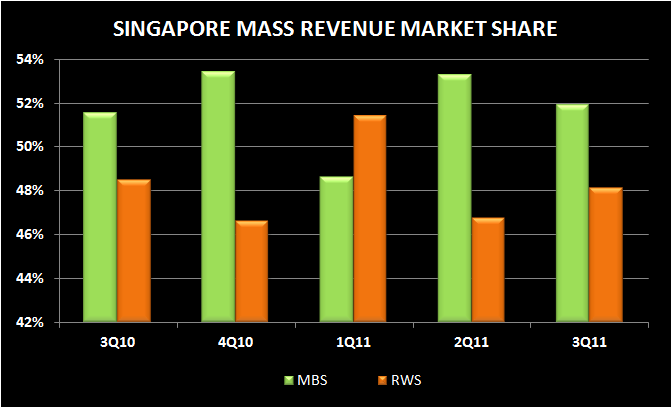

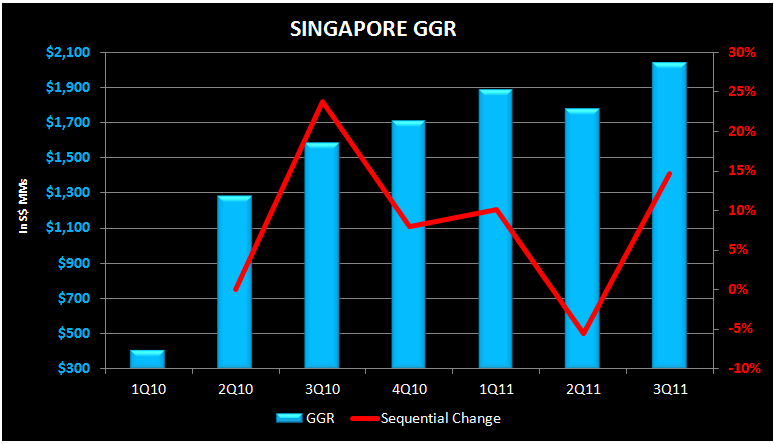

Singapore casino gaming market rebounded in Q3, as gross gaming revenues rose 29% YoY and 15% sequentially. For comparison, Macau GGR grew 7% QoQ and 48% YoY. S’pore gaming EBITDA grew 3% QoQ to S$882MM, 2% lower than Q1’s high of S$902MM. Mass revenues grew 10% to S$640MM and VIP Rolling Chip Volume expanded 16% to S$36.8BN, a new record.

3Q hold was 2.9%, slightly higher than Q2’s 2.82%. Average hold in for the 2 IR’s since 1Q10 has been close to 3%. Sequential revenue growth has been falling since 3Q 2010.

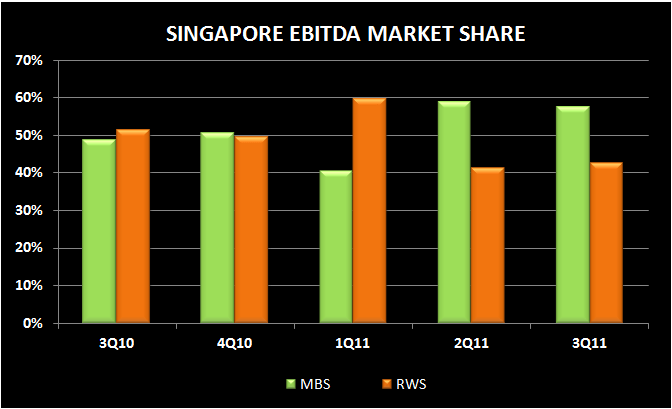

It took MBS only 6 quarters to lead in every market share category in Q3. The biggest shift was in VIP RC Volume share where MBS surged from 48% in Q2 to 56% in Q3. Despite having a hold % that was 0.5% points lower, MBS extended its VIP win market share to 51.6%. While Genting’s bleeding may continue, its slot ramp towards the end of the year may help build mass share in Q4.

Singapore’s Q3 strength is a relief for the bulls as weak Q2 results had dampened optimism. However, as GENT pointed out in their Q3 conference call, caution is warranted at least for the rest of the year. We still see a cap on long-term growth in Singapore unless junkets are approved in the near future.