THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - November 22, 2011

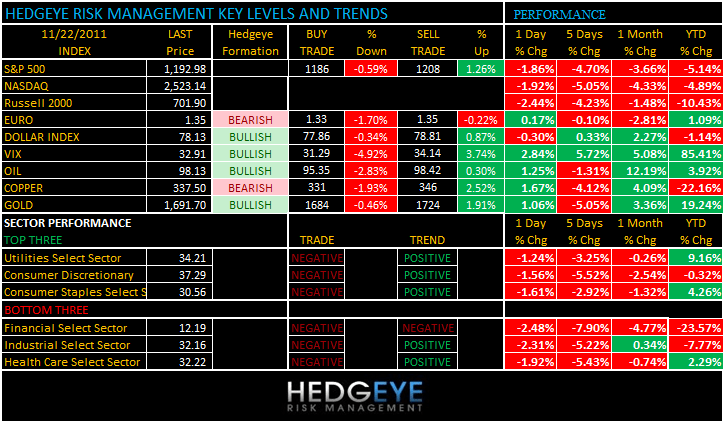

OVERSOLD is as oversold does. Yesterday’s SP500 immediate-term TRADE oversold line = 1187 and this morning’s math gets me 1186, so that’s the zone. Problem with that so far is that a 10-14 point bounce can’t get us back above 1203 (TREND line resistance). As we look at today’s set up for the S&P 500, the range is 22 points or -0.59% downside to 1186 and 1.26% upside to 1208.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2157 (-2568)

- VOLUME: NYSE 932.24 (-2.45%)

- VIX: +32.91 +2.54% YTD PERFORMANCE: +85.41%

- SPX PUT/CALL RATIO: 1.81 from 1.05 (+72.62%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 48.99

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 1.97 from 2.01

- YIELD CURVE: 1.70 from 1.72

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45/8:55am: ICSC/Redbook weekly comp retail sales

- 8:30am: GDP, Q/q, (Annualized), est. 2.5% (prior 2.5%)

- 8:30am: Personal Consumption, est. 2.4% (prior 2.4%)

- 10:00am: Richmond Fed, est. -2 (prior -6)

- 11:30am: U.S. to sell 4-wk bills

- 1:00pm: Fed’s Kocherlakota speaks in Winnipeg

- 1:00pm: U.S. to sell $35b 5-yr notes

- 2:00pm: FOMC minutes of Nov. 1-2 meeting released

WHAT TO WATCH:

- Germany sees no alternative to current policy to fight euro- zone financial crisis, Merkel ally says

- S&P, Moody’s won’t lower ratings on the U.S. after supercommittee talks fail

- Quinnipiac University holds news conference on results of national poll on 2012 GOP presidential contenders

- Obama makes speech on American Jobs Act in at high school in Manchester, N.H.

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

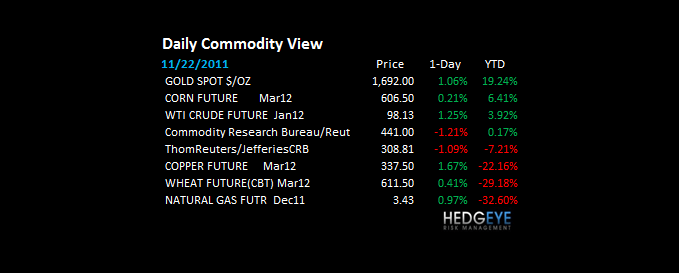

GOLD – We are long and wrong Gold here and do not like it having broke its intermediate-term TREND line of $1722/oz. Gold selling off like this has a lot more to do with liquidations in the hedge fund business than anything else. Performance is not good out there.

