TODAY’S S&P 500 SET-UP - November 15, 2011

How people get longer w/ Italy and France trading like this defies logic. As we look at today’s set up for the S&P 500, the range is 36 points or -1.50% downside to 1233 and 1.38% upside to 1269.

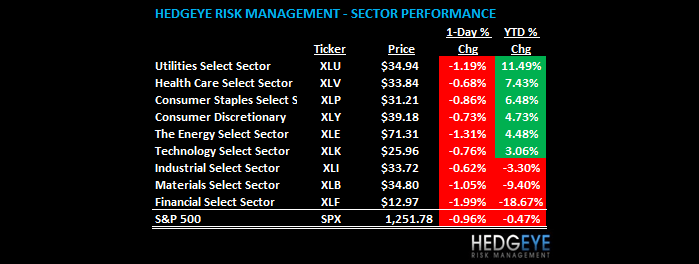

SECTOR AND GLOBAL PERFORMANCE

The SP500’s TAIL remains bearish (1269 resistance). With stocks down for both November and 2011 YTD again, this should not surprise anyone. Since 2007, despite the fanfare, the SP500 has been making a series of lower long-term highs as volatility makes a series of higher long-term lows.

That’s the message for long-term investors. In the shorter-term, the best October ever continues to provide a hope that another bottom is in. Our S&P Sector Studies confirm that view (for now), with 7 of 9 Sectors remaining bullish from an intermediate-term TREND perspective.

The 2 of 9 that remain in Bearish Formations (bearish TRADE, TREND, and TAIL) are the two that auger most poorly in our King Dollar Global Macro Theme - Financials (XLF – down -18.8% YTD) and Basic Materials (XLB – down -9.4% YTD).

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1585 (-3762)

- VOLUME: NYSE 709.97 (-6.86%)

- VIX: +31.13 +3.36% YTD PERFORMANCE: +75.38%

- SPX PUT/CALL RATIO: 1.20 from 1.48 (-19.23%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 45.55

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.04 from 2.04

- YIELD CURVE: 1.80 from 1.80

MACRO DATA POINTS (Bloomberg Estimates):

- US ICSC-Goldman Chain Store (12-Nov);

- US Empire Manufacturing (Nov); consensus (1.8)

- US PPI (Oct); consensus (0.1%)

- US PPI ex Food & Energy (Oct); consensus +0.1%

- US Retail Sales (Oct); consensus +0.4%

- US Retail Sales ex Autos (Oct); consensus +0.2%

- US Redbook Chain Store (12-Nov);

- US Business Inventories (Sep); consensus +0.2%

- US API Crude Inventories (11-Nov);

WHAT TO WATCH:

- Fed's Evans speaks on dual mandate

- Fed's Bullard speaks on economic outlook and monetary policy

- Money may have started disappearing from MF Global customer accounts four days before company filed for bankruptcy - WSJ,

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Sino-Forest Says Probe Refutes Muddy Waters Allegations

- Speculators Boost Bullish Bets to Seven-Week High: Commodities

- Hedge Funds Raise Oil Bets to Highest Since May: Energy Markets

- Gold Declines for Second Day as Paulson Cuts Bet, Euro Weakens

- Aussie Resisting Iron Ore Drop to Spur RBA Cut: Chart of the Day

- China Shuts 90% of Lead-Acid Battery Plants as Prices Drop

- Oil Falls as Europe Debt Concern Counters Shrinking U.S. Supply

- Paulson Cuts Holding in SPDR Gold Trust; Soros Fund Has Increase

- Sumitomo Metal’s Nickel Project in Philippines May See Delay

- Rusal Says Up to 15% of Global Aluminum Capacity May Be Shut

- Copper Falls for First Day in Three Amid Europe Debt Concerns

- MF Global Overseer Has ‘Multiple’ Possible Buyers in LME Shares

- Crude Trades Near Two-Day Low in New York; Brent Futures Gain

- Nippon Metal, Nisshin Steel Seek to Merge Within a Year

- Cameco Raises Hathor Bid to C$625 Million to Trump Rio Offer

- Copper Falls in London as Traders Get More Negative: LME Preview

- Andrew Hall’s Astenbeck Buys Uranium, Rare Earth Companies

- Gold Declines as Dollar’s Gains Curb Demand; Paulson Cuts Bet

CURRENCIES

EURO – The only line of support of consequence that remained in our model was 1.37 and now that’s gone. Plenty of weak hands were forced to cover in the last 6 weeks. It’s a better short today than it was yesterday.

