TODAY’S S&P 500 SET-UP - November 8, 2011

Top 3 on Bloomberg this morning: Olympus (fraud), Berlusconi (out?), and Cain (groping?). Nice! As we look at today’s set up for the S&P 500, the range is 13 points or -0.49% downside to 1255 and 0.55% upside to 1268.

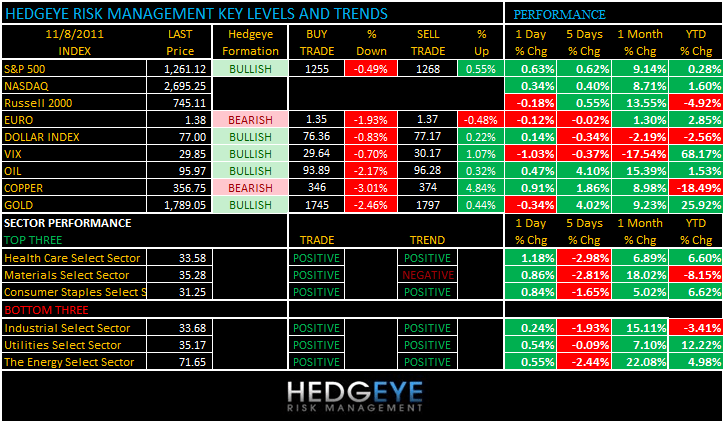

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -306 (+942)

- VOLUME: NYSE 782.75 (-9.14%)

- VIX: 29.85 -1.03 YTD PERFORMANCE: +68.17%

- SPX PUT/CALL RATIO: 2.30 from 1.57 (+46.30%)

CREDIT/ECONOMIC MARKET LOOK:

US TREASURY Yields – only up 3bps day over day to 2.03%, the long end of the US treasury market couldn’t care less about some of the lowest volume beta chasing rallies US stocks have ever seen. The 2011 call on Growth Slowing remains buy the long-bond (TLT)

- TED SPREAD: 44.14

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.04 from 2.06

- YIELD CURVE: 1.79 from 1.84

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30 a.m.: NFIB Small Business, est. 90.0 (prior 88.9)

- 10:00 a.m: IBD/TIPP Economic Optimism, est. 41.0 (prior 40.3)

- 10:00 a.m: JOLTS job openings, (prior 3056)

- 11:30 a.m: U.S. to sell $35b 4-wk bills

- 1:00 p.m.: U.S. to sell $32b 3-yr notes

- 1:00 p.m.: Fed’s Kocherlakota speaks in Sioux Falls, S.D.

- 1:30 p.m.: Fed’s Plosser speaks on monetary policy in Philadelphia

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- Election Day in the U.S. includes referendum in Ohio on collective bargaining rights

- Jefferson County Commission will consider filing the nation’s biggest municipal bankruptcy

- Olympus said 3 executives helped conceal decades of losses by paying higher fees to takeover advisers

- OPEC releases estimates on global oil demand, 8:30 a.m.

- U.S. Chamber of Commerce releases qtr economic briefing, 9 a.m.

- President Obama travels to Philadelphia

- New York City Mayor Michael R. Bloomberg will join the Center for American Progress and the American Action Forum for a discussion on deficit reduction in Washington. 10 a.m-11 a.m

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Oil Rises to Three-Month High on Signs of Shrinking U.S. Stocks

- Cargo to U.S. Dropping for First Time Since End of 2009: Freight

- Damaged U.S. Corn Crop Pressures Global Food Supply: Commodities

- Gold Drops After Reaching 7-Week High on European Debt Risk

- Carbon Plan Passed by Senate as Gillard Seeks Public Support

- Stocks Gain, Euro Pares Drop as ECB’s Stark Predicts Crisis End

- Copper Advances First Day in Three on Strike, Inventory Drop

- Diesel Supply Falls to 31-Month Low in Survey: Energy Markets

- Copper May Slip Below $7,635 a Ton: Technical Analysis

- Palm Oil Climbs to Seven-Week High as Production Poised to Slow

- Buy Corn, Sell Wheat in 2012 as Gap Set to Narrow, Bowler Says

- Copper May Advance on Signs of Reduced Supplies: LME Preview

- Gold May Decline as Rally to Six-Week High Spurs Investor Sales

- AB Foods Sees Sales, Profit Gaining as Commodity Costs Ease

- Coca-Cola Hellenic Profit Falls on Higher Commodity Costs

- Oil Climbs to Three-Month High on Possible New Leaders in Europe

- Hedge Funds Curb Wagers for First Time in a Month: Commodities

CURRENCIES

EUROPEAN MARKETS

ITALY – oh the drama – with bond yields only down -4bps d/d to 6.62% and Italian Equities still in full crash mode (down -33% since 2011 YTD highs, despite these fun little short squeezes “off the lows”), other than having an Italian running the ECB buying everything he can that is Italian sov debt here, what else do we need? Silvio says “look into my eyes”…

ASIAN MARKETS

JAPAN – on a huge fraud (Olympus) the Nikkei broke its only remaining line of TRADE support (8835) and sliced back down to -15.3% for the YTD; plenty “value” investors bought Japan on the “tsunami recovery” thesis – hearing crickets on that thesis now…

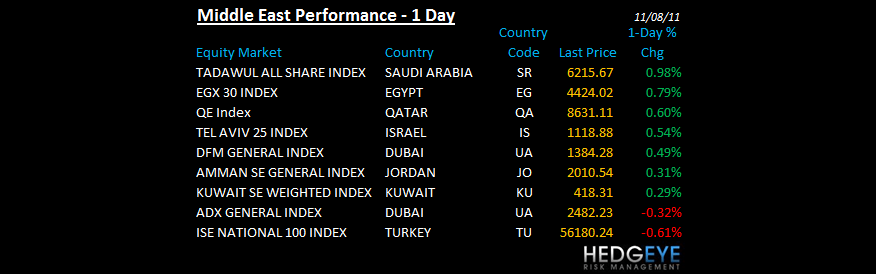

MIDDLE EAST

MOST POPULAR MIDDLE EAST HEADLINES FROM BLOOMBERG

- UN Report May Show Iran Is Moving Closer to Nuclear Bomb

- Gulf Keystone Upgrades Volumes for Shaikan Discovery

- Russia Says Timing of UN Report on Iran Nuclear Weapons ‘Wrong’

- Gulf Keystone Revises Shaikan Resources to 8b-13.4b Barrels

- Lavrov Says Iran Attack Would Be ‘Very Serious Mistake’: Reuters

- Mubadala Development Owns 9.85% of Swedish Auto, Filing Shows

- Doha Bank Considers 2012 Acquisition in Emerging Market

- Medvedev Condemns Israel’s ‘Dangerous’ Threat of Iran Strike

- Iran Ready And Able to Build a Nuclear Bomb, UN Watchdog Warns the Wor

- Mol Advances Most in Week After Iraqi Oil Estimate Upgrade

- Gulf Times (QA): Fresh clashes in Bahrain

- Econ Times (IN): Russia warns against military strike on Iran - The Econo

- Aramco Cuts Asia Oil Differentials, Lifts U.S.: Persian Gulf Oil

- Zain Iraq Hires Advisers for Initial Public Offering: FT

- Iran on Verge of Building Nuclear Weapon, Washington Post Says

- Syrian Opposition Calls Homs ‘Disaster Area’ Amid Siege

- Oil rallies to seven-week high ahead of IAEA report on Iran

The Hedgeye Macro Team

Howard Penney

Managing Director