Conclusion: Romney looks poised to win the Republican nomination, but Obama is looking increasingly difficult to beat.

Our Macro Team was on the road this week meeting with clients on the West Coast and inevitably politics came up as part of the macro discussion. As most macro traders know, policy and policy makers are key factors in determining the future price direction of various asset classes. Specifically, both monetary and fiscal policy shape interest rate policy and, eventually, the price of key currencies.

In theUnited States, this coming year is obviously a Presidential Election year. Barring an unforeseen development, the showdown over the Presidency will be between President Obama and former Massachusetts Governor, Mitt Romney. Despite the media trying to make the Republican nominating process seem competitive, it is anything but competitive.

According to InTrade, Romney is currently at 70.1% probability of gaining the nomination. The rest of the field is very distant, with Perry at 11%, Gingrich at 8%, and Cain at 5%. Interestingly, the most recent national poll of the Republican front runners suggests a slightly closer race with Romney at 25%, Cain at 23%, Perry at 14%, and Gingrich at 12%. From our perspective, while polls can be instructive, predictive markets tend to be more accurate. Further, the primary calendar plays very well into Romney’s strategy.

The early caucuses or primaries in January and February are outlined in the table below:

In aggregate, of the first ten primaries or caucuses, Romney appears poised to win six handily and in the remaining four, he is in a tight race with Herman Cain. (Incidentally, most of these polls were taken before the recent Cain sexual harassment scandal). The key surprise could well be that Romney does better than expected in Iowa and then goes for close to a clean sweep in January and February, which would effectively end the race early. This appears to be the scenario that is priced into the InTrade contract.

So, assuming this race very quickly becomes Obama versus Romney, does President Obama stand a chance? According to a preponderance of political strategists, many pertinent economic indicators, and relevant approval polls, President Obama will be a one term President. A few key points to consider (hat tip to Karl Rove for collecting this data):

- No President has ever been re-elected with 74% of American saying the country is on the wrong track a year before the election;

- No President has ever been re-elected with so few Americans, 13% according toGallup, saying they are satisfied with the way things are going;

- No President has been re-elected with unemployment at 9% a year prior to the election; and

- No President has been re-elected with a job approval as low as Obama currently has.

Sounds dismal for Obama, right? Well, not so fast.

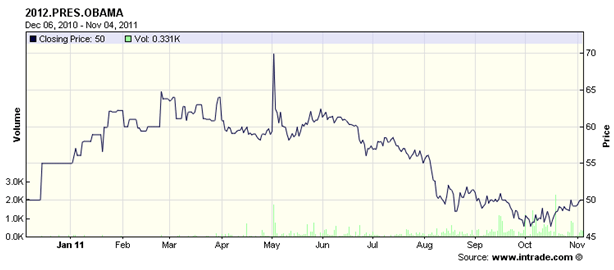

According to InTrade, Obama is now at 50.5% on the contract as to whether he gets re-elected, which suggest a more than 50% probability. As outlined in the chart below, this is off the lows of early October. Now, clearly there is some correlation to the massive positive move in the U.S. stock market we’ve seen in October. Nonetheless, Obama is a long ways from a sure thing as a one term President.

According the to the Real Clear Politics aggregate, Obama trails the generic Republican challenger by about +3 points. This spread is within the margin of error and overtime has consistently indicated a slight lead for the generic Republican. Conversely, when polled against the actual Republicans, Obama does well. For instance, Obama has consistently outpolled Romney for the last month by either tying or beating him in every poll, and currently leads by +1.9 points. As for the rest of the field, it isn’t even close as Obama demolishes them head-to-head.

So far, at least, voters seem to be siding with the devil they know, versus the devil they don’t. In addition, there is a clear and definitive incumbency advantage for in Presidential elections as, according to a paper by David Mayhew, the incumbent has been re-elected 2/3s of the time versus 50% of the time when the there was no incumbent running. The real risk for the Republican candidate is that the economy and stock market improve in 2012, even if only marginally. This scenario could take a marginal Obama lead to a solid re-election.

Daryl G. Jones

Director of Research