- Supercommittee Failure Threatens Recovery as Rating Affirmed

- World Bank Says Asia Has Room for Stimulus to Limit Europe Hit

- Oil-Tanker Rally Threatened as Ships Seen Accelerating: Freight

- DuPont Faces Squeeze as Titanium Ore Costs Advance: Commodities

- Gold Rebounds From Four-Week Low as Debt Concerns Spur Demand

- Iron Ore May Resume Fall as Demand Declines, Ord’s Arden Says

- Copper Advances as China Imports Rise, Global Inventories Drop

- Stocks Slump as Treasuries Rise on U.S. Budget; Euro Trims Loss

- Hong Kong Bourse to Introduce Commodities Trading, CEO Says

- India’s Gold Imports May Drop 15% as Rupee Plunges to Record

- Lupatech Default Bets Send Bonds to Record Low: Brazil Credit

- BHP Leads Mining Bond Sales in Surge to Record: Australia Credit

- Oil Trades Near One-Week Low on Speculation U.S. Stockpiles Rose

- Ex-Goldman Commodities Chief Plans Hedge Fund, SparkSpread Says

- Oil Gains First Day in Four as U.S. Expands Sanctions on Iran

- UBS Names Ed Carroll, Hector Freitas to Head Commodities

- Vale Proposes Tito Martins as CFO in Management Reshuffle

- Palm Oil May Gain After Breaking Resistance: Technical Analysis

- Rio Says Some Mines Are Affected by Orica Plant Shutdown

CURRENCIES

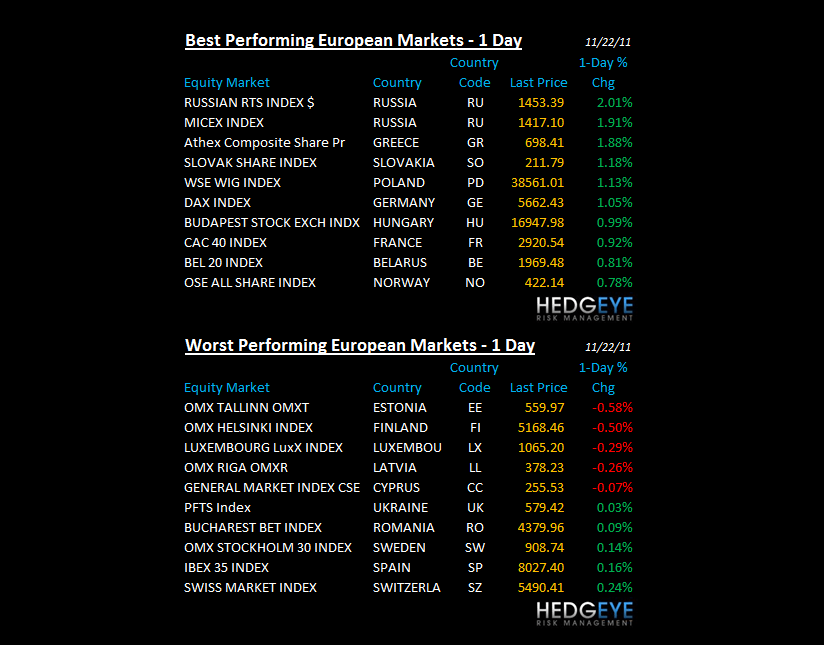

EUROPEAN MARKETS

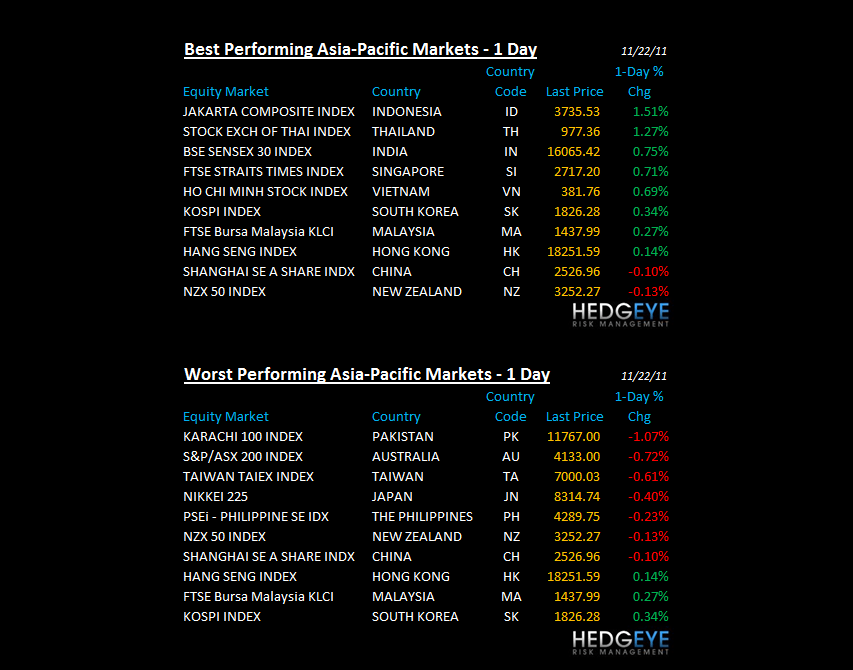

ASIAN MARKETS

ASIA – better than bad is the best way to describe how Asian stocks traded after the European and US selloff. Again, immediate-term TRADE ranges are what they are – they always get overbought/oversold. India finally arrested its recent decline, +0.75%.

MIDDLE EAST

- Oil Abundance in Canada Provokes Anxiety Over Fossil Fuel Lust

- U.S. Targets Iran Oil, Bank in Bid to Halt Nuclear Program

- Egypt Cabinet Offers to Resign as Mass Protests Planned

- OPEC May Cut Production at December Meeting, Luaibi Says

- Malaysia Leveraged Buyout Sukuk to Fund PLUS: Islamic Finance

- Oil Gains First Day in Four as U.S. Expands Sanctions on Iran

- DUBAI'S BENCHMARK STOCK INDEX CLOSES AT LOWEST SINCE JUNE 2004

- Mizuho, Mitsubishi UFJ to Finance $1.6 Billion Oman Project

- Saudi Shiites Protest in Eastern City of Qatif After Man Killed

- Dubai Shares Fall to Seven-Year Low on U.S., Europe Growth Risk

- ADCB May Offer Benchmark Bond in First-Half of 2012, CFO Says

- Abu Dhabi Taqa Offers to Buy Back Bonds, Will Meet Investors

- Doha Bank Plans to Sell Bond in First Quarter, Deputy CFO Says

- Dubai’s Stocks Fall to Lowest Level in More than Seven Years

- Dubai’s Al Wasl Brokerage May Shut as Stocks Slump to 2004 Low

- Saudi Aramco Turns to Gas, Petrochemicals as Oil Demand Wanes

- Abu Dhabi Islamic Bank Said to Sell $500 Million Five-Year Bond

- Iraq Oil Minister Expects Output Cut at Next OPEC Meeting

- N.Y. Man Faces Terror Charges After FBI Said to Decline Case

- Genel, Biggest Kurdistan Oil Producer, Falls in London Debutukuk

The Hedgeye Macro Team

Howard Penney

Managing Director