This note was originally published at 8am on November 02, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Equality of outcome is a form of inequality.”

-Paul Ryan

As I sit here in my hotel room in San Francisco this morning, the elephantine intellects of the Fiat Fool system continue to attempt to centrally plan us towards “equality.” Meanwhile, markets are producing very Unequal Outcomes.

Instead of stability, we have volatility. If the +41.9% rip in the Volatility Index (VIX) in the last 3 days isn’t a reminder of that, I don’t know what is…

My longest of long-term theses about Big Government Intervention and money printing remains. From Japan, to the USA, to Europe, and back again, Fiat Fool policies to inflate A) shorten economic cycles and B) amplify market volatility.

Back to the Global Macro Grind…

Get the US Dollar right, and you’ll get mostly everything else right. As bad as I looked being long the US Dollar last week is as good as my team looks this week. The US Dollar has put on an impressive +3% move, recovering its TREND line of support (75.37 on the US Dollar Index), and mostly every asset class price that’s inversely correlated to that has fallen, hard.

Since I shorted the SP500 on Thursday at 1290 (Time Stamp), US stocks have had a straight down correction of -5.6%, taking the SP500’s correction from its 2011 YTD high (April) back to a double digit loss (-10.6%). Longer-term, like Japanese stocks, the SP500 has crashed from its all time peak (down -22.2% from October 2007). Bull market?

With all but 3 country stock market indices in the entire world negative for the YTD, this is obviously not a bull market in equities. It’s a bull market in long-term US Treasuries. It’s a bull market in volatility. But these asset classes are pricing in very Unequal Economic Outcomes.

Update on the Eurocrat Bazooka:

This morning Old Wall Street’s finest brokerages tried to fire the first mini-missile of EFSF bond issuance from Ireland, and had to abort mission! Given that this was the 1st €3B of €600 or so BILLION of these fiat issues coming down the pike, I’d say that’s really not good.

Inclusive of attempts to ban short selling, ban CDS trading, and ban gravity, European markets have already been telling you how this sad story of Keynesian spending and leverage ends…

- Germany’s DAX snapped its TREND line of 6112 yesterday and is crashing again (down -22% from its 2011 peak)

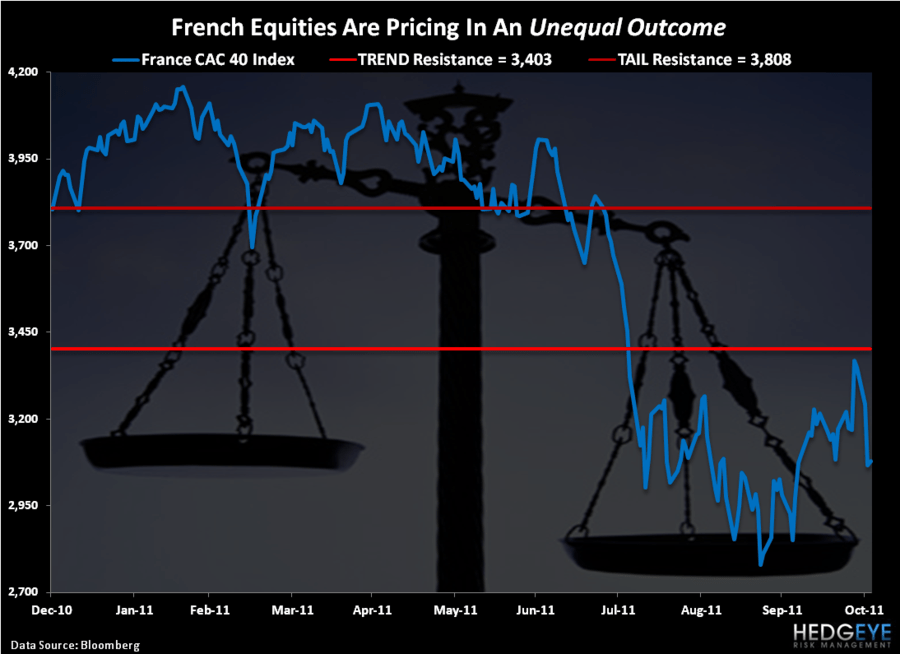

- France’s CAC never recovered its TREND line of 3403, and continues to crash (down -26% from its 2011 peak)

- Greece’s Athex Index never recovered a risk management line of consequence in the last 12 weeks (down -56% from its 2011 peak)

Never mind the €2-3 TRILLION Bazooka, these professional politicians can’t sell the world on €3B in bonds!

The European Sovereign Bond market gets this obviously. In fact, they didn’t suspend disbelief like stock market people did last week either. Italian and French sovereign debt yields continue to make a series of higher-highs, reminding you that piling-debt-upon-debt-upon-debt structurally impairs economic growth.

Setting aside the differences between Europe, Japan, and the US, that’s the story of the Fiat Fools that isn’t getting its “fair share” of air-time, yet (Obama’s team is working on rectifying this inequality). The part about causality. The part that would require these central planners to accept responsibility for the bigger problem than maybe even the banks themselves – Growth Slowing.

If Growth Slowing takes Europe’s economy into the negative 1-3% GDP zone as inflation spikes into the +3-6% range, what do you get?

European Stagflation.

Stagflation earns the lowest multiple for stocks (read: in the 1970s, the SP500 traded at 7x earnings 3 different times in the same decade). Why is that so? Simple: the combo of Growth Slowing and Margins Compressing is the kiss of the “value” investor’s death.

That’s the bad news. And it’s a European problem that perversely could result in a Strong US Dollar which, in turn, would Deflate The Inflation in America (think commodity prices). In the long-term, while these are very Unequal Global Macro Outcomes relative to how the central planners of the 2011 Fiat were thinking, this should only perpetuate global economic volatility in the short-term.

As for the “price stability”, stay tuned for the Bernank’s latest on that at his 1230PM EST press conference.

My immediate-term support and resistance ranges for Gold (bullish TRADE and TREND), Oil (bullish TRADE; bearish TAIL), German DAX (bearish TRADE, TREND, and TAIL) and the SP500 (bullish TREND; bearish TAIL) are now $1710-1785, $91.16-93.87, 5828-6119, and 1213-1248, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer