THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Unemployment

Initial jobless claims came in at 393k versus 390k consensus and a revised 391k for the week prior.

Notes below from CEO Keith McCullough

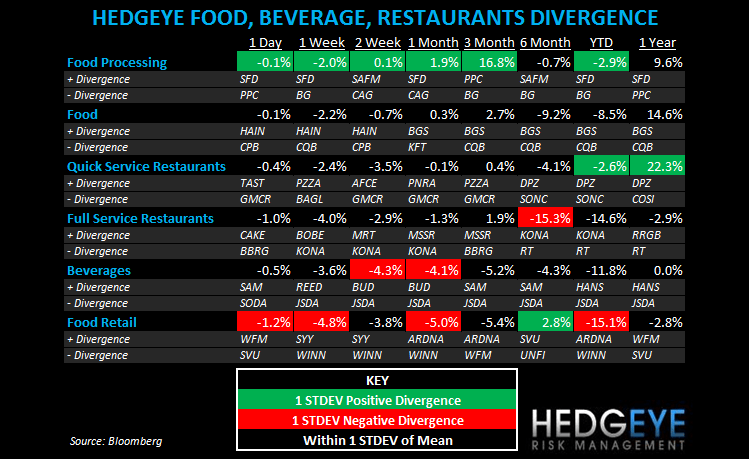

Santa needs turkey and beverage.

- ASIA – Equities are crashing again after the NOV Chinese PMI print came in at 48 vs 51 and stocks moved back into the -20% peak-to-trough zone for the YTD (HK -2.1% and down -26.7% from YTD high; India down another -2.2% and down -23.3% from YTD high); both Hong Kong (which we’re short) and Singapore reported very elevated inflation readings (+5.8% and +5.4.% y/y)

- EUROPEAN STAGFLATION - this is still my call and it’s not consensus; European consensus is for a recession – Stagflation gets a much lower equity market multiple; on the Stag side of the ledger, Germany and France reported awful Manufacturing PMI #s of 47.9 and 47.6, respectively this morn; Germany has plenty of debt to issue in NOV/DEC and their auction today was not good.

- TREASURIES – the Long-Bond and US Dollar is where this November Santa is at! 10yr plummeting to 1.90% this morning and finally immediate-term oversold as the Yield Spread continues to collapse (down another 9bps wk/wk to 164bps wide).

Deutsche Bank and Dexia are the lead dominos in a long list of European banks getting in line for bailout funds.

SUBSECTOR PERFORMANCE

QUICK SERVICE

YUM: Yum! Brands said Tuesday that it will separate its India business from Yum! Restaurants International and create a separate divison, a standalone, called Yum! Restaurants India. Niren Chaudhary has been promoted to president of the new division. CEO David Novak said that he is confident that India will turn into “a major growth engine for Yum”.

MCD: McDonald’s is testing out a new style, conceived by Paris designer Patrick Norguet, at a store in Villefranche-de-Auragais, according to the LA Times. The redesign is part of an effort to change the chain’s image in France from teen hangout to family restaurant.

DNKN: Dunkin’ Donuts is launching a twitter promotion that gives fans the chance to win a Keurig brewer and a box of Dunkin’ Donuts K-Cups. One winner per hour will be randomly selected from anyone that tweets the hashtag #DDKCUPPACKS and shares how Dunkin’ Donuts K-Cup packs keep them running throughout the holiday season. The promotion begins at 6AM Friday and ends at 11AM; there will be five winners, total.

CASUAL DINING

CBRL: During Cracker Barrel’s earnings call yesterday morning, management expressed confidence in sales trends which are, according to the company, improving in November from October. Advertising guidance for the year was unchanged. The company aims to raise price 2-3% in FY12 and notes that beef, dairy and coffee costs are up sharply.

KONA: Kona Grill says that Mark Robinow is no longer Executive Vice President, CFO, and Secretary of the company, effective as of 11/21. In the same press release, Kona Grill announced the authorization of the repurchase of up to $5 million of the company’s outstanding common stock. We are changing our stance from positive to negative. Buying back stock is the wrong decision in our view, given the cash position of the company and the need for store growth.

CAKE: Cheesecake Factory was maintained “Equalweight” at Barlcays.

Howard Penney

Managing Director

Rory Green

Analyst