“The fear of another great inflation remained with him all his life.”

-Niall Ferguson

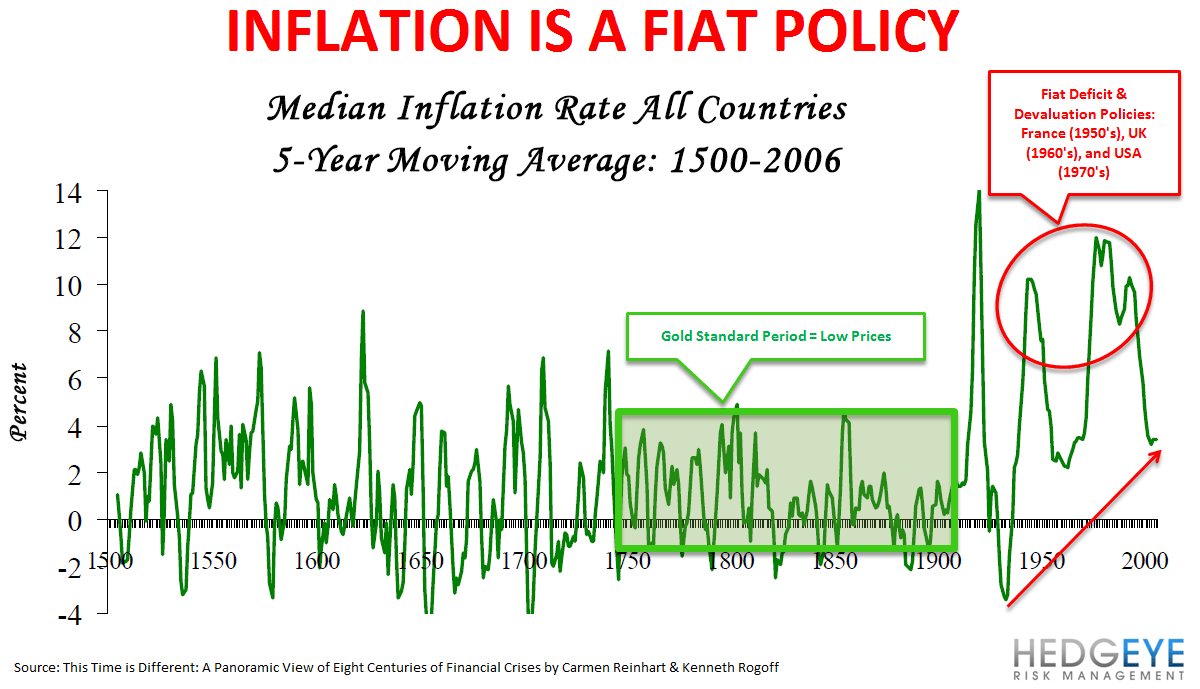

Inflation is a centrally planned policy. Period.

History is littered with examples of governments devaluing their fiat currencies for short-term political resolve. Keynesians can call their goals “price stability” and “full employment” all they want. The People are starting to call that a joke. In the long-term, banning both gravitational forces and the truth about long-term prices will be difficult.

The aforementioned quote comes from an excellent book that I am in the middle of studying – Niall Ferguson’s High Financier – The Lives and Times of Siegmund Warburg. In the Post 1913 Federal Reserve Act Period (Chart of The Day), there are very few merchant bankers (not to be confused with central or too-big-to-perform bankers) who rival Warburg’s legacy.

What’s most interesting to me about Warburg (like it is with most revolutionary capitalists), is where he came from. Context and experience are some of the things I personally thank God for every day of my life. For Siegmund Warburg, context and experience are what made him the change that the British and American banking systems needed to see.

“I brought something to England which was a little bit different because I was a damn foreigner, a German Jew.”

-Siegmund Warburg (High Financier, page 233)

You don’t have to take my word for it on any of this. I’m just a Canadian who came to the American Financial Empire in 1995 and studied the source code of Keynesian economic dogma at Yale in my cutoff jean shorts.

Take Harvard’s word for it – Ferguson’s book has 104 pages of footnotes.

You don’t have to take Warburg’s word for it either – few in the Establishment of the British economic elite did after he became a British citizen in 1939. But when a post WWII debt-laden England resorted to debauching the British Pound, Warburg called them out on it, big time.

Great Inflations?

Warburg lived through Germany’s hyperinflation of the 1920s and the politicized central banking that perpetuated it. Today’s good ole boy network money printing is not a new strategy. We don’t have that hyperinflation (yet) either. But the manic financial media seems hell bent on cheering on its catalysts.

WTIC and Brent Crude oil prices are trading at $95 and $112/barrel this morning. Deflation? Pull up any long-term chart that doesn’t use 2008’s $150/barrel oil price as its anchoring point in the analysis (all-time high), and you’ll conclude what every man, woman, and child from Kenya to Vietnam already has – Keynesian monetary policies are exporting generationally high levels of food and energy inflation.

Warburg didn’t believe in trading prop, levering up his client deposits, or front-running client capital. His strategy was to simply keep his bank’s balance sheet liquid and conservatively positioned throughout the British and French currency devaluations of the 1950s and 1960s. He also avoided getting train wrecked by the US Dollar Devaluation that ensued under Nixon and Carter in the 1970s.

Warburg fundamentally believed that “inflation was primarily a political phenomenon caused by governments who do not have the courage to either reduce their expenditure or to cover it by taxation.” (High Financier, page 36). Sound familiar?

The sad and pathetic reality about Western Economic Leadership in the 21stcentury (read case studies of both Bush/Obama US Administrations, the 8 or 9 Japanese PM’s they’ve had in the last decade, or … uh, Europe!), is that this is all very familiar.

“To sin by silence when they should protest makes cowards of men.”

-Abraham Lincoln

The metaphor that Ferguson and I make between the British Empire’s peak (then) and America’s (potentially now) is a very important debate that needs to be had. If we repeat history’s mistakes, our children have no business forgiving the elephantine intellects endowed upon us from our Ivy League institutions.

In the late 1940’s and early 1950’s Warburg was at least as critical of British policy as Hedgeye and many others are of US fiscal and monetary policy today.

Then?

“By the September 1949 devaluation, which saw the Pound’s dollar value reduced by 30% from $4.03 to $2.80, his Wartime enthusiasm for Labour had waned significantly… he argued in a highly critical memorandum written in August of that year … The country was spending too much on defence. Profits and pay were on a much too high level… the employers indulge frequently in illusions as to the profits …” (High Financier, page 131)

Now?

But, but, but … if you don’t adjust them for inflation, ‘corporate profits are great’… and we continue to beg for The Bernank and/or the Italian Job from Super Mario, to cut, print, cut… beg, cut, print… print, bail, cut…

If you’ve been awake since 2006 and watched Big Government Interventions A) shorten economic cycles and B) amplify market volatilities, you get it. Great expectations for Great Inflations have become the root of the common man’s heartache.

My immediate-term support and resistance ranges for Gold, Oil, German DAX, and the SP500 are now $1, $92.66-94.86, 6105-6413, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer