TODAY’S S&P 500 SET-UP - November 21, 2011

The bull markets we see are in the US Dollar (UUP), Long-term Treasuries (TLT), and Growth Slowing (FLAT). As we look at today’s set up for the S&P 500, the range is 40 points or -1.29% downside to 1200 and 2.00% upside to 1240.

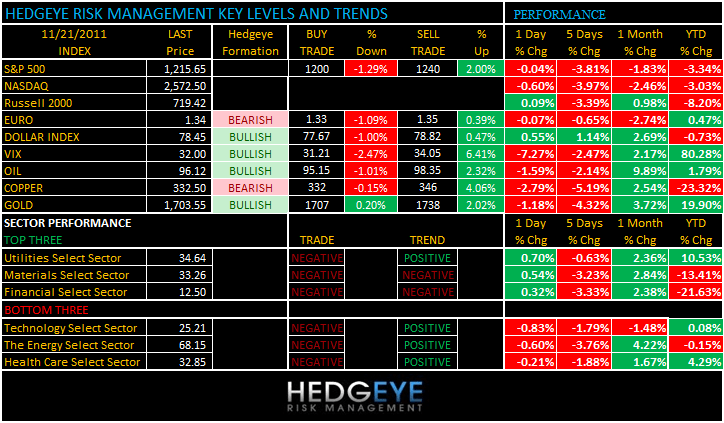

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +411 (+2289)

- VOLUME: NYSE 955.68 (-6.73%)

- VIX: +32.00 -7.27% YTD PERFORMANCE: +80.28%

- SPX PUT/CALL RATIO: 1.05 from 2.14 (-50.93%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 48.78

- 3-MONTH T-BILL YIELD: 0.00%

- 10-Year: 2.01 from 1.96

- YIELD CURVE: 1.72 from 1.69

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed, est. 0.19, (prior -0.22)

- 0am: Existing home sales, est. 4.8m, prior 4.91m

- 11:30am: U.S. to sell $29b 3-mo., $27b 6-mo. bills

- 1pm: U.S. to sell $35b 2-yr notes

- 2:30pm: Fed’s Lockhart to speak on economy in Brazil

- 8 pm: Fed’s Bullard gives welcoming remarks in St. Louis

WHAT TO WATCH:

- Bipartisan supercommittee said to be on brink of failure, setting stage for $1.2t in automatic spending cuts

- Deutsche Bank CEO Josef Ackermann said yesterday Europe needs a “firewall” to prevent its debt crisis from spreading and should increase the size of its rescue fund

- Deadline today for the Congressional Budget Office to receive information for scoring a proposal in advance of supercommittee target date of Nov. 23; Democratic aide says supercommittee likely will announce today that it can’t reach agreement on deficit savings

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Hedge Funds Cut Bullish Bets by Most in Seven Weeks: Commodities

- Gold May Drop as Spanish Opposition Victory Curbs Haven Demand

- Oil Falls to Lowest in a Week on Asian Demand, European Crisis

- New Cameco Bid Topping Rio Seen in Record Hathor Value: Real M&A

- Oil Bets Jump to Six-Month High Before Seaway: Energy Markets

- Dana Gas Yields Jump Most in Month on Debt Risk: Islamic Finance

- Copper Set for ‘Strong Rally’ in 2Q on Deficit, Goldman Says

- Mechel ‘Lucky’ Paying Less Than Norilsk on Loans: Russia Credit

- Graff Diamonds to Use Planned IPO Proceeds on Asia Stores

- Gold Falls to 3-Week Low as Stronger Dollar Cuts Investor Demand

- Tin Exports From Indonesia May Drop 26% This Month on Curbs

- Copper Imports by China Gain for a Fifth Month on Arbitrage

- Rubber Blacklist Proposal May Cut Defaults, Thai Group Says

- Copper Falls for Third Day as Growth Concerns Threaten Demand

- Temasek, ADM, Mitsui to Invest in New Hope Agriculture Fund

- Newfoundland’s Oil Royalties Fund Debt Reduction: Canada Credit

- ABB, Siemens to Benefit From Commodity Mkt Strength: Citigroup

- OPEC’s Meeting in December Will Be ‘Comfortable,’ Badri Says

- UniCredit Names Fischer Co-Head of Project & Commodity Finance

CURRENCIES

EUROPEAN MARKETS

SPAIN - center right government = austerity = European Stagflation; if Singapore thinks they only to +1-3% GDP growth in 2012, the Europeans could be down -2-4% GDP in no time. European stocks getting rocked and now all major European tapes back in Bearish Formations (bearish across all 3 of my risk management durations); Greece -60% since FEB

ASIAN MARKETS

SINGAPORE – these guys are now being as explicit as we have seen them since 2008 about Global Growth Slowing (the Monetary Authority of Singapore: “The world economy and financial system are at their most fragile state since the 2008-2009 global financial crisis”); both HK and India continued to crash overnight (down -25.3% and -22.2% respectively from YTD tops)

MIDDLE EAST

- New York Man Charged With Plotting Pipe-Bomb Attacks in City

- Fatal Egypt Clashes Fuel Investor Concern Before First Vote

- Dana Gas Yields Jump Most in Month on Debt Risk: Islamic Finance

- Assad Defiance in Syria Spurs U.S., Allies to Mull New Steps

- Egyptian Protesters, Forces Clash for Third Day Before Election

- Saudi Aramco CEO Sees Risk of World Double-Dip Recession

- OPEC’s Meeting in December Will Be ‘Comfortable,’ Badri Says

- Iranian Airline Buys Mothballed Merkel VIP Jet, Spiegel Says

- Kuwait Opposition Groups Plan Protest Tonight to Oust Premier

- Saudi Arabia’s Oil Minister Says ‘Very Happy’ With Crude Prices

- Majid Al Futtaim Seeks to Raise About $500 Million From Sukuk

- Fawaz Al Hokair May Tap Debt Markets in 2012, CFO Says

- Dubai’s Shares Retreat to Month Low on U.S. Impasse, Europe Risk

- Iran Says Oil Market Will Suffer If Its Exports Disrupted

- Al Futtaim Group Says in Final Stage to Raise $1 Billion Loan

- Yara, Hydro Raise Salaries for Qataris Amid New Rules: DN Link

- Shuaa Sinks to Eight-Year Low on Firing Plan, Quarterly Loss

- Majid Al Futtaim Seeks to Raise About $500 Million From Sukuk

The Hedgeye Macro Team

Howard Penney

Managing Director