THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - November 3, 2011

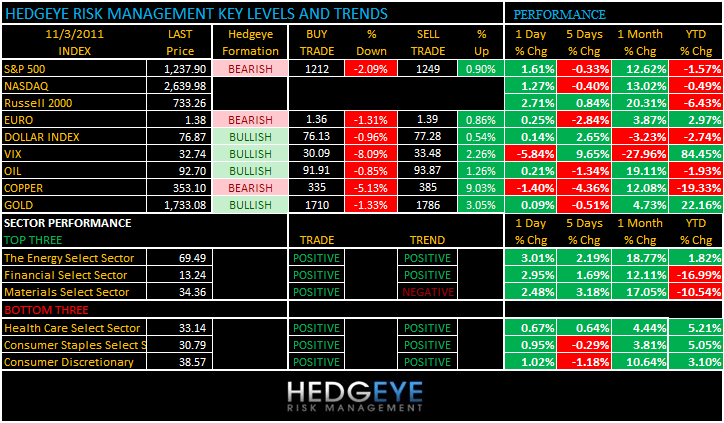

Another day, another dislocation between stocks and bonds – bond yields have had the big moves right in 2011. As we look at today’s set up for the S&P 500, the range is 37 points or -2.09% downside to 1212 and 0.90% upside to 1249.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1998 (+4151)

- VOLUME: NYSE 957.34 (-27.98%)

- VIX: 32.74 -5.84% YTD PERFORMANCE: +84.45%

- SPX PUT/CALL RATIO: 2.29 from 2.29 (-0.28%)

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – UST 10yr yields are down -16% (39 bps) since this hour of the morning last Thursday; that’s a lot. And now we have 10s bearish on both TRADE and TREND durations again (TRADE line support was 2.11% and we’re looking at 2.02% this morning with the Yield Spread (10s minus 2s) down from 203bps wide at the start of the wk to 179bps this morn – not good).

- TED SPREAD: 43.30

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.03 from 2.01

- YIELD CURVE: 1.80 from 1.78

MACRO DATA POINTS (Bloomberg Estimates):

- 8am: RBC Consumer Outlook, prior 39.2

- 8:30am: Nonfarm Productiviity, est. 3.0%, prior -0.7%

- 8:30am: Jobless claims, est. 400k, prior 402k

- 9:45am: Bloomberg Consumer Comfort, prior 51.1

- 10am: ISM Non-Manufacturing, est. 53.5, prior 50.0

- 10am: Factory orders, est. -0.2%, prior -0.2%

- 10:30am: EIA natural gas storage, est. 70, prior 92

WHAT TO WATCH:

- American Eagle Outfitters (AEO): narrows 3Q earnings forecast to 26c-27c/shr from 22c-27c, exceeding est. by at least 3c

- Costco (COST); U.S. comp sales ex-fuel beat est.

- Whole Foods Market (WFM): fails to increase its fiscal 2012 profit forecast, still sees EPS $2.21-$2.26

- Groupon IPO expected to price this evening; yesterday, co. was said to stop taking orders for IPO because of demand

- German, French leaders withheld EU8b, warned that Greece will surrender all European aid if it votes against bailout package agreed only last week.

- MF Global’s commodity customer funds have shortfall of $633m, CFTC said

- SEC likely to file charges against more Wall Street firms in connection with sale of mortgage-linked securities: FT

- Bank of England, ECB announce interest rate decisions later today

COMMODITY/GROWTH EXPECTATION

COMMODITIES: The CRB Index remains bearish TREND and TAIL with a wall of resistance 326-335

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Porsche Sells Malbec to Keep Autos Coming Into Argentina: Cars

