Higher hold contributed over 10% of the 42% YoY growth. November GGR should fall significantly MoM.

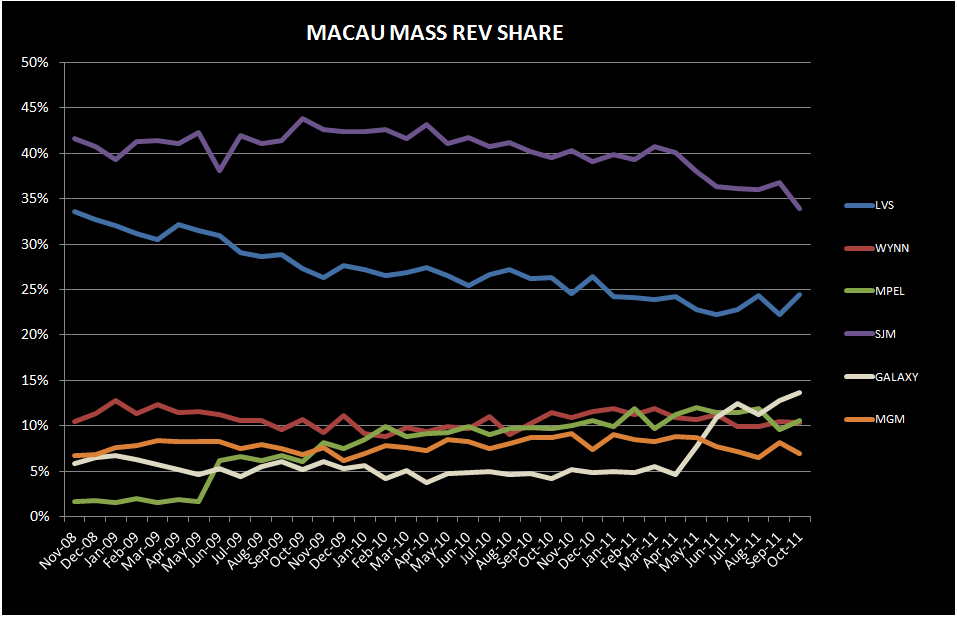

As previously disclosed, October gross gaming revenues (GGR) increased 42% YoY to $3.35BN. With the detail in hand, we can confirm that while growth was strong, the month got a boost from good hold and an easy hold comparison from last October. Total direct play this month was 6.3% of the market, compared to 7.5% last year. The total market held at 3.05% vs. 2.70% in October 2010. Normalizing for hold, October would have increased 30% YoY. High margin Mass business increased 36%, just slightly lower than the 40-41% growth we’ve seen during the last 4 months.

As we approach the next 3 months of the year we expect YoY growth rates to decelerate, partly due to difficult hold comparisons and trends we are seeing in our sequential monthly projections (see “MACAU: EYE ON NOVEMBER” published on 11/2/11). Hold rates for November 2010 through January 2011 ranged between 3.05% and 3.13%. Normal hold levels would alone shave roughly 10% off YoY growth.

Y-o-Y Table Revenue Observations

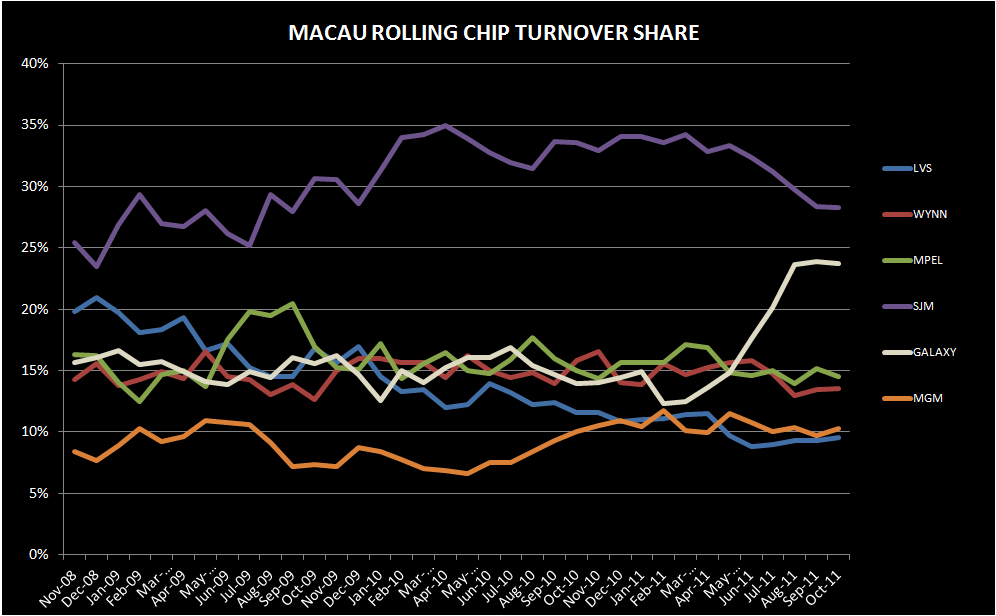

Total table revenues grew 43% YoY this month, on top of 50% growth last October. October Mass revs rose 36%; VIP revs grew 45%; and Junket RC rose 30%.

LVS

Table revenues grew 5% only YoY – exhibiting the slowest concessionaire growth in the market, in-line with recent trends. We’ll be keenly watching for a turnaround in November since we’ve heard that LVS has been extending additional junket credit and 2 new junkets are coming online at the Four Seasons this month. Over the last 5 months LVS’s table revenues have grown at 14% while the market has grown 48% - roughly 30% of the market’s pace.

- Sands was down 6% YoY, driven by low hold. The YoY decline was driven by a 15% drop in VIP which was somewhat offset by 12% increase in Mass.

- Junket RC was up 21%

- Sands held poorly in October and had a difficult YoY comp. Adjusted for 14% direct play (15% in 3Q11), hold was about 2.05%, compared with 3.00% hold in October 2010 assuming 15% direct play (in-line with 4Q10).

- Venetian was up 8% YoY, driven by a Mass increase of 28% offset by a 4% drop VIP

- Junket VIP RC fell slightly, down 1%

- Assuming 23% direct play in the quarter (just slightly below the 24% we saw in 3Q11), hold was 2.99% compared to 3.12% hold in October 2010 assuming 19% direct play (in-line with 4Q10)

- Four Seasons grew 17%YoY, driven by an 89% increase in Mass VIP revenues and a small 3% increase in VIP revenue.

- Junket VIP RC increased 10% YoY

- While we believe that the property held low, the comparison was also very easy. Assuming 36% direct play (which is close to the 38% in 3Q11 and implies a 19% sequential increase in average monthly direct play levels), hold was 2.65% in October, compared with a hold rate of 1.82% if we assume 54% direct play in October 2010 (in-line with 4Q10)

WYNN

Wynn table revenues were up 36%, which benefited from an easy hold comparison

- Mass was up 23% and VIP increased 40%

- Junket RC increased 11%

- Assuming 10% of total VIP play was direct (in-line with 3Q11), we estimate that hold was 2.9% compared to 2.3% last year (assuming 11% direct play – in-line with 4Q10)

MPEL

Table revenues grew 49% - equally driven by Mass and VIP

- Altira revenues rose 28% with Mass growth at 18% while VIP grew 29%, helped by an easy hold comparison

- VIP RC increased 14%

- We estimate that hold was 2.9% vs. 2.7% last year (direct play is not material at Altira)

- CoD table revenue was up 62%, driven by 57% growth in Mass and 64% growth in VIP – helped by high hold and an easy comparison

- Junket VIP RC grew 37%

- Assuming a 13% direct play level, hold was 3.4% in October compared to 2.6% last year

SJM

Revs grew 15%

- Mass was up 17% and VIP was up 14%

- Junket RC was up 10%

Galaxy

Table revenues continued its streak of triple-digit gains, +201%; mass soared 340%, while VIP gained 186%

- StarWorld table revenues grew 64% - exhibiting the best growth of any mature property

- Mass grew 56% and VIP grew 65%, helped by high hold and an easy comp

- Junket RC grew 28%

- Hold was high at 3.1% compared to just 2.5% hold last October

- Galaxy Macau's total table revenues were $339MM, 41% higher than September’s

- Mass table revenues rose 29% MoM to $59MM

- VIP table revenue of $280MM, a 43% MoM increase, helped by luck. Hold was 3.4% this month vs. 2.8% in September.

- RC volume of $8.3BN, up 19% MoM

MGM

Table revenue increased 50% YoY, helped by high hold in the quarter

- Mass revenue growth was 9%, while VIP grew 60%

- Junket RC increased 24%

- Assuming a direct play level of 8%, we estimate that hold was 3.6% this month vs. 3.0% in October 2010, also assuming direct play of 8%

