THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Notes below from CEO Keith McCullough

Intraday yesterday I made the 4th“Short Covering Opportunity” call I’ve made since August 4th:

- OVERSOLD – is as oversold does. Yesterday’s SP500 immediate-term TRADE oversold line = 1187 and this morning’s math gets me 1186, so that’s the zone. Problem with that so far is that a 10-14 point bounce can’t get us back above 1203 (TREND line resistance)

- ASIA – better than bad is the best way to describe how Asian stocks traded after the European and US selloff. Again, immediate-term TRADE ranges are what they are – they always get overbought/oversold. India finally arrested its recent decline, +0.75%.

- GOLD – I’m long and wrong Gold here and do not like it having broke its intermediate-term TREND line of $1722/oz. Gold selling off like this has a lot more to do with liquidations in the hedge fund business than anything else. Performance is not good out there.

Growth Slowing in Asia and the US combined w/ European Stagflation remains our fundamental Global Macro view on the topline.

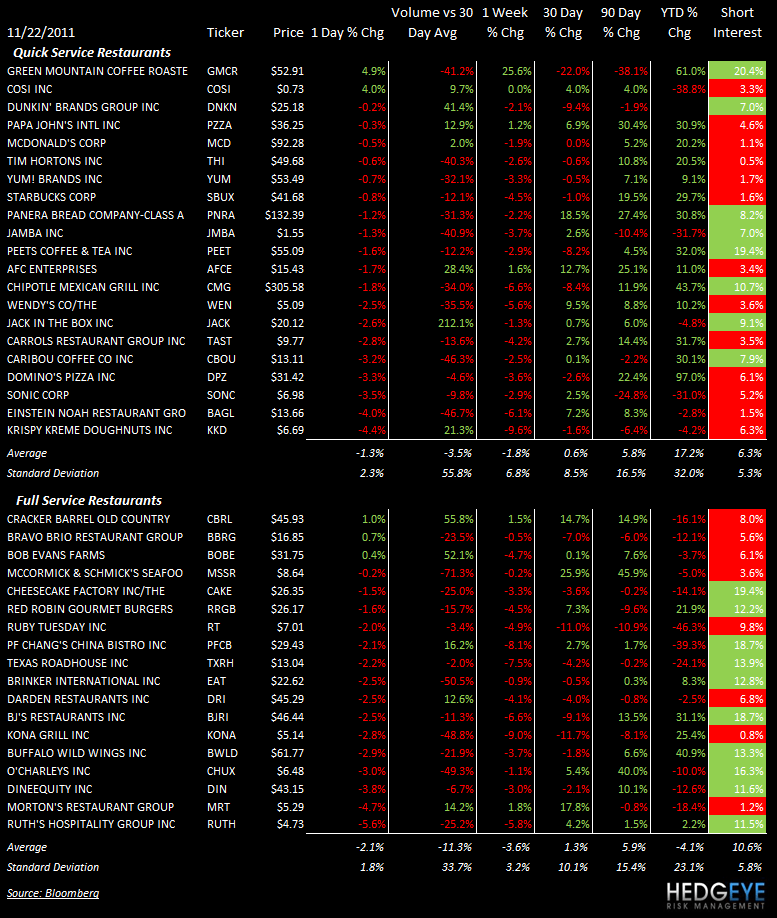

SUBSECTOR PERFORMANCE

QUICK SERVICE

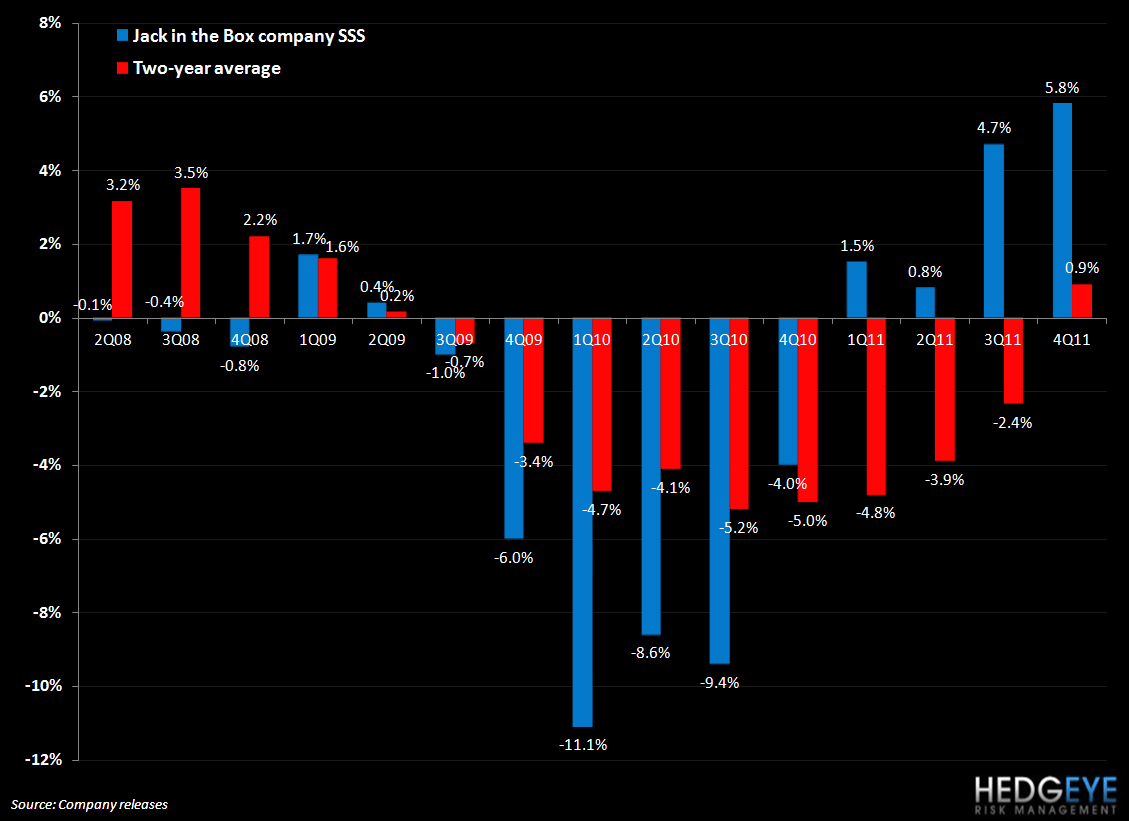

JACK: Jack In The Box reported 4Q EPS of $0.49 versus consensus $0.41. Company same-store sales at Jack in the Box restaurants gained 5.8% in the quarter versus consensus of 2.0%. Qdoba system same-store sales came in at 3.7% versus consensus 4.1%. Margins continue to improve. Guidance for 1QFY12 same store sales indicates a high level of confidence in the top line. Same-store sales are expected to increase approximately 4 to 5% at Jack in the Box (consensus +1.5%) and 2 to 3% at Qdoba system restaurants versus consensus of 2.7%. Below is a chart of Jack in the Box company same-store sales including management’s guidance for 1Q12. Commodity costs for the full year FY12 are expected to be up 5% on FY11.

YUM: Yum! Brands’ Taco Bell has cut 105 jobs across the nation and at its Irvine headquarters, according to media reports. 30 of those jobs were open and unfilled and 75 were layoffs. Taco Bell Chief Executive Greg Creed said that the structural changes being made were necessary to compete in an increasingly competitive marketplace.

CASUAL DINING

CBRL: 1QFY12 EPS was reported at $1.03 versus Bloomberg consensus $1.05. Comparable store restaurant and retail sales were down -1.6% and -1.3%, respectively. The press release said that there was a sequential improvement in both metrics during the quarter. Food costs are expected to be up 5.5% to 6.5% versus FY11.

MSSR: McCormick and Schmick’s and Landry’s have announced that Landry’s tender offer to acquire all of the issued and outstanding shares of common stock of MSSR at $8.75 per share has commenced.

Howard Penney

Managing Director

Rory Green

Analyst