THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

The NFIB Small Business Optimism Index rose in October for a second month, implying less pessimism on the outlook for sales and the economy. The Index climbed to 90.2, the highest level since June, from September’s 88.9 and consensus expectations for October of 90. The NFIB’s Chief Economist sounded cautious in his statement, however, saying “It’s hard to call it a recovery with unemployment about as bad as it was at the recession bottom.”

SUBSECTOR PERFORMANCE

QUICK SERVICE

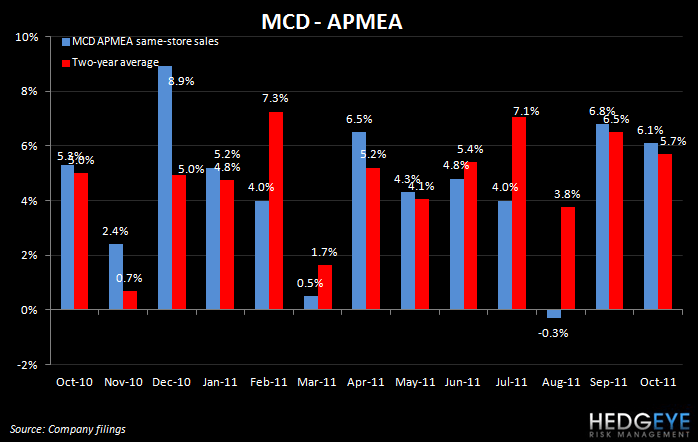

MCD: McDonald’s printed 5.5% global same-store sales for October versus expectations of 4.5% and guidance of 4-5%. The U.S. division saw comps grow 5.2% versus consensus of 3.7%. MCD Europe comps grew 4.8% versus the Street at 4.2% and APMEA came in at 6.1% versus expectations of 5.4%. If growth is slowing in Asia and Europe is sliding into the Mediterranean, mid-single digit one- and two-year trends are better than bad.

YUM: Yum! Brands’ Little Sheep acquisition has been approved by China’s commerce ministry. The acquisition cleared China’s anti-monopoly laws. Little Sheep is a hot-pot restaurant chain that operates in more than 400 restaurants in China. The acquisition was worth HK$4.4 billion (US$566 million), according to Bloomberg.

SBUX: Starbucks is rolling out mobile payments in Canada today.

DNKN: Dunkin’ Donuts announced 12 new restaurants in Des Moines, Iowa. The first is slated to open in 2012 and the last in 2018.

CASUAL DINING

CBRL: Cracker Barrel today began mailing its proxy statement for the company’s Annual Meeting of Shareholders to be held in December. Chairman Michael Woodhouse also sent a letter to the company’s shareholders urging them to elect the company’s nominees to the Board of Directors and to vote against the election of Sardar Biglari. The company’s track record, in terms of creating shareholder value over the last few years, may spur shareholders to seek some new direction.

MSSR: Tilman is to purchase McCormick and Schmick’s for $8.75 per share in cash. This is approximately a 29% premium to the closing price yesterday.

Howard Penney

Managing Director

Rory Green

Analyst