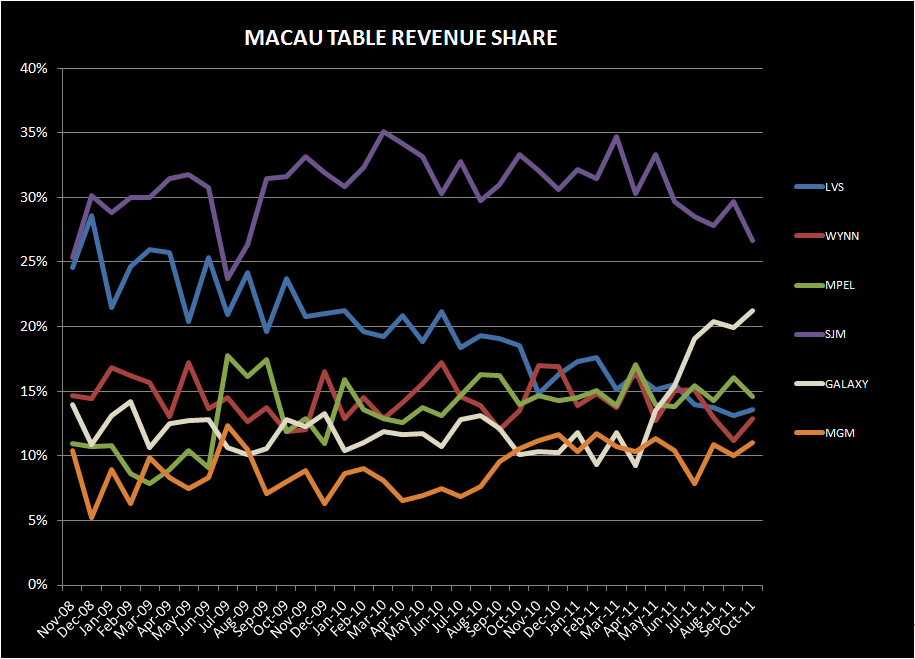

Sequential Market Share (property specific details are for table share while company-wide statistics are calculated on total GGR, including slots)

LVS

Share increased 40bps sequentially to 14.1%. This compares to 6 month trailing market share of 15.1% and 2010 average share of 19.5%

- Sands' share ticked up 10bps to 3.5% off of all time lows in September

- Mass rev share fell 30 bps offset by a 50bps improvement in VIP share

- Venetian’s share fell 40bps sequentially to 8.1% share

- VIP share fell 1% to 5.9%, below the prior TTM average of 6.8%

- Mass share gained 1.5% sequentially to 15.5% - above the 14% average for the trailing 6 months

- Junket RC fell 20bps to 4.7%

- FS share improved 80bps to 2.0%

- VIP share increased 1% to 1.9%

- Mass share ticked down 10bps to 2.3%

- Junket RC improved 20bps to 1.5%

WYNN

After hitting an all-time low in September market share, WYNN was the largest share gainer in October – gaining back 1.6% to 13.1% share - although still below their 6 month trailing average share of 14.2% and 2010 average share of 15%. Wynn’s share should continue to struggle with the opening of Sands Cotai Central in March and with the introduction of new junkets at the Four Seasons this month.

- Mass market share fell 20bps at 10.3%

- VIP market share increased 2.2% to 13.6%

- Junket RC share was flat MoM at 13.5%, below its 6 month trailing average of 14.7% and 2010 average of 15.2%

MPEL

Market share fell 1.5% points to 14.7%, below than its average 6 month trailing share of 15.2% but above its 2010 share of 14.6%.

- Altira share fell 50bps to 4.7%, compared to a 5.6% average share in 2010; Mass share fell 10bps while VIP share dropped 1%.

- CoD’s share dropped 80bps to 9.9% driven by share losses in VIP that were partly offset by strength in Mass

- Mass market share increased 1.1% points to 9.1%

- VIP share fell 1.5% points bps to 10.1%

SJM

In a reversal from last month SJM lost the most share in October, down 3.0% to 26.0%, their lowest share since August 2009 and below its 6-month trailing average of 29.2% and 2010 average of 31.3%.

- Mass market share dropped 2.8% to 33.9% - an all-time low

- VIP share fell 2.8% to 24.5%

- Junket RC share ticked down 10bps to 28.3% - their lowest share since Sept 2009

Galaxy

Gained 1.3% share to 20.9%. October share compares with an average share of 10.9% in 2010 and a 6 month trailing average of 16.0%.

- Galaxy Macau share gained 1% to 10.5%

- Mass and VIP market share gained 90bps to 8.2% and 11.2%, respectively

- RC share ticked down 20bps to 10.8%

- Starworld lost 40bps of market share to 9.2%, 10bps above its TTM share of 9.1% pre-Galaxy Macau level.

MGM

Gained 1.1% to 11.2% due to an improvement in VIP share. October share compares with an average share of 10.3% in 2010 and a 6 month trailing average of 10.4%.

- Mass share lost 120bps to 6.9% but was more than offset by a 160bps decrease in VIP share to 12.2%

- Junket RC gained 60bps to 10.3%, above the property’s 2010 average of 8.4% and in-line with its 6 month trailing average of 10.4%

Slot Revenue

Slot revenue grew 18% YoY and increased $2MM sequentially.

- As expected, Galaxy slot revenues grew the most with 309% YoY to a record of $16MM

- MGM slot revenues had the second best growth at 24% YoY to $20MM – an all-time high for the property

- Wynn slot revenues grew 11% YoY to $25MM

- MPEL slot revenues grew 3% YoY to $22MM

- SJM slot revenues grew 7% YoY to $14MM – down from $17MM in September

- LVS slot revenues fell 3% YoY to $33MM