McDonald’s will announce October sales before the market open on 11/8.

McDonald’s reported stronger-than-expected sales and EPS for 3Q which has given the stock a boost. September sales were especially strong, with global comps coming in at +6.6% versus expectations of +3.9%. APMEA was the largest upside surprise, with comps at +6.9% versus consensus at +2.7%. Europe printed the same number, versus the Street at +3.3%. The US came in at +5% versus expectations of 4.1%.

During the third quarter earnings call management struck a positive tone and gave October-to-date global comps, as of 10/21, of between +4% and +5%. Consensus seems to be clinging to the low end of that range at 4.1%, according to Consensus Metrix. Judging by the Consensus Metrix data, the consensus numbers of 3.42% and 4.27% for Europe and APMEA, respectively, imply a sequential decline in two year average trends in October. While Europe was helped in September by a calendar shift related to Ramadan which alone may make a sequential decline two-year average trends more likely, the turmoil in Europe is also a concern. Also a concern is slowing growth in Asia, which could negatively impact APMEA comps. However, growth was slowing in September as well and MCD posted an impressive +6.9% comp that month. Growth in important APMEA markets such as China and Australia has been trending lower throughout the year. We believe there could be upside risk to the consensus figures in those two divisions.

Compared to October 2010, October 2011 had one less Friday and one additional Monday. As a result, we would expect a negative calendar shift. In January 2011, when there was the same calendar shift versus January 2010, the impact was between -1.3% to -0.4% varying by area of the world. For the purposes of this post we are assuming that the same calendar shift occurred in October 2011.

Below we go through our take on what numbers will be received by investors as good, bad, and neutral, for MCD comps by region. For comparison purposes, I have adjusted for historical calendar and trading day impacts and make the aforementioned assumption for October 2011’s calendar shift.

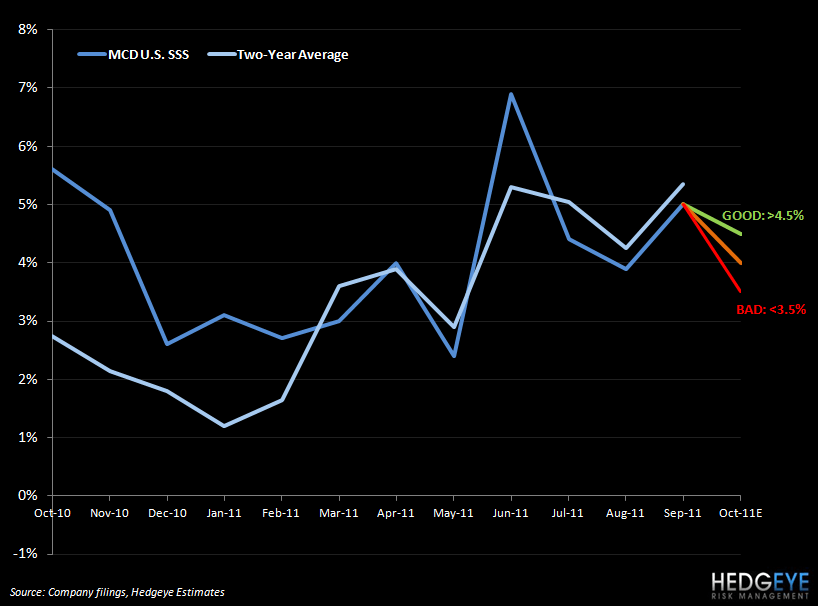

U.S.: facing a compare of 5.6% (including a calendar shift which impacted results by -0.2% to +1.2%, varying by area of the world).

GOOD: A print above 4.5% would be considered a good result, as it would imply a sequential acceleration in two-year average trends in October. Following what was a strong month in September, a further acceleration would be a good indication for the strength of the domestic business.

NEUTRAL: A number between 3.5% and 4.5% would be considered neutral given that, on a calendar-adjusted basis, the midpoint of the range would imply trends that are roughly in line with September. We are holding the domestic business to a high standard because we believe that investors are expecting MCD to continue to take share in the U.S.

BAD: A number below 3.5% would imply a sequential deceleration in two-year average trends which would be received as a bad result by investors. Given the high standard MCD has set, a deceleration – especially after the 10/21 guidance of 4-5% global comps – would be a disappointment.

Europe: facing a difficult compare of 5.8% (including a calendar shift which impacted results by -0.2% to +1.2%, varying by area of the world).

GOOD: A print of 4% or higher would be received as a good result by investors because, while it could imply a sequential deceleration in two-year average trends, two-year average trends would still be in line with the year-to-date average and far in excess of the poor trends in August (albeit impacted by Ramadan shift).

NEUTRAL: A number between 3% and 4% would be interpreted as a neutral result by investors, as two-year trends would have deteriorated somewhat on a sequential basis but would still be roughly level with year-to-date trends on a calendar-adjusted two-year average basis.

BAD: Below 3% would be received as a bad print from a headline perspective; any comp below 3% is low for MCD Europe. August was a case of an unfavorable Ramadan-related calendar shift impacting traffic but a repeat in October could lessen investor confidence.

APMEA: facing a compare of 5.3% (including a calendar shift which impacted results by -0.2% to +1.2%, varying by area of the world).

GOOD: A print of more than 5.5% would be received as a good result by investors. While this result would imply a sequential decline in two-year average trends, the absolute level would be above the year-to-date average calendar-adjusted two-year average trend. Growth has been slowing in important APMEA countries and this has been reflected in APMEA comps, therefore we feel that a calendar-adjusted two-year average trend between 5.5% and 6% (which a 5.5% print would imply) would be received well by investors.

NEUTRAL: A result of 4.5% to 5.5% would be received as neutral by investors.

BAD: A print of less than 4.5% would be interpreted as a bad result by investors as it would imply a strong decline in two-year average trends.

Howard Penney

Managing Director

Rory Green

Analyst