- Ikea’s Paper Pallet Challenges Wood’s 50-Year Dominance: Freight

- Skunky Smells, 150-Decibel Blasts Pitched as Pirate Defenses

- Gold Drops With Commodities as European Leaders Cut Greek Aid

- China Record Corn Crop Still Failing to Meet Demand: Commodities

- World Food Prices Drop Most in 19 Months on Grain, Dairy Slump

- MF May Have Transferred Customer Money After Audit, CME Says

- Oil Drops After Europe Freezes Greek Aid, U.S. Stockpiles Rise

- U.S. Stocks Rebound, Commodities Rise as Dollar Slips After Fed

- Coal India to Quicken Search for Overseas Mines as Output Drops

- China Plans ‘Orderly’ Delivery of New Ships as Glut Hits Rates

- Midwest Refinery Upgrades Boost Canadian Crudes: Energy Markets

- Copper Declines on Concern European Debt Crisis to Damp Demand

- Copper Resumes Drop on More Signs of China Slowdown: LME Preview

- China Will Not Change Domestic Monetary Policy, Zhang Says

- Thousands March in Oakland Shutting Down Fifth Busiest U.S. Port

- Twenty-Five Indonesian Tin Producers to Extend Export Ban

- Oil Near Two-Month High as Europe Presses Greece on Rescue Deal

- U.S. Rebel’s Split Riles $6 Billion World of Ethical Commerce

- Top Gold Forecasters See Rally to Record by March: Commodities

CURRENCIES

EUROPEAN MARKETS

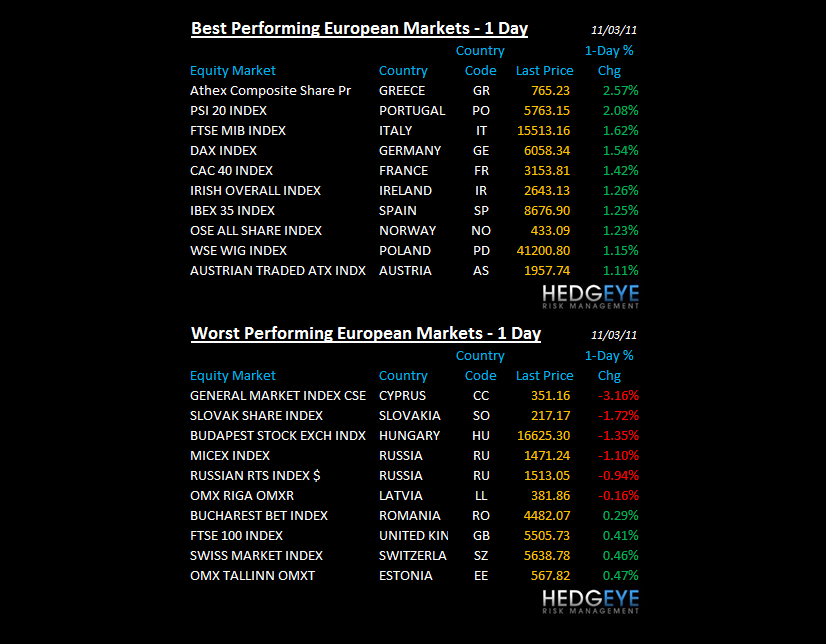

EUROPE - "off the lows" again, this rally looks really suspect (no volume) as the CAC in particular remains bearish/broken across durations

FRANCE – interestingly, but not surprisingly, French bond yields are flagging the nasty – whether you look at the spread risk b/t German Bunds or the nominal level of French 10s, it all looks the same to me – on the stock side, the CAC40 keeps failing at my TREND zone of 3403. France’s stock market remains in crash mode (> 20% peak to trough decline for the YTD)

ASIAN MARKETS

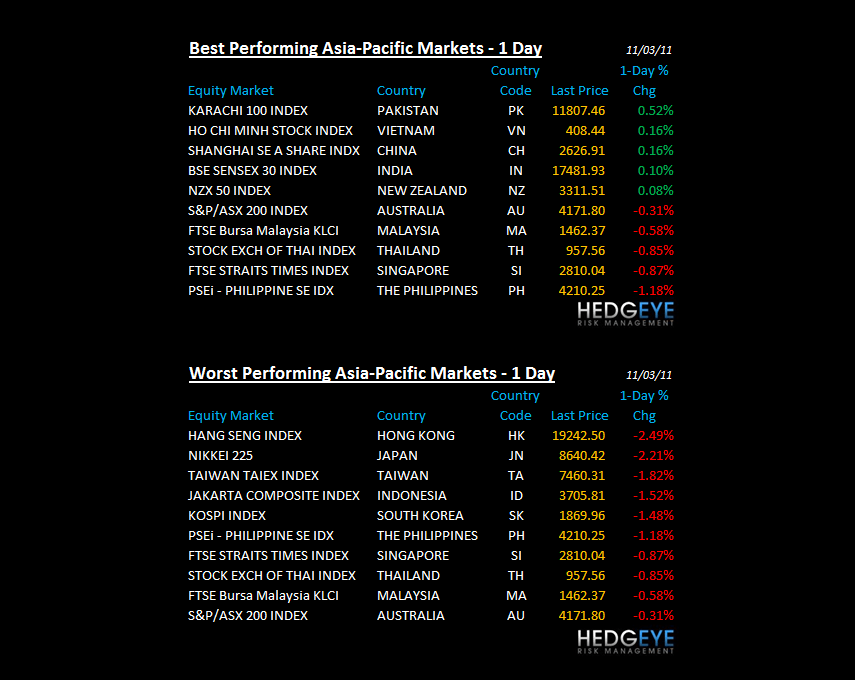

ASIA: ugly breakdowns in both the Hang Seng (-2.5%) and KOSPI (1.5%) overnight; both remain bearish on the Hedgeye TREND duration

MIDDLE EAST

The Hedgeye Macro Team

Howard Penney

Managing Director