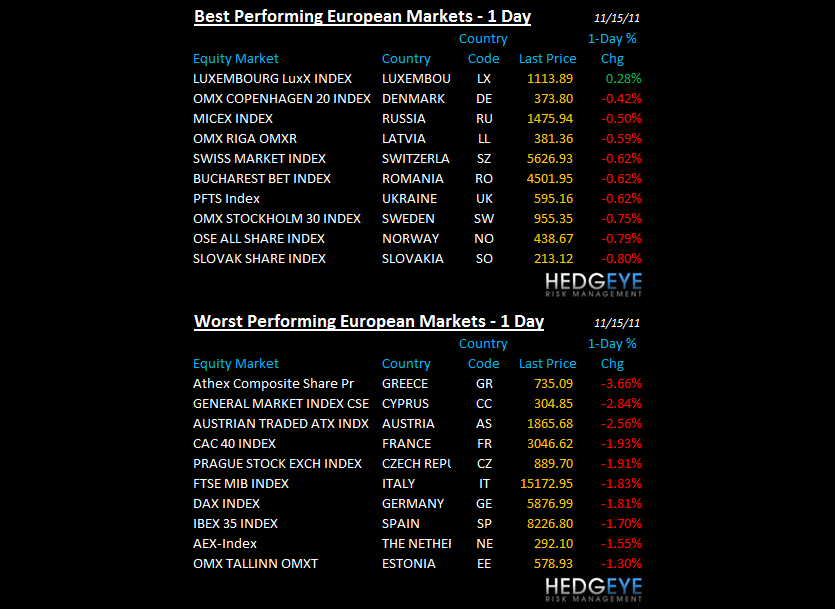

EUROPEAN MARKETS

FRANCE – I’ll write and say this every day until its headline news – France is a bigger problem (from here) than Italy. French banks have not marked their pig paper yet and that paper (Spain’s 12-month fiat priced at 5.02% this morning vs 3.61% last) is a Lehman-like problem. We remain short French Equities, which remain in a Bearish Formation (bearish TRADE, TREND, and TAIL).

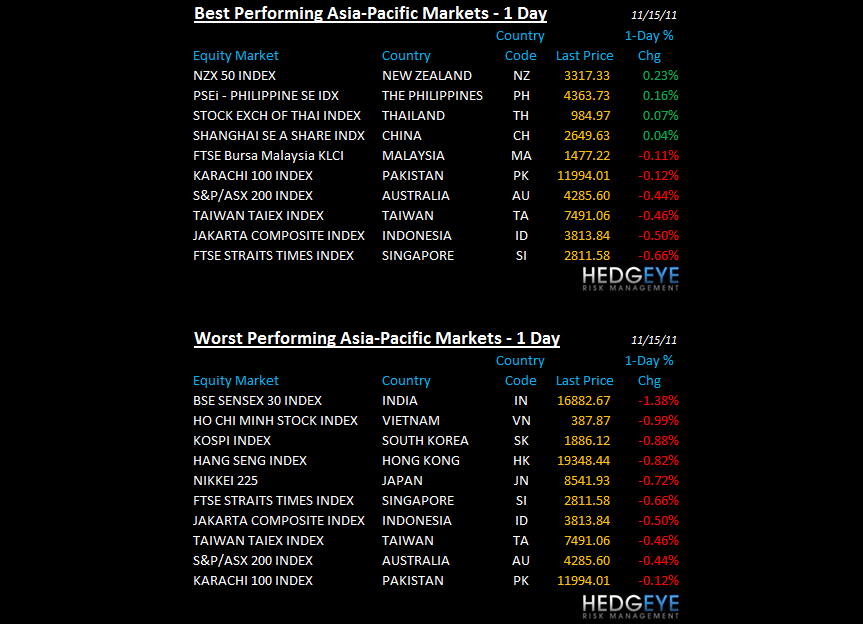

ASIAN MARKETS

INDIA – one of the big places in this world (with a lot of people) that does not cease to exist amidst the European headlines has once again snapped its last line of support (17,169 on the Sensex), leading Asian stocks lower overnight after an awful inflation report (+9.73% OCT).

MIDDLE EAST

POPULAR MIDDLE EAST HEADLINES FROM BLOOMBERG

- Qatar Air CEO Ridicules Airbus After Shelving Aircraft Order

- Obama Microphone Slip Shows Scary Israel Rift: Jeffrey Goldberg

- Bahraini Body Endorses Malaysian Derivatives: Islamic Finance

- Syria Under Pressure After Suspension by Arab League

- Taqa Third-Quarter Net More Than Doubles on Higher Oil, Gas

- Union Properties Reports Record Quarterly Loss as Costs Jump

- Commercial Bank of Qatar Removed From Goldman CEEMEA Focus List

- Saudi Arabia Said to Boost Indian Oil Exports in 2012 Contracts

- Oil Above $200 Possible in Event of Iran Conflict, SEB Says

- Kuwait Finance Says Management Unaware of Rajhi Stake Buy Plan

- Premier Oil Sells U.K.’s Cladhan to Taqa, Buys Fields From Nexen

- Gas Exporters Seek Cooperation to Raise Supply, Boost Prices

- Qatar Shares Decline on Bets Gains Overdone, Europe Debt Concern

- Israel Behind Deadly Iranian Blast, Source Says: Time Link

- Airbus Postpones Qatar Accord as Al Baker Leaves Deal Dangling

- Boeing Wins Order From Qatar Airways for Two 777 Freighters

- Abu Dhabi Commercial Bank Said to Plan U.S. Dollar Sukuk Sale

- Iranian Parliament to Investigate Blast at Military Base

The Hedgeye Macro Team

Howard Penney

Managing Director