We’re more concerned with the potential for a junket commission war between the operators.

We believe LVS may have struck a sweetheart deal with Neptune which may be more attractive (to Neptune) than the best junket deals with Galaxy, MPEL, or MGM. Whether other junkets demand the same deal from other concessionaires (there are no secrets) remains to be seen. It seems likely, however, that market wide commissions and commission advancement are likely to escalate. How much will that constrict margins? Will Wynn follow suit? Could the junkets negotiate as more of a consortium? We will try and answer these questions in a later note. This note deals with another area of concern: receivables.

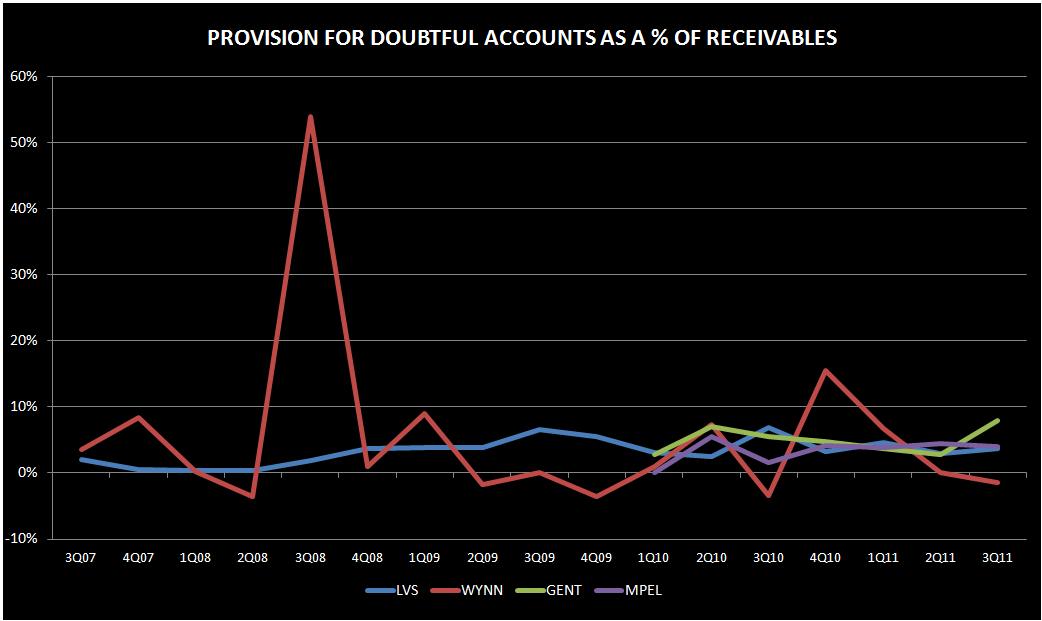

After Genting Singapore reported a large spike in their provision for bad debts last week (as seen in the chart below), credit issues once again became the topic de jour amongst the gaming community. Existing fears of a VIP slowdown have made investors already on edge. We’re not dismissing either issue but the numbers don’t provide a lot of basis for concern. In addition, we think it’s interesting that the investment community only seems concerned with these charges when they occur at an Asian-based operator. Wynn has several quarters with large spikes in their provision for doubtful accounts but no one seems to lose a wink of sleep over these. Namely in 4Q 2010, Wynn Macau took a $10MM charge which they simply explained “was a function of business volumes… in particular in our direct program in the fourth quarter.” In 3Q08, Wynn Macau took a provision of $19MM as well.

As the chart below shows, MPEL’s receivables as a % of direct play, while decreasing, are higher than the comp set. We believe that this is a direct reflection of the lending that goes on in their premium mass segment.

The 3rd chart shows that while Genting’s receivables as a % of direct play have been increasing, they do not look out of whack with what MBS reports, although we would be concerned if the upward trend continues.