now expect marketing spending as a percentage of net revenues between 11.2% and 11.3%. This additional leverage in marketing will be offset by higher spending in selling costs related to our direct to consumer business as we continue to invest to drive current and future growth.” – CFO Brad Dickerson

GPS: “One of the big investments we've made and I'm comfortable doing it, is to make sure we continue to keep up a fairly aggressive level of marketing in 2011, 2012, and probably beyond.” – CEO Glenn Murphy

JCP: “SG&A for the quarter came in better than anticipated…this was driven primarily by our decrease in marketing spend, lower credit costs and benefits realized from our expense reduction initiatives.” – CFO Michael Dastugue

DKS: “But I think that most of our issues from the outdoor standpoint were really self-inflicted, from what we did from a marketing standpoint, and as we kind of moved into the third quarter, we thought that we would be more aggressive and we would change some of those marketing dollars back to that category of business, and we're pleased with the results.” – CEO Ed Stack

PSS: “Our marketing is increased for next year into 2012 and will be refocused obviously as it relates to our ongoing strategy. So the messaging is segmented proportionately to our strategy.” – CEO Payless ShoeSource LuAnn Via

“We are looking to reallocate some of the money that we spend, and, for instance, we are looking to spend a relative amount more on marketing, but we are looking to take other expenses out. And we are looking to invest where we can grow and invest to connect with consumers and invest in the front end and customer facing.” – CAO Doug Treff

Hedgeye Retail: We’re going to start to see a lot of deferred SG&A spend. Unfortunately for those companies, the ones that they’re catching up to are still putting coin to work. We’re going to see competitive spreads widen.

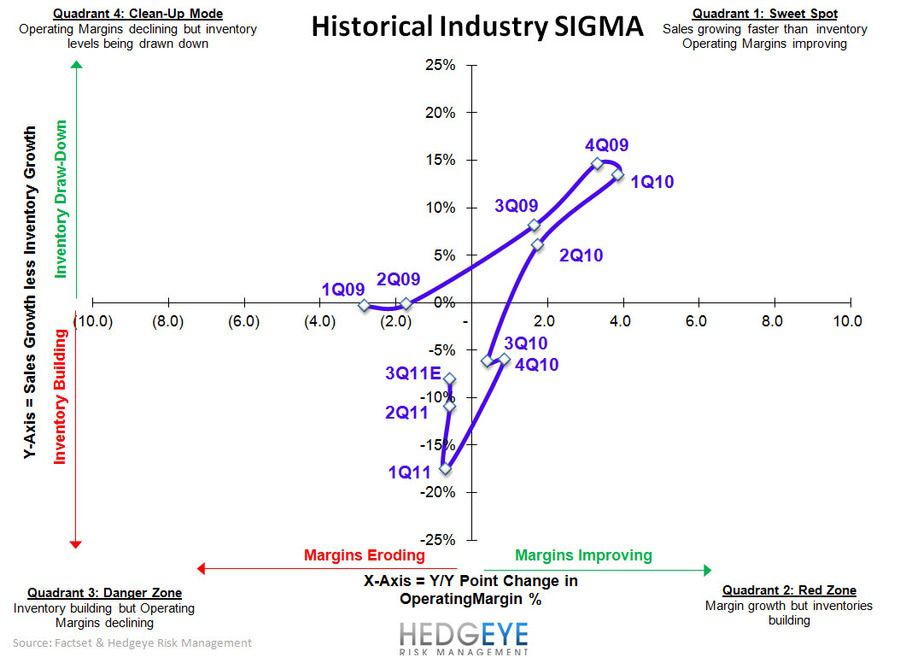

Take a look at the industry SIGMA for Q3-to-date. Operating margins have improved on the margin which is good, but the sales/inventory spread essentially remained flat – not good at all. Rather than getting more aggressive in flushing out inventories headed into what is lining up to be a highly competitive holiday season, the industry sacrificed some sales to improve profitability over the short-term at the expense of risking greater deterioration in profits over the intermediate-term. As we have seen over the last several months, sales are decelerating. One of the key factors that has propped up consumer spending to date has been a reduction in the personal saving rate. While it could go lower, we don’t expect to see it with home values continuing to decline.

Inventories have come down over each of the last two quarters, but not at the rate they need to in order to avoid a scenario where retailers are forced to get increasingly more aggressive on pricing. We expect the worst of it to play out in the domestic mid-tier market.

Shorts: JCP, HBI, CRI, SHLD

Longs: NKE, LIZ, WMT, RL