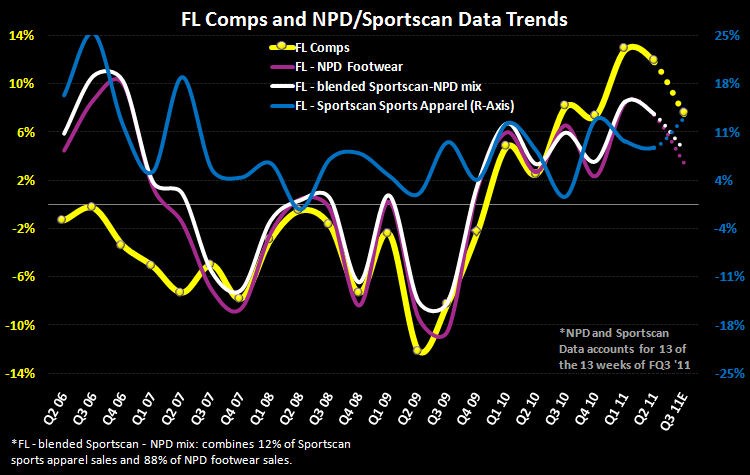

We expect a solid Q3 out of FL Thursday. Despite the overhang of NBA related headline risk, the already-anemic basketball category actually improved on the margin, and overall industry sales appear to have accelerated throughout the quarter. The latest NPD data which is a component of our (statistically-valid) comp predictive model, supports our above consensus view.

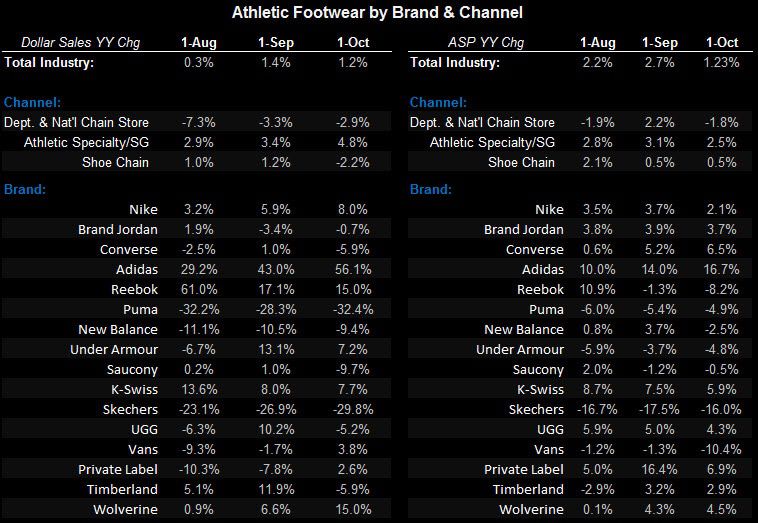

We’re at $0.46 for FL on a comp assumption of +7.5% for the quarter headed into Thursday’s print, which is ahead of the Street at $0.39 and +5.3% respectively. We’re increasing our comp assumption to +7.5% from +6% based on stronger sales coming through in October. Through the first two months of the quarter, the Athletic Specialty channel was tracking up +3.1% -- well ahead of the total industry -- which had been tracking up +0.8%. With the Athletic Specialty channel tracking ~200-400bps ahead of aggregate weekly numbers we took up our estimates as October came in closer to up +2% as reflecting in the weekly data.

It’s important to note that weekly footwear numbers reflect the broader industry sample and therefore understate the underlying sales performance in the athletic specialty channel that most accurately reflects sales at athletic retailers such as FINL, DKS, HIBB, and FL in particular given its contribution to the sample set. October data out today confirms continued outperformance in the athletic specialty channel, which came in up +4.8% compared to the broader industry up +1.2% right in-line with our expectations.

In light of sales coming in stronger at quarter end, we have increased our GM estimates to 160bps over last year driven by +100bps in occupancy leverage and 60bps from merchandise margin, which may prove conservative as well a 5% increase in SG&A to support more active marketing efforts. This equates to EPS of $0.46 for the quarter up from our previous $0.42 estimate and $1.83 for the year vs. consensus at $0.39 and $1.72.

While we have been incrementally less bullish on the stock up here north of $22 given the near-term headline risk associated with the pending NBA strike, we expect the stock to maintain its underlying momentum when it reports results Thursday. With the stock currently trading at 12.5x and 11x our F11 and F12 EPS estimates respectively and below its historical average of 13x-15x, we would be looking to get more constructive on any weakness.

Casey Flavin

Director