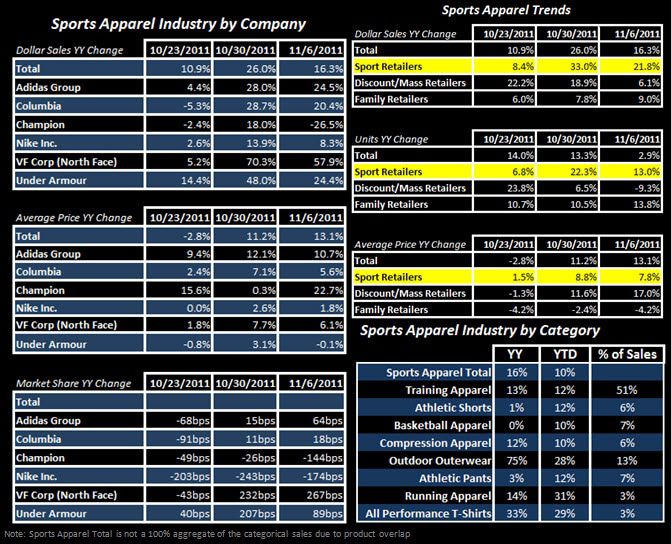

Sports apparel numbers continue to defy gravity. Let's see if the trend holds in the coming weeks when comps get tough. Regardless, the numbers look solid. Good for FL FINL DKS HIBB.

Sports apparel numbers continue to defy gravity. Let's see if the trend holds in the coming weeks when comps get tough. Regardless, the numbers look solid. Good for FL FINL DKS HIBB.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.