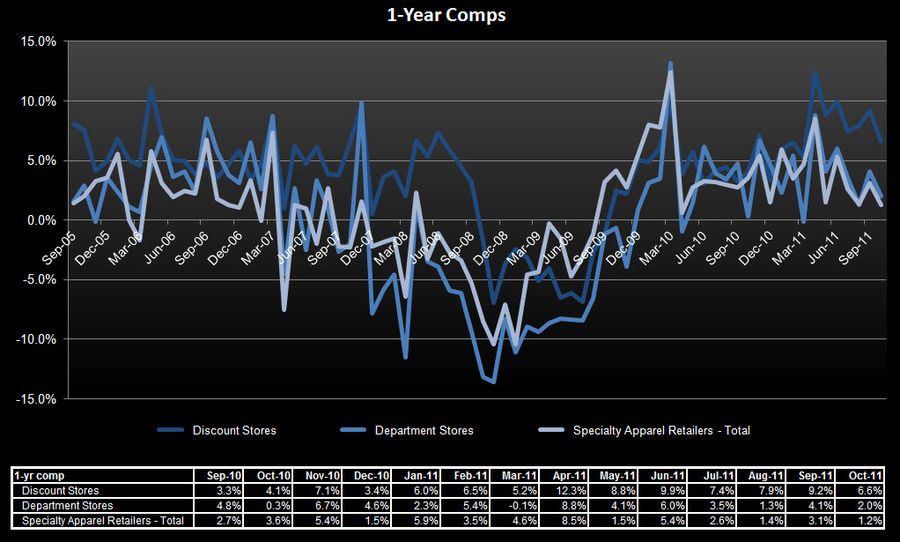

This morning’s sales reports reinforce our standing view that Q3 is setting up to be the worst in two-years. Following a choppy August BTS season, September sales came in better than expected setting the stage for what turned out to be a very disappointing October to cap off Q3. Perhaps the biggest callout out of October numbers is the swing in top-line trends. This is stating the obvious – we realize; however, recall that sales came in stronger than expected, but weren’t translating to commensurate bottom-line growth last month. Now both top-line AND bottom-line trends are rolling heading into Q4. The result is widespread revisions for both Q3 as well as for the full-year. In addition to continued weakness in low-to-mid tier markets, the spread between high-end outperformance relative to the low-end narrowed in October reflecting incremental weakness at the high-end. Despite the chink in high-end demand, the low-to-mid-tier retailers (e.g. BONT, SSI, JCP, etc.) are slowing at a faster rate. We still firmly think there will be an increased bifurcation between upward and downward revisions in retail over the next quarter and into 2012.

A few additional callouts in October:

- The High/Low-end performance spread has narrowed. Within department stores, Neimans +8% and JWN +5.4%continue to post solid results while SKS +1.8% and M +2.2% came in weaker than expected and more in-line with KSS, +3.9%, TJX +3%, and SSI +0.8%. The clear underperformers were JCP -2.6% and BONT -10.2%.

- Consistent with recent months, Discounters continue to be among the strongest performing segment of retail. This is likely due to greater grocery exposure, which continues to be a key category. Retailers with exposure there (TGT up low-teen and COST up DD) fared better than most with COST betting expectations and TGT coming in light, though still up +3.3%.

- JCP was again a clear negative callout. While the company didn’t revise its guidance, it should have and we expect it to when they report next week with Q3 comps coming in down -1.6%. The Street’s at $1.19 for Q4, we’re shaking out under a buck. A consistent disappointment of late is the company’s e-commerce, which posted its third straight decline down -4.5% with comps ahead only getting tougher. This continues to defy explanation as e-commerce is one of the few positive channels for any retailer not named JCP.

- Lastly, we have to callout HBI admitting that it got its forecasting wrong on last night’s call. Compounding the error, they also highlighted that after a tough August, strong sales in September and October should reaccelerate order demand. Perhaps they should have held the call until after retailers reported October sales as that certainly doesn’t appear to be the case.

The bottom-line is that sales are now getting weaker across the board – including at the high-end. However, the domestic mid-tier market continues to experience a more aggressive roll in both top and bottom line results setting up for increased volatility heading into year-end. We would still avoid most names that touch the domestic mid-tier market.

Shorts: JCP, HBI, UA, GIL

Longs: LIZ, WMT, NKE

Casey Flavin

Director