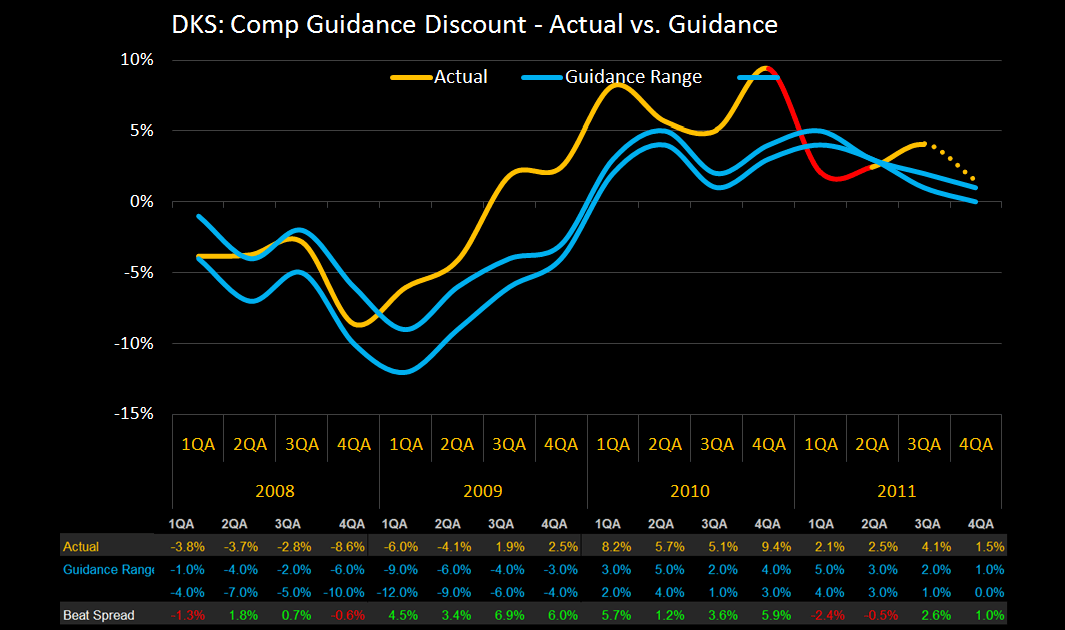

Solid results out of DKS this morning ($0.32 vs. $0.27E) reflect accelerating sales strength we’re seeing in the athletic specialty channel – good for NKE & UA and FL & FINL. Following two quarters in a row where the company came in below its comp guidance it trumped both guidance (+1%-2%) and expectations (+2%) in Q3.

Here a few callouts from Q3:

- In addition to a reacceleration in sales on both a 1yr and 2yr, the company’s comp (+4.1%) came in above guidance is notable given its missed expectations in each of the last two quarters.

- The composition of DKS’ comp was also impressive with Golf Galaxy up +2.4% despite others citing weakness in the category and e-commerce up +17% on a +82% comp reflecting solid acceleration in underlying 2yr trend

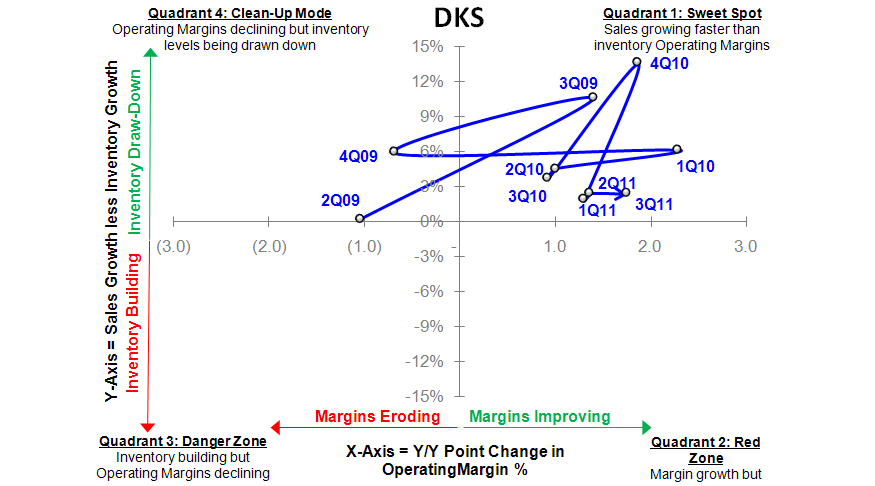

- The company has posted a positive sales/inventory spread and operating margin growth for seven consecutive quarters – one of the more stable recent records of note in retail

- Inventories up +7%, up only 0.1% per sq ft. with 19 stores opened in the qtr reflecting a healthy athletic channel – good for NKE and UA.

- Gross margins were up +126bps reflecting continued mix improvement and strength in the channel i.e. lack of promotional activity.

- SG&A up +7.1% was leveraged on higher sales – we expect continued leverage in Q4

- Company raising Q4 outlook by a penny on comp guidance that looks acheivable.

Call at 10am at

Casey Flavin

Director