This note was originally published at 8am on November 16, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“If the masses were going to run the world, they would need a lot of instruction.”

-Sylvia Nasar

That’s a quote from Nasar’s recently published book “Grand Pursuit” where she explains how one of Yale’s “great men”, J. Willard Gibbs (chemist, mathematician, physicist), thought about a globally interconnected world at the turn of the 20th century (page 147).

The late 1800s and early 1900s were a very formative time for the study of economics. That’s when mathematicians got involved. Quantifying the qualitative is important. The fear-mongering styles of Malthus, Carlyle, and Marx were replaced by new lines of thinking from the likes of Marshall, Schumpeter, and Fisher. Re-thinking was good.

Since then, we’ve had a long, hard, muddle through nerdy economic debates about Hayek vs Keynes, Rand vs Bureaucrats, and Capitalism vs Socialism. But we really haven’t evolved the process by which we apply modern day math (Chaos and Complexity Theory) to how we’re thinking about economies and markets.

Since Chaos Theory is the most relevant mathematical conclusion since relativity, I think there is plenty of re-working and re-thinking to be done. Instructing The Masses on how markets work will take time. It’s time that I am personally willing to make.

Back to the Global Macro Grind…

One of the gaping voids that’s obvious to anyone who has studied a Yale or Princeton economics textbook is the behavioral side of markets that plays such a critical role in the decision making of market participants. Kahneman, Tversky, and Taleb have all contributed significantly to qualifying the impact psychology has on markets, but we are still in the very early days of applying these learnings.

Quantifying sentiment is very difficult. I’ve been on the road seeing clients from Denver to Kansas City to San Diego, Boston, and New York in the last 6 weeks – and the #1 question I get is “what are you hearing.”

What I am “hearing” and what my risk management models are seeing are quite often very different things. But since our industry has effectively become one gargantuan front-running exercise of trying to beat the market’s beta, it’s a question that modern practitioners of asset management have to constantly evaluate.

What’s sentiment right now?

Well, from a Global Macro perspective, there’s not one answer that fits nicely in a baby blue box with a Tiffany bow on it. Sorry. Asian stock markets continued to fall, hard, last night. China was down another -2.5%, and India remains under inflation’s pressure (Sensex down another -0.6%). The Euro, European Bonds, and European Equities remain a mess.

From a US stock market “sentiment” perspective, one of the best contrarian readings I can give you is measured by looking at the spread between Bulls and Bears in the II Survey (comes out every Wednesday):

- In late September, the spread was bearish (meaning more Bears than Bulls) on the order of -1900 basis points (19%)

- After October’s rally (the biggest ever in US stock market history), the Bullish to Bearish spread flattened to even

- This morning, the spread has widened to +1500 basis points (Bulls 47.4% minus Bears 32.6% = +15%)

And while that’s only 1 factor I’m observing in my multi-factor, multi-duration, risk management model – my spidey senses say that sounds just about right. Hedge Funds fear being short. Mutual Funds fear missing Santa Claus. Central planners fear-monger.

Back to where I started this morning’s note, I think we’re a lot smarter than staring at the futures on TV this morning looking for an emotional direction. Mediocre minds are not going to lead us anywhere but lower. We need to be the change we all want to see in our analytics.

While Big Government Interventionists and the ad dollars that support them think that all of this is going to end according to their central plan, globally interconnected markets have a not so funny way of getting in the way of that…

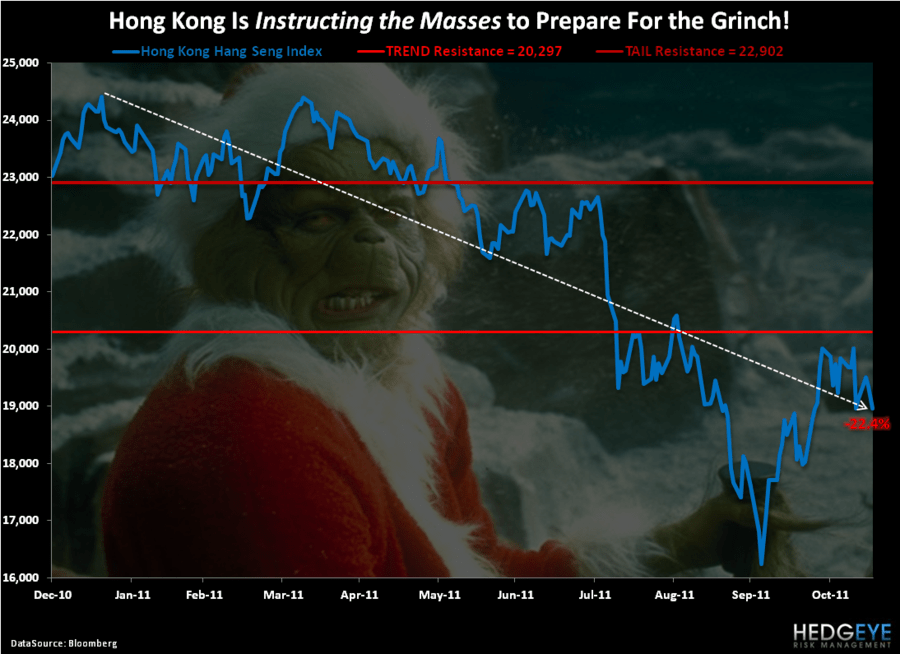

My Top 3 globally interconnected points confirming Asian, European, and North American stock market weakness this morning are:

- Chinese Demand: Hong Kong trading down -2% well below TREND line support of 20,297 on the Hang Seng

- Dr Copper: down another -1% to $3.48/lb, remaining in what we call a Bearish Formation (bearish TRADE, TREND, and TAIL)

- US Treasury Yields: continue to signal that both US and Global Growth are slowing (TRADE resistance for 10-yr yields = 2.15%)

Of course the Euro collapsing versus the US Dollar remains the #1 Correlation Risk factor affecting Global Macro markets. But you already know that – because our Instructing The Masses since founding the firm in 2008 has been consistently backed by the math.

My immediate-term support and resistance ranges for Gold, Oil, France CAC, German DAX, and the SP500 are now $1747-1810, $96.92-100.33, 3037-3176, 5820-6089, and 1237-1269, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer