THE HEDGEYE BREAKFAST MENU

Notable macro data points, news items, and price action pertaining to the restaurant space.

MACRO NOTES

Initial jobless claims came in at 397K versus 400k expectations and a revised 406k in the week prior. The drop below the 400,000 threshold in the latest week was better than expected improvement and puts initial jobless claims at their lowest level since late September; the downtick in claims points to slowly improving economic data. Continuing claims dropped in the prior week.

Bloomberg Consumer Comfort Index fell to -53.2 in the latest week the second-lowest reading in almost 26 years of data. The index has held below -50 for six of the past seven weeks; a period unmatched even during the 2008-2009 recession.

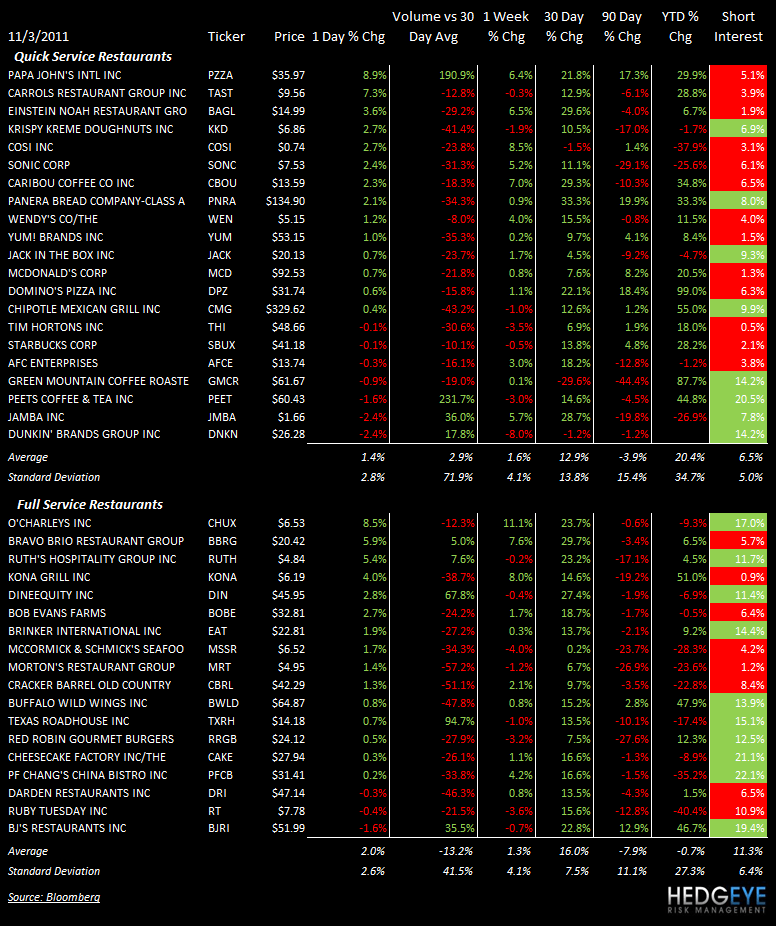

SUB-SECTOR PERFORMANCE

HEDGEYE RESTAURANT RESEARCH CALLS

WEN: Wendy’s top-line has strengthened thanks to advertising and the new burger. We now like Wendy’s on the long side from a TRADE (3wks or less) and TAIL (3yrs or less) perspective. We have no stance on the TREND (3mos or more).

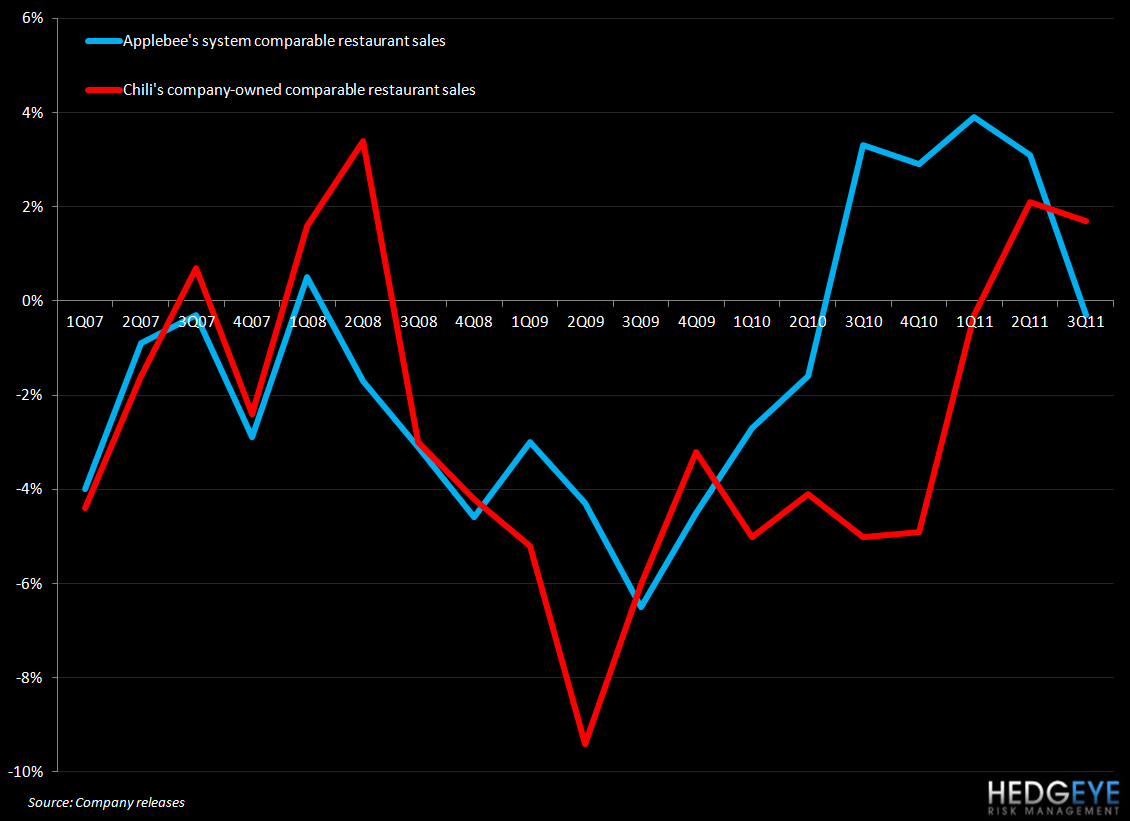

EAT: We like Brinker on the long side from a TRADE (3 weeks or less) TREND (3 months or more) and TAIL ( 3 years or less). Today's new from DIN and CHUX suggest that Chili's is gaining share in the Bar & Grill space

FULL SERVICE SECTOR

STEAK CATEGORY: Outback Steakhouse launched a new holiday promotion Wednesday that includes steak combinations with grilled shrimp, ribs and lobster tail. Officials with Outback’s Tampa, Florida-based parent OSI Restaurant Partners LLC, said the combination plates start at $11.99 and will be available through January 17. Options include herb-roasted prime rib paired with a lobster tail and served with a side salad; Outback’s signature sirloin paired with a skewer of grilled shrimp; or a six-ounce sirloin served with a half-rack of wood-fired grilled ribs. All are served with a dressed baked potato

DIN: Dine Equity reported Q3 EPS of $1.04 versus expectations of $0.99. The company reduced guidance for Applebee’s domestic system-wide same-restaurant sales performance to a range of 1.5% to 2% versus 2% to 4% prior. Consensus is 1.7%. Consolidated free cash flow guidance was lowered to between $104 and $114M which reflects a reduction from previous expectations of $112 to $122M. We believe that Chili’s is part of the problem and continue to like EAT.

CHUX: O’Charley’s reported a loss of -$0.18 versus expectations of -$0.17 for the third quarter. Comps came in at -0.9% versus consensus of +0.7%. The overcrowded Bar & Grill category is suffering. Ninety Nine’s 3Q comps were +4.1% versus expectations of +1.7% and Stoney River printed a +6.8% versus expectations of +3.8%.

DRI: Darden was downgraded to Neutral by Janney Montgomery on concern that comps are decelerating. We agree that comps are decelerating but there are better shorts in the group.

CAKE: Cheesecake Factory was downgraded to Neutral by Janney Montgomery.

Howard Penney

Managing Director

Rory Green

Analyst