Most of the commodities that we monitor for the purpose of following trends important to the restaurant and food industries took a dive over the last week.

STOCK THOUGHTS

Beef – WEN, JACK, CMG, TXRH

The supply and demand setup for beef remains bullish. Prices decreased over the last week but, given the likelihood that the U.S. herd size will be far smaller in 2012 than at the outset of 2011, elevated prices are likely to continue. Today, JACK management said that the company expects beef prices to be up 9 or 10% in 2012.

Data released by the USDA yesterday showed that cold storage supplies of beef were down 3% month-over-month in October and down slightly year-over-year. Corn is declining but winter feed stocks are depleted enough already that farmers are reducing herd sizes into year-end which will tighten supplies for 2012. There is also a seasonal uptick in the slaughter of cows in the last weeks of the year that is worth taking into account.

Concerns over Europe’s economic prospects and economic growth estimates for the U.S. being cut are weighing on beef prices but emerging market demand remains strong. Tyson Foods reported disappointing 4Q earnings yesterday and, during the earnings call, President and CEO Donald Smith said that demand was flat overall during the quarter. On a global basis, however, TSN sees demand for proteins growing but anticipates a shift in food service from beef to chicken, given the continuing high price inflation beef is bringing to restaurant companies’ P&Ls.

Chicken – BWLD

Chicken wing prices were one of the few items to increase in price over the last week. Tyson said yesterday that the company expects food service companies to focus more on chicken in 2012 which is a bullish sign for wing prices. Our view for some time has been that 1Q will prove to be very difficult for Buffalo Wild Wings as high wing prices pressure margins and the company does not have the option of preserving margins while driving sales through promotion, as it did in 3Q.

Grains – WEN, TXRH, CMG, PNRA, PZZA, DPZ

Another decline in grain prices is bullish for the restaurant industry. Feed costs for protein producers such as SAFM and TSN remain high at current prices but the trajectory is unmistakably downward. Investors are, in general, losing interest in commodities as open interest for commodities, tracked by the S&P GSCI Index, has declined 14% since February as debt and deficit concerns weigh on the EU and US. US exports of wheat fell for a second straight day today as speculation mounts that demand will decline for supplies from the US as competing exporters such as Russia boost production.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken – Whole Breast

Chicken Wings

Cheese

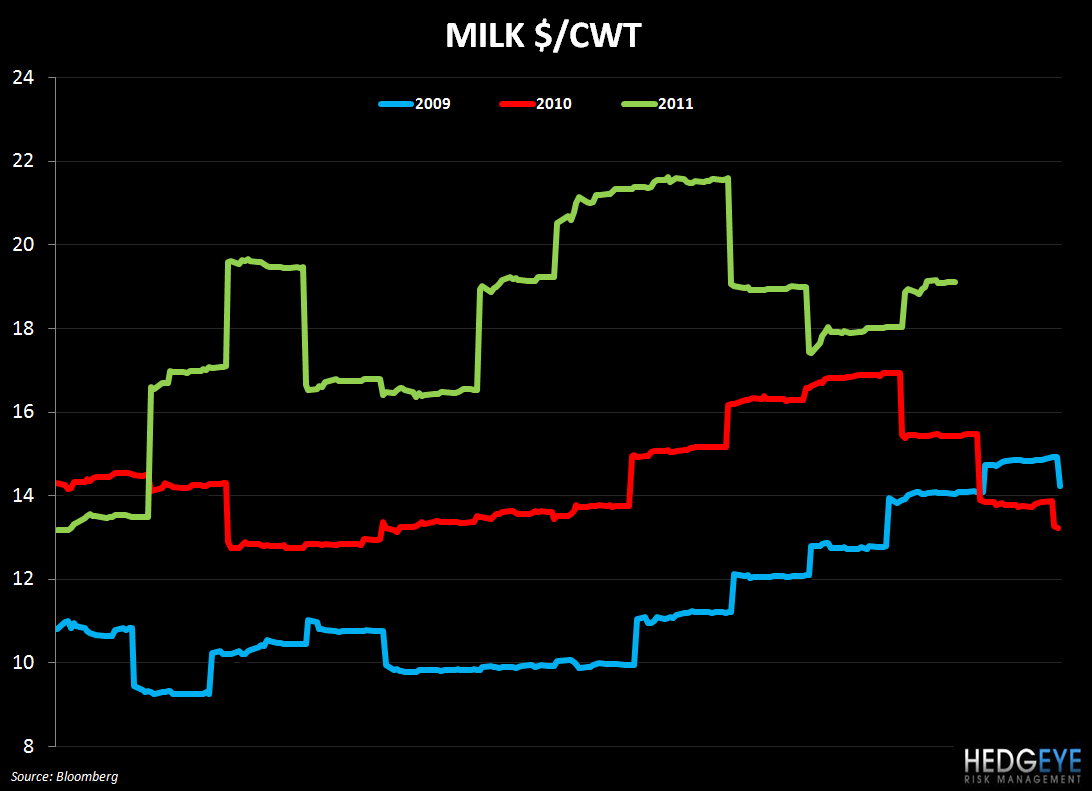

Milk

Howard Penney

Managing Director

Rory Green

Analyst