This note was originally published at 8am on October 31, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“We can lick gravity, but sometimes the paperwork is overwhelming.”

-Werner von Braun

The only problem with last week contributing to the best month for stocks since 1974, is the 1970s. This morning, between German Retail Sales falling to flat year-over-year and Eurozone inflation (CPI) remaining at +3%, European Stagflation remains.

Most of last week’s fanfare can be boiled down to one solid gravitational factor that underpins all of the math behind what we’ve been calling The Correlation Risk – the US Dollar. If you get the US Dollar Index’s direction right, you’ll get most other things right.

The US Dollar Index is up +1.3% so far this morning. That’s a good start to my week because my being long it last week was nasty. Inclusive of a -1.7% week-over-week drawdown, the US Dollar was down for the 3rdconsecutive week, and down -4.6% since the week ended October 7th, 2011.

Since that 1stweek of October (after the Cover of Barron’s said “Watch Out, Mr. Bull” – this weekend it said “Not So Fast, Mr. Bear”?), this is what other major moves in Global Macro have looked like:

- Euro/USD = +6.1%

- CRB Commodities Index = +6.6%

- Oil = +12.5%

- Copper = +14.9%

- Volatility (VIX) = -32%

- 10-yr US Treasury Yield = +12%

So what was this all about – Growth or Gravity?

We’ve had plenty of rallies since the start of 2011 where consensus has been convinced that this has been all about growth. The only problem with that is that there is a big difference between growth and inflation. That’s why the legitimate calculations of GDP growth apply a legitimate “deflator” to the nominal growth estimate. It’s called the purchasing power of money.

Remember in Q1 of 2011 when Sell-Side and Washington “economists” had +3-4% 2011 GDP and 1450 SP500 targets? We do. We also remember that the price of oil was tracking upwards of $110/barrel – and that had a big impact on global economic growth slowing.

After it was revised -81% to the downside versus the “preliminary US government estimate”, US GDP growth in 1Q11 was only 0.36%. That was using a “deflator” that we’d consider accommodative to the Big Government Interventionist camp that it’s not Policy, Stupid.

That was then – this is now. What does this economy need from here?

A) More US Dollar Debauchery

B) Higher Oil prices

C) Stock market cheerleading based on A) and B)

Alex, I’ll take a restroom break and the other side of Jon Corzine’s long/short book for $1,000.

Obviously most people whose compensation isn’t solely tied to stock market inflations are allowed to get the point here. Not surprisingly, amidst last week’s generational squeeze, a few not so funny things happened on the way to the Europig Forum:

- European PIIG Bond Yields (Italy most specifically) hit new 3-year highs

- TED Spread (measures global banking counterparty risk) hit a new 2011 YTD high

- US Financials (XLF), The Russell 2000 (IWM), and the price of Copper (JJC) all failed at their long-term TAIL lines of resistance

Now that last point is probably the most interesting – because, essentially, it ties back to the aforementioned point about growth. It’s a question really. The Question this morning (as in what you do with your money right here and now): is Global Growth “back” OR was that just another Dollar Down reflation of asset prices?

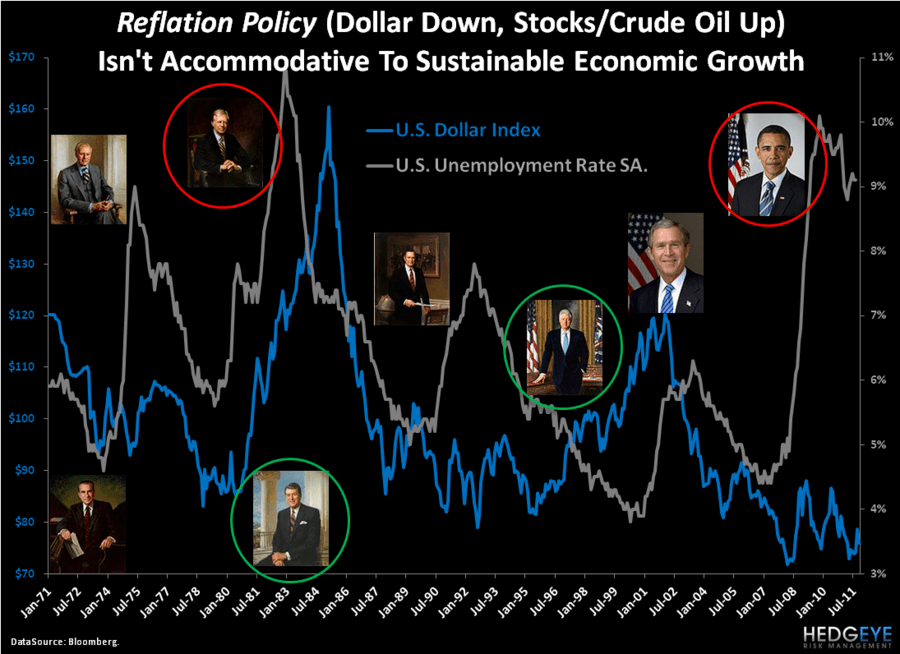

Longer-term, I think the only way to recover real US economic growth (adjusting for inflation) is to:

1. Strengthen the US Dollar

2. Deflate The Inflation

3. Strengthen Employment

In the Chart of the Day, you’ll see this quite clearly across US Presidential terms. Someone running for President in 2012 really needs to use this picture. Going all the way back to when Richard Nixon abandoned the Gold Standard (1971) and embarked on today’s Euro-style debt monetization scheme, a Strong US Dollar = Strong America.

To be sure, looking back at the last 18 days of the biggest move ever in stock prices (ever is a long time), Licking Gravity’s short-term political resolve has its Month-End Markup perks, for some of us…

But, for most of us, the long-term TAILs of Global Growth are still broken.

My immediate-term support and resistance ranges for Gold (bullish TRADE and TREND), Oil (bullish TRADE; bearish TAIL), German DAX (bullish TRADE; bearish TAIL), and the SP500 (bullish TRADE and TREND) are now $1706-1774, $90.19-93.86, 6098-6455, and 1267-1294, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer