“A clever person solves a problem. A wise person avoids it.”

-Albert Einstein

Yesterday was not a good day for me. Today will be. This is the game. And I love playing it.

Yesterday, I couldn’t have been more confused between the intraday and end of day signals I was getting in my risk management model. In general, when that happens (and I’ve had to learn this lesson the hard way by getting whipped around), the best decision is to take down exposure and get out of the way.

So this, fortunately, is what I did:

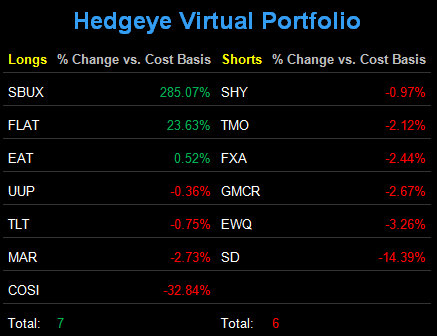

- Sold my US Equities in the Hedgeye Asset Allocation Model back down to 0% (from 6% on the open and 12% the week prior)

- Sold my LONGS in the Hedgeye Portfolio (different product) down from 9 LONGS on the open to 7 LONGS by the close

- Stayed with my best Global Macro long ideas – US Dollar (UUP), Long-term Treasuries (TLT), long UST Flattener (FLAT)

Unfortunately, staying with these long positions (UUP, TLT, and FLAT) made me feel shame yesterday. That’s what you should feel when you lose. Losing means you didn’t have it right. Winners need to lose before they can really learn how to win.

Intermediate-term to long-term investors have not been losing being long these positions for the last 6-9 months as it’s become clear that Global Growth Slowing will dominate Global Macro investing in 2011.

Most of the losers out there who focus on whining and finger pointing will obviously disagree with that statement – blame Europe or blame Canada for US GDP growth being 0.36% in Q1 or China slowing sequentially throughout the year – that’s easier, I guess.

There is nothing that’s been easy about investing in a globally interconnected macro marketplace in 2011. That will not change with French, Italian, and US Equities collapsing early this morning.

Ironically enough, Madame Lagarde seems to be geeking out on Le Chaos Theory this morning, prefacing her great depression fear-mongering speech to the last bastion of money printing – the IMF:

“In our increasingly interconnected world, no country or region can go it alone… there are dark clouds gathering in the global economy.”

Really?

On what part? The Lord Voldemort darkness of it all that is required to scare the hell out of people, or the socializing of losses part where only the young can dare “go it alone” in this world and bet on themselves?

If you thought all of this begging, banning, and printing was going to end well, you certainly didn’t get that call from me. In the last 4 years of ranting to you, I have to say that some days it really sucks to have to write about reality.

I’m on the same team as you. I am responsible for both my family and firm’s well being. I am looking to make this world a better place for my kids. But piling-more-policy-upon-policy is not the way out of this confidence spiral. It’s sucking the life out of capitalism.

Let us fail.

That’s the only way anyone on any team I have ever played on was really able to learn. Let me give-away the puck in front of 10,000 crazy fans wearing Badger red in Wisconsin (when my Mom is in the stands wearing blue) and let me hear that building light me up with insults like a Christmas tree in December for giving away a Yale goal.

Mucker, high and off the glass next time, eh?

Avoiding risk is important. It’s a process, not an emotional beta chasing point. Here are some of the most important lines in all of Global Macro to avoid “buying the dip” on:

- EUR/USD $1.37 – do not buy Euros on that breakdown if/when it occurs (buy US Dollars)

- SP500 – do not buy the SP500 if it cannot sustain itself above 1268 TAIL line resistance

- CAC40 (France) – do not buy French stocks if the intermediate-term TREND line of 3403 isn’t recovered

With everyone talking about Italy this morning, focus on France. We’ve been shorting Italy for 2-years and as of this morning it’s still crashing (down -34.5% from its YTD peak). Berlusconi is going away, but European Stagflation isn’t.

Focus on where the puck is going, not where it’s been. If I had to learn that risk management lesson from The Great One, so be it. I’ll take that over losing money today, all day long.

My immediate-term support and resistance ranges for Gold, Oil, German DAX and the SP500 are now $1, $94.01-97.07, 5, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer