Early November GGR forecast of HK$20-22 billion

Average daily table revenues for the first 6 days of November slowed to HK$639 million from HK$678 million in the last week of October. One week of data doesn’t make a trend and we don’t know the impact of hold. We would caution, again, that November is likely to display a sharp slowdown from October (see “An Eye on November” published on 11/02/11). October contained Golden Week, 31 days, and a high VIP hold percentage. Our projection for full month November Gross Gaming Revenues is HK$20-22 billion, up 19-31% YoY. At the midpoint of that range, HK$21 billion, November would represent a 19% MoM decline.

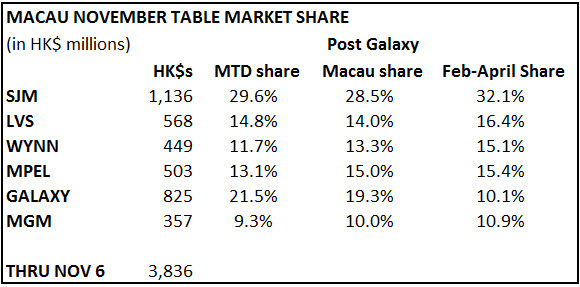

Market shares are pretty irrelevant at this point but SJM and Galaxy had the strongest week.