What’s not to like? But they’re raising the bar, and probably won’t get paid for it.

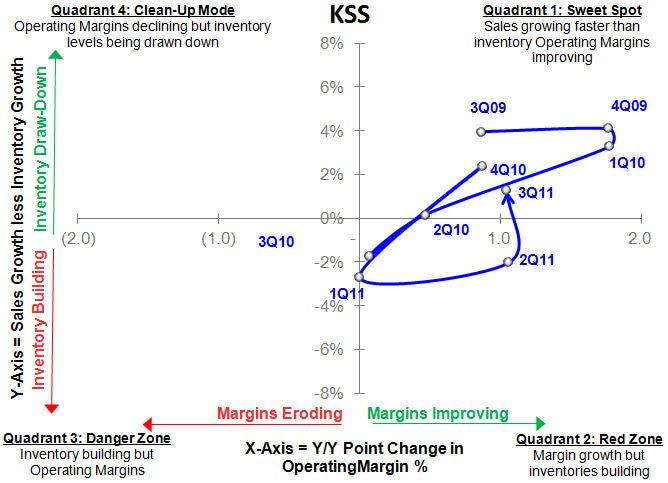

We have a very mixed read on this KSS quarter. On one hand, it was the mother of all in-line performances – something we’ve grown to know and love (and expect) out of this company. Sales were already a known entity and margins came in virtually in-line. The inventory spread improved year/year and sequentially, making KSS one of the few retailers to post this trend. In effect, it was the opposite of what we saw from Macy’s. That’s notable given that KSS represents roughly 8% of the softlines industry in aggregate – the more sane the industry is on inventories – especially in the mid-tier -- the better. KSS showed yet again, why it sets so many benchmarks for the rest of the industry.

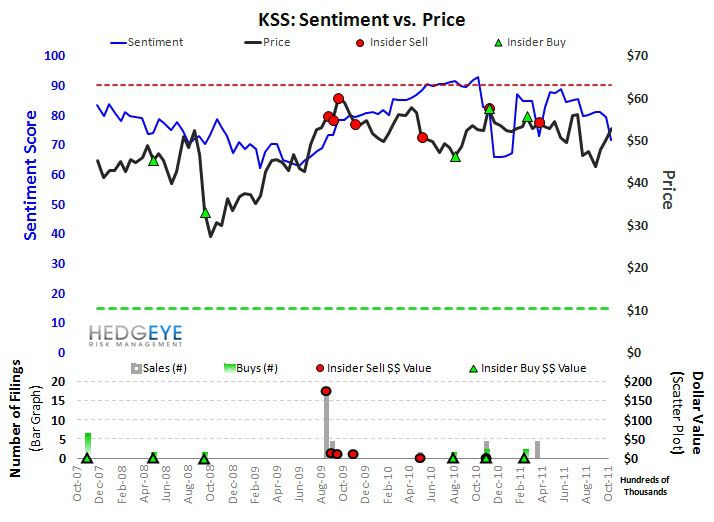

But we’re a bit perplexed on guidance. This is a complete and total nit-pick, but why take up 4Q at a time when yy compares are getting tough? With so much uncertainty coming down the pike, why not keep the year even instead of stepping up the Street’s expectations by 5% when we’re already looking at 18 Buys, 6 Holds, and only 1 Sell? Buy-side sentiment is slightly less positive, with 6% of the float short – on the higher side for KSS. But blended together in our Sentiment Indicator, people are still bulled-up on this name. (see chart below).

We have no reason to doubt that the KSS will hit numbers in 4Q. There are a lot of factors at play, and it’s way too early to tell. But the ante chip just went up a notch and now KSS HAS TO hit estimates.

More